Yahoo Finance

Yahoo Finance Why PepsiCo Looks Like a Better Dividend Play Than Coca-Cola

PepsiCo Inc. (NASDAQ:PEP) and the Coca-Cola Co. (NYSE:KO) are among the best-known packaged food and beverage companies in the world. In addition, they share quite a bit of similarities, from their target markets to their business models to their financial profiles.

But as the saying goes, the devil is in the details. As I will argue below, a closer look at a few key operating and financial metrics suggests that PepsiCo might be the best dividend stock to own.

Dividend yield: A tie that favors PepsiCo

This Powerful Chart Made Peter Lynch 29% A Year For 13 Years

How to calculate the intrinsic value of a stock?

When it comes to dividend stock investing, the yield is considered by many to be the most important number. Yield is the ratio of the dividend per share payment, usually annualized based on the disbursements made in the last 12 months, by the share price. In other words, yield is what investors get to pocket relative to how much the stock is currently worth in the market.

As the chart below depicts, PepsiCo and Coca-Cola yield virtually the same today: 3.10%. The yield is enticing, in my view, even if not stratospheric, beating core PCE inflation by about 30 basis points.

Source: Koyfin

Notice, however, that PepsiCo has historically and consistently yielded less than Coca-Cola going back at least five years. In my view, this has been the case due to PepsiCo's higher growth and perceived better quality.

So despite PepsiCo and Coca-Cola yielding the same today, I believe this is a positive for the former. Simply put, I believe investors now have a chance to own a stock that rarely offers a yield that is better than (or even equal to) its key Atlanta-based competitor.

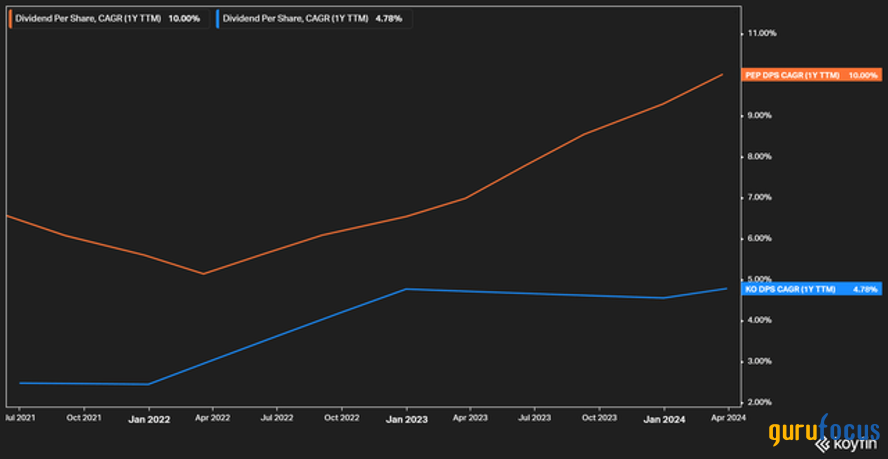

Dividend growth: PepsiCo wins

While some dividend investors emphasize (sometimes too much) the yield when deciding which stock to buy, other factors should be considered as well. Dividend growth is one of them.

Looking back since the peak of the Covid-19 crisis (see chart below), PepsiCo has increased its per-share dividend payments at a substantially faster pace than Coca-Cola: 10% today on a trailing 12-month basis versus Coke's 5%.

All else held equal, investors are better off owning a stock whose company tends to increase the dividend payments over time - and likely will continue to do so going forward. At the risk of oversimplifying the analysis, 10% annual growth in PepsiCo's dividend projected over the next five years suggests a dividend yield of 4.90% by 2029, assuming an unchanged share price. In the case of Coca-Cola, the projected yield would be a less enticing 3.90% assuming the current dividend growth rate of 5%.

Source: Koyfin

Financial robustness: Coca-Cola (barely) wins

Of course, paying a dividend alone is not enough: the company needs to be able to sustain that dividend payment in the future, if not grow it above the inflation rate at least. This is where financial robustness comes into play.

I define financial robustness from two different angles: free cash flow generation and the strength of the balance sheet.

In 2023, PepsiCo produced $7.90 billion in free cash flow, a drastic improvement of 41% year over year and 10% annualized from the pre-pandemic levels of 2019. Last year, the FCF generated was 19% higher than the total dividend payments made. With constant-currency earnings per share projected to rise by 8% in 2024, the dividend payments seem to be well covered.

Coca-Cola looks slightly better. While FCF has grown by only 4% per year since 2019, last year's $9.70 billion was 23% higher than the $8 billion in dividend payments made, suggesting a modestly higher dividend coverage ratio.

On the balance sheet side, PepsiCo's net debt of $37.1 billion represents a less-than-concerning 37% of total assets. Coca-Cola looks better, with $30.9 billion in net debt adding up to 32% of its total assets.

While I believe Coca-Cola wins the financial robustness battle against PepsiCo based on the above, I think it barely does so. In the end, PepsiCo's dividend coverage and balance sheet seem to be good enough to support the yield and dividend payment growth.

Stability of the business model: PepsiCo wins

Lastly, and turning to a more qualitative discussion, I think PepsiCo runs a more balanced, more stable business model.

The New York-based company generates about 27% of its revenue and 56% of its operating profits from its snack division (Frito Lay) in North America, which provides better top- and bottom-line diversification. Meanwhile, Coca-Cola is almost exclusively a beverage business that, granted, finds slightly better geographical diversification than its key peer.

In addition, PepsiCo's business is better distributed across at-home and away-from-home channels, in part due to Frito Lay and Quaker. This helps to explain why its revenues increased by 5% in the first pandemic year, while Coca-Cola saw its sales decline by a painful 11% in 2020 due to the lockdowns.

All things held equal, I would rather invest in a company whose business model is better balanced if the goal is to reliably collect dividend payments along the way.

In summary

While I believe PepsiCo and Coca-Cola are both good dividend stocks to own, I think the former is a better bet today. Supporting the argument are a historically low dividend yield premium that usually favors Coke, PepsiCo's history of increasing the dividend payments more aggressively and PepsiCo's more stable business model, despite Coca-Cola seemingly having an edge over its competitor on financial robustness.

This article first appeared on GuruFocus.