With its stock down 12% over the past three months, it is easy to disregard WD-40 (NASDAQ:WDFC). However, stock prices are usually driven by a company's financials over the long term, which in this case look pretty respectable. Particularly, we will be paying attention to WD-40's ROE today.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. In other words, it is a profitability ratio which measures the rate of return on the capital provided by the company's shareholders.

How Do You Calculate Return On Equity?

ROE can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for WD-40 is:

32% = US$68m ÷ US$216m (Based on the trailing twelve months to February 2024).

The 'return' refers to a company's earnings over the last year. Another way to think of that is that for every $1 worth of equity, the company was able to earn $0.32 in profit.

What Is The Relationship Between ROE And Earnings Growth?

Thus far, we have learned that ROE measures how efficiently a company is generating its profits. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company's earnings growth potential. Assuming everything else remains unchanged, the higher the ROE and profit retention, the higher the growth rate of a company compared to companies that don't necessarily bear these characteristics.

WD-40's Earnings Growth And 32% ROE

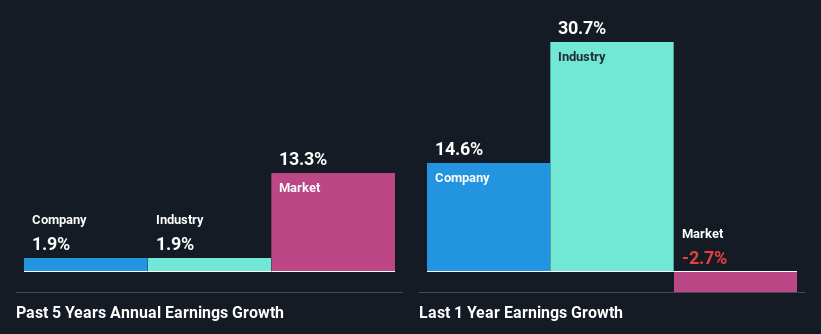

To begin with, WD-40 has a pretty high ROE which is interesting. Additionally, the company's ROE is higher compared to the industry average of 22% which is quite remarkable. Given the circumstances, we can't help but wonder why WD-40 saw little to no growth in the past five years. Based on this, we feel that there might be other reasons which haven't been discussed so far in this article that could be hampering the company's growth. These include low earnings retention or poor allocation of capital

We then performed a comparison between WD-40's net income growth with the industry, which revealed that the company's growth is similar to the average industry growth of 1.9% in the same 5-year period.

Earnings growth is an important metric to consider when valuing a stock. It's important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). This then helps them determine if the stock is placed for a bright or bleak future. Is WD-40 fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is WD-40 Making Efficient Use Of Its Profits?

With a high three-year median payout ratio of 66% (implying that the company keeps only 34% of its income) of its business to reinvest into its business), most of WD-40's profits are being paid to shareholders, which explains the absence of growth in earnings.

In addition, WD-40 has been paying dividends over a period of at least ten years suggesting that keeping up dividend payments is way more important to the management even if it comes at the cost of business growth.

Summary

In total, it does look like WD-40 has some positive aspects to its business. Its earnings have grown respectably as we saw earlier, which was likely due to the company reinvesting its earnings at a pretty high rate of return. However, given the high ROE, we do think that the company is reinvesting a small portion of its profits. This could likely be preventing the company from growing to its full extent. With that said, the latest industry analyst forecasts reveal that the company's earnings are expected to accelerate. To know more about the latest analysts predictions for the company, check out this visualization of analyst forecasts for the company.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.