① Maifushi was first listed on the Hong Kong Stock Exchange on May 16. By the close, the stock price had risen 18.46% to HK$51.65, with a market capitalization of HK$12.146 billion. ② The gross margin of the McFTSE SaaS business is close to 90%, and no profit has been achieved until now.

“Science and Technology Innovation Board Daily”, May 16 (Special Correspondent Chen Junqing, Reporter Zhu Ling) Maifushi (02556.HK), a SaaS solution provider for marketing and sales, was first listed on the Hong Kong Stock Exchange today (May 16). The co-sponsors are CICC and CCB International. At the close, the stock price rose 18.46% to HK$51.65, with a market capitalization of HK$12.146 billion.

Maifushi is a marketing and sales SaaS solution provider in China. The company provides a comprehensive cloud solution covering the entire marketing and sales management process of the enterprise through the Marketingforce platform. According to Frost & Sullivan's data, based on 2022 revenue, the company is the largest marketing and sales SaaS solution provider in China, with revenue of 530 million yuan in 2022, with a market share of 2.6%.

According to the distribution results announced by Maifushi, the company sold 5.9497 million shares globally, accounting for 10% of the public sale and 90% of the international sale. For each lot of 100 shares, the sale price was HK$43.6, and the net proceeds were HK$181 million. Among them, the public sale received 5.95 times the subscription, and the international sale received 1.03 times the subscription.

▍ SaaS gross margin is nearly 90%, and losses continue to narrow

The overall revenue scale of Mifushi is expanding. According to the prospectus, from 2021 to 2023, Mifushi's revenue was 877 million yuan, 1,143 million yuan, and 1,232 billion yuan respectively. Further analysis of the revenue structure showed that the continued increase in revenue from the SaaS business was mainly due to the increase in SaaS business revenue. The total revenue share of SaaS business during the reporting period was 50%, 46.4%, and 57%, respectively, while revenue from precision marketing services reached 50.0%, 53.6%, and 43.0% respectively.

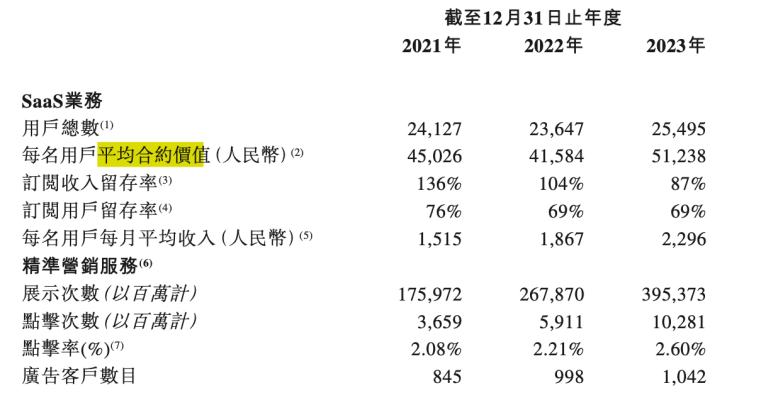

The profit essence of the SaaS business is to charge subscription fees from subscribers. During the reporting period, the total number of Maifushi Saas users was 24,1127, 23,647, and 25,496. The average contract value for each user in the SaaS business was RMB 45026, RMB 41,584, and RMB 51238, respectively. Whether it is an increase in the number of users or an increase in the average contract value per user, it has had a positive impact on the increase in revenue.

Judging from profitability, Maifushi's performance is still relatively stable. During the reporting period, Maifushi's gross margins were 54.5%, 49%, and 57.3%, respectively. Although overall gross margins were high, there were certain fluctuations. However, on the positive side, gross margin in 2023 is 8.3% higher than in 2022, which is quite significant. Among them, the gross margin generated by revenue from the SaaS business was relatively high. The gross margins were 90.1%, 89.2%, and 87.7% respectively during the reporting period, which stabilized in the range of 87%-90%. This is mainly due to the relatively low costs associated with procuring third-party services and hardware to support operations.

In contrast, the gross margin of revenue generated by precision marketing services was relatively low. The gross margins of precision marketing services were 18.9%, 14.3%, and 17.0% respectively during the reporting period, mainly due to the high costs associated with purchasing advertising traffic from media platforms for online advertising solution services.

