Stock pickers are generally looking for stocks that will outperform the broader market. And in our experience, buying the right stocks can give your wealth a significant boost. To wit, the Qinghai Jinrui Mineral Development share price has climbed 46% in five years, easily topping the market return of 15% (ignoring dividends). However, more recent returns haven't been as impressive as that, with the stock returning just 3.8% in the last year.

After a strong gain in the past week, it's worth seeing if longer term returns have been driven by improving fundamentals.

While Qinghai Jinrui Mineral Development made a small profit, in the last year, we think that the market is probably more focussed on the top line growth at the moment. Generally speaking, we'd consider a stock like this alongside loss-making companies, simply because the quantum of the profit is so low. For shareholders to have confidence a company will grow profits significantly, it must grow revenue.

For the last half decade, Qinghai Jinrui Mineral Development can boast revenue growth at a rate of 15% per year. Even measured against other revenue-focussed companies, that's a good result. It's good to see that the stock has 8%, but not entirely surprising given revenue shows strong growth. If you think there could be more growth to come, now might be the time to take a close look at Qinghai Jinrui Mineral Development. Of course, you'll have to research the business more fully to figure out if this is an attractive opportunity.

For the last half decade, Qinghai Jinrui Mineral Development can boast revenue growth at a rate of 15% per year. Even measured against other revenue-focussed companies, that's a good result. It's good to see that the stock has 8%, but not entirely surprising given revenue shows strong growth. If you think there could be more growth to come, now might be the time to take a close look at Qinghai Jinrui Mineral Development. Of course, you'll have to research the business more fully to figure out if this is an attractive opportunity.

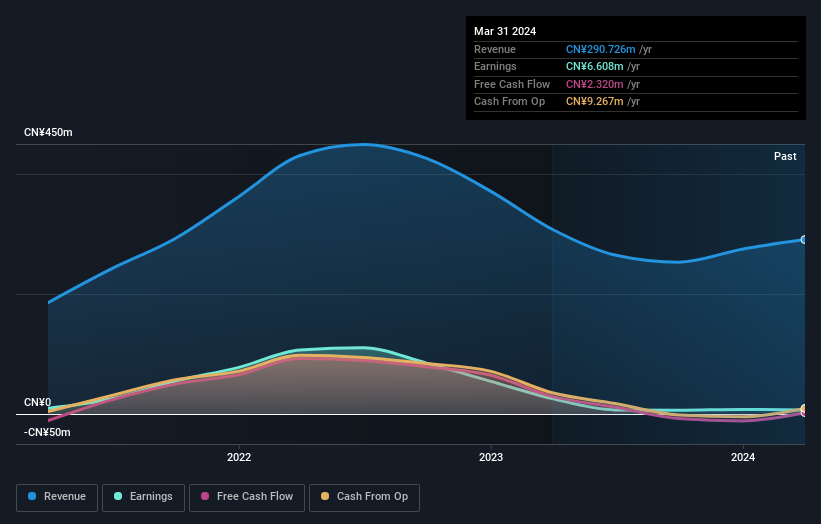

The image below shows how earnings and revenue have tracked over time (if you click on the image you can see greater detail).

This free interactive report on Qinghai Jinrui Mineral Development's balance sheet strength is a great place to start, if you want to investigate the stock further.

A Different Perspective

It's good to see that Qinghai Jinrui Mineral Development has rewarded shareholders with a total shareholder return of 3.8% in the last twelve months. However, the TSR over five years, coming in at 8% per year, is even more impressive. The pessimistic view would be that be that the stock has its best days behind it, but on the other hand the price might simply be moderating while the business itself continues to execute. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. Consider for instance, the ever-present spectre of investment risk. We've identified 3 warning signs with Qinghai Jinrui Mineral Development , and understanding them should be part of your investment process.

If you like to buy stocks alongside management, then you might just love this free list of companies. (Hint: many of them are unnoticed AND have attractive valuation).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Chinese exchanges.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.