Nvidia Has Gained Over $1 Trillion in Market Cap in 2024. Can It Do It Again to Surpass Microsoft and Apple to Become the Most Valuable Company in the World?

After gaining 239% in 2023 to become the best-performing component of the S&P 500, Nvidia (NASDAQ: NVDA) has sustained its momentum so far this year. The stock has nearly doubled -- gaining over $1.1 trillion in market cap year to date -- and 2024 isn't even halfway over.

At the end of 2022, Nvidia was worth $359 billion. And suddenly, less than a year and a half later, it could be worth $3 trillion, surpassing Microsoft and Apple in market cap.

At the rate the stock is going up, Nvidia is on track to accomplish that feat by year-end. But no growth stock goes up in a near-straight line forever. Let's find out what it would take for Nvidia to slow down, and even if it does, why it could still take pole position as the most valuable company in the world.

Checking all the boxes

One look at Nvidia's price chart over the last couple of years, and it's hard to argue that the stock isn't overvalued. It looks like yet another case of a stock that ran too far too fast and is primed for a sell-off. And maybe it is.

However, Nvidia has (mostly) gone up for the right reasons. The extent of the run-up may be overdone, but Nvidia checks all the boxes that growth investors look for. And when the story is that good, the only thing preventing a stock from soaring is the valuation.

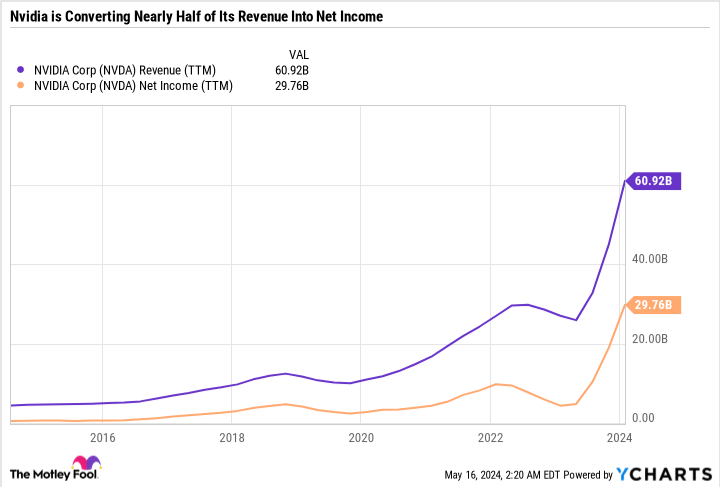

A hockey stick graph, or hockey stick curve, resembles flattish growth and then a sharp upward-sloping line to the right that illustrates breakneck growth. Nvidia's sales and net income have this pattern in spades.

Nvidia is converting nearly $0.50 on every dollar in sales into net income -- not gross profit or operating income, but bottom-line net income. That is an incredible achievement, especially at the scale at which Nvidia is doing it.

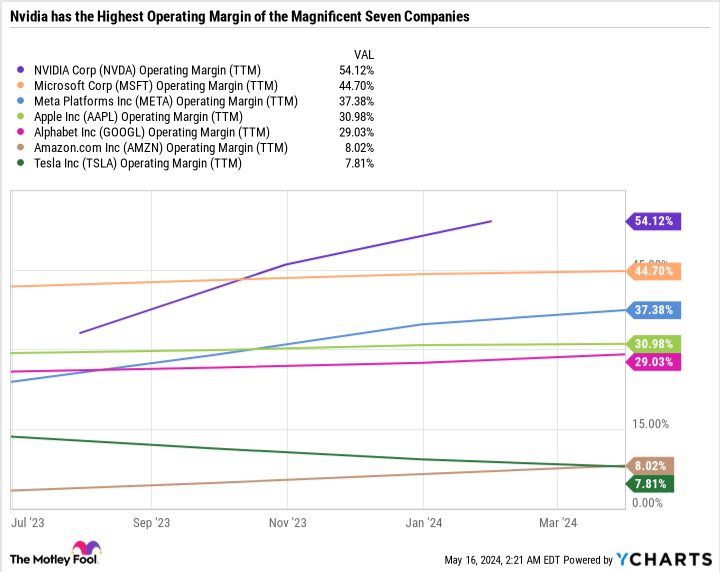

Nvidia also has extremely high operating margins -- higher than any other "Magnificent Seven" company -- a term that refers to large, industry-leading growth stocks Microsoft, Apple, Nvidia, Alphabet, Amazon, Meta Platforms, and Tesla.

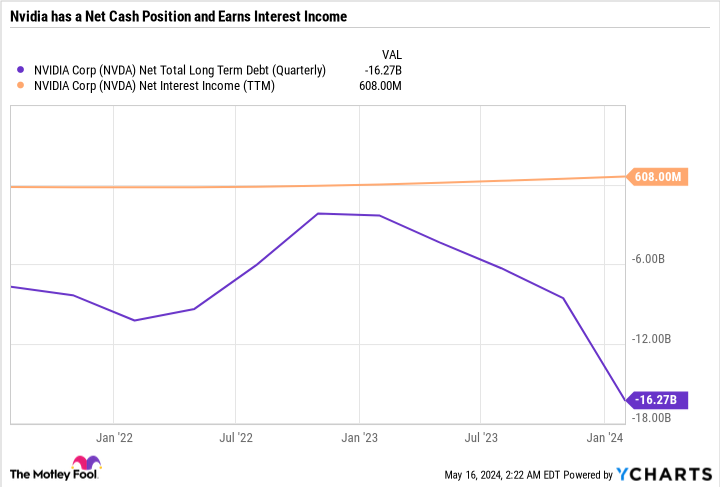

To top it all off, Nvidia has a net cash position on its balance sheet. In fact, it makes money on its cash -- generating over $600 million in interest income over the last 12 months.