However, in a situation where revenue continues to expand and gross margin is also at a high level, Maifushi is still in a state of loss in the profit segment, which is also in line with the normal state of the SaaS industry in China. Losses during the reporting period The company lost approximately 273 million yuan, 216 million yuan and 169 million yuan respectively during the same period, with a cumulative loss of about 660 million yuan over three years. The adjusted net losses were approximately $130 million, $132 million and $28 million, respectively. Overall, Maifushi still showed insufficient hematopoietic capacity in terms of profit and loss, but there was a marked improvement in the trend, and the adjusted net loss in 2023 has shrunk to a level close to the break-even line.

▍ High expenses and R&D expenses

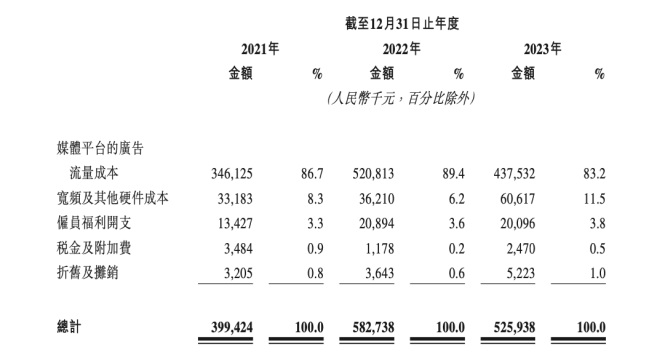

High traffic costs are the largest part of MaFTSE's service costs, and traffic costs have always accounted for more than 80% of service costs during the reporting period. Through observation, the reporter found that the investment in traffic costs was highly correlated with the revenue of the online advertising solution service business.

In response, Maifushi stated in its prospectus that the cost of advertising traffic on media platforms increased from RMB 346.1 million in 2021 to RMB 520.8 million in 2022. This is broadly in line with business growth in online advertising solutions services. The cost of advertising traffic on our media platform was reduced from RMB 520.8 million in 2022 to RMB 437.5 million in 2023, in line with the decline in revenue from online advertising solutions services.

According to Frost & Sullivan, when it comes to precision marketing businesses, advertising traffic procurement costs for media platforms usually account for 90% to 99% of the total cost of services. From 2018 to 2022, the price of online traffic has increased by about 20%. As a result, enterprises are increasingly willing to adopt marketing and sales SaaS solutions to help attract and convert customers in an efficient manner.

Maifushi is also well aware of this. The specific signs are increasing sales and distribution expenses, which were 284 million yuan, 315 million yuan, and 327 million yuan respectively during the three years of the reporting period. In addition, R&D expenses, which are the second-largest expenditure of Maxfos, have also remained high all year round, recording 160 million yuan, 224 million yuan, and 210 million yuan respectively during the reporting period.

High R&D expenses also reflect the continued expansion of the company's SaaS business and efforts to improve its own profitability. According to Frost & Sullivan, SaaS solution providers often lose money when expanding their business due to the time gap between revenue recognition and operating expenses. Although SaaS companies incur significant expenses from R&D to sales, distribution, and management, the resulting revenue growth may only be seen in later stages because revenue is recognized during the contract period.

The continued high level of these expenses has the most direct impact on MagFTSE's profitability and is also the main reason for the company's losses.

▍ 2.6% market share, ranking first in China

On the market side, Maifushi's products are mainly aimed at B2B customer groups. The customers are relatively diverse. The top five major customers each generate 40% to 50% of the total revenue for the same year. On the other hand, on the supplier side, the fees of the top five suppliers each account for more than 90 per year's sales costs. The process of excessive reliance on suppliers not only increases cost risks, but also greatly limits their growth potential and development space.

With a market share of 2.6% in terms of revenue in 2022, Maifushi ranked first, but it did not close the gap with second place. The marketing and sales SaaS solutions market in China is currently in a growth stage. The degree of diversification is relatively high, and there is plenty of room for improvement in market share.

According to Frost & Sullivan's report, the potential market size of marketing and sales of SaaS solutions in China has maintained a compound annual growth rate of over 29%, and is expected to reach 74.5 billion yuan in 2027. The performance of this listing shows that Maifushi has certain capital strength. The capital raised will further accelerate its development in the AI SaaS field, stabilize its competitiveness in the market, and occupy more market share.