This is what checking all the boxes looks like. But the question is how long can Nvidia keep growing at this rate?

Spearheading a revolutionary market

Sustained rallies in the stock market aren't always smoke and mirrors. In Nvidia's case, the company has done a phenomenal job monetizing its computing power in various industries. If you go back and look at Nvidia's annual reports from a few years ago -- or better yet -- five-plus years ago, you'll notice that the company looked almost indistinguishable from today.

Nvidia's biggest market used to be selling graphics processing units (GPUs) for gaming, personal computers, and data visualization. All of these applications involve massive data sets that need to be visualized and analyzed, and that require immense computing power. These are still profitable and growing business segments for Nvidia, but they don't make or break the business like in past years.

The crypto industry figured out that Nvidia's GPUs were great for mining (what blockchain networks use to affirm transactions and release new coins into circulation). This opportunity expanded the end use cases for its product offering even further.

Nvidia's products are also useful for increasingly sophisticated automobiles and help support electric vehicles.

But the value of these use cases pales in comparison to what Nvidia's GPUs were seemingly born to do: handle massive datasets and compile simulations for data centers to address customers' artificial intelligence (AI) needs. The change didn't happen overnight, but product improvements and technological breakthroughs have positioned Nvidia as a leader in AI because it makes the products that complex AI models need to run.

In 2024, Nvidia's compute and networking segment made up over 77% of revenue and 85% of segment operating income. The reason Nvidia's stock price is unrecognizable from where it was a few years ago is because Nvidia (the company) is also unrecognizable.

The best bull case for Nvidia is that it is a rally backed by fundamentals and a multidecade growth industry. If AI adoption continues, it stands to reason that Nvidia will continue to see increased demand.

Four challenges worth considering

As great as Nvidia's business looks today, I think there are four main challenges investors should consider before buying the stock.

The first is competition. Nvidia is vulnerable to losing market share even if the overall market opportunity keeps getting bigger.

The second is AI adoption slowing. Right now, companies are investing in AI, which is a boon for Nvidia's business. But eventually, they'll have to make a return on those investments. Investing in AI and monetizing AI are two completely different things. For example, Adobe's recent results disappointed Wall Street and sent the stock tumbling. Adobe is heavily investing in AI and is seeing great results and product improvements -- but it has been expensive and is damaging its short-term earnings results, which is testing investors' patience. That's not exactly good news for Nvidia, considering Adobe is a major customer.

The third concern, which is related to the second, is the cyclicality of the chip industry. Nvidia isn't a software-as-a-service company with consistent inflows -- it sometimes gets huge spikes in orders followed by order declines. Meta Platforms plans to spend $10 billion on Nvidia GPUs by the end of 2024. That's a massive purchase, not an annual recurring expense.

This rapid sales surge, followed by a decline in growth, is reflected in analyst consensus earnings per share (EPS) projections, which call for $24.98 in fiscal 2025 EPS, followed by $32.10 in fiscal 2026 EPS. Nvidia earned $11.93 in fiscal 2024 EPS -- implying that EPS would more than double in fiscal 2025, but then decelerate and grow by less than 30% in fiscal 2026.

That leads me to the fourth concern: valuation. Nvidia has a sky-high price-to-earnings (P/E) ratio of 79 -- but due to the expected growth, the forward P/E is a much more reasonable 37.6. That gives Nvidia a lower forward P/E than Costco Wholesale -- illustrating that rapid earnings growth can make a seemingly expensive stock look more affordable. But that forward P/E is only if Nvidia achieves analysts' lofty expectations. Still, anything close to those estimates would be a big win and could drive the stock higher. That's not really the concern. The bigger risk is what comes after that. So much growth in so little time may open the door to a slowdown.

Let's say that Nvidia shoots up another 50% by the time its fiscal 2024 results are out and achieves the consensus estimates. At that point, the company would be worth over $3.5 trillion. And assuming Microsoft and Apple stall, that would make Nvidia the most valuable company in the world. But the stock would also have a P/E over of around 56. And if growth is only expected to be 30%, investors may realize that's simply too high of a price to pay, even for a great company.

A bad setup

I could see Nvidia pushing the limits of a $3 trillion market cap if investors get enamored with its growth in fiscal 2024. But the problem is that the stock is somewhat set up to fail over the next three to five years given its near-term growth will make its comps that much harder in fiscal 2026 and beyond.

Pair that backdrop with uncertainty, the cyclicality of the chip industry, and unforeseen challenges, and the risk simply outweighs the reward.

To consider buying Nvidia, I'd have to see the valuation make more sense on a multiyear time horizon. If growth slows and it falls out of favor, Nvidia could start to look really cheap. But for now, it's just too hot of a story that can seemingly do no wrong.

Ultimately, I think Microsoft maintains its crown as the most valuable company simply because it has a more of a rinse-and-repeat, less cyclical business model that spans a variety of end markets. It is also high margin and has plenty of cash to fuel dividends, buy back stock, and make strategic acquisitions.

Nvidia has what it takes to gain another $1 trillion in market cap, but there are too many question marks beyond that outlook to consider buying the stock now.

Should you invest $1,000 in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $566,624!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of May 13, 2024

Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool's board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool's board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool's board of directors. Daniel Foelber has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Adobe, Alphabet, Amazon, Apple, Costco Wholesale, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Fool recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Nvidia Has Gained Over $1 Trillion in Market Cap in 2024. Can It Do It Again to Surpass Microsoft and Apple to Become the Most Valuable Company in the World? was originally published by The Motley Fool