With EPS Growth And More, Jackson Financial (NYSE:JXN) Makes An Interesting Case

With EPS Growth And More, Jackson Financial (NYSE:JXN) Makes An Interesting Case

For beginners, it can seem like a good idea (and an exciting prospect) to buy a company that tells a good story to investors, even if it currently lacks a track record of revenue and profit. Unfortunately, these high risk investments often have little probability of ever paying off, and many investors pay a price to learn their lesson. Loss making companies can act like a sponge for capital - so investors should be cautious that they're not throwing good money after bad.

對於初學者來說,收購一家向投資者講述好故事的公司似乎是個好主意(也是一個令人興奮的前景),即使該公司目前缺乏收入和利潤記錄。不幸的是,這些高風險投資通常幾乎不可能獲得回報,許多投資者爲吸取教訓付出了代價。虧損的公司可以像海綿一樣爭奪資本,因此投資者應謹慎行事,不要一筆又一筆地投入好錢。

If this kind of company isn't your style, you like companies that generate revenue, and even earn profits, then you may well be interested in Jackson Financial (NYSE:JXN). While this doesn't necessarily speak to whether it's undervalued, the profitability of the business is enough to warrant some appreciation - especially if its growing.

如果這種公司不是你的風格,你喜歡那些創造收入甚至賺取利潤的公司,那麼你很可能會對傑克遜金融(紐約證券交易所代碼:JXN)感興趣。儘管這並不一定說明其估值是否被低估,但該業務的盈利能力足以保證一定的升值——尤其是在其增長的情況下。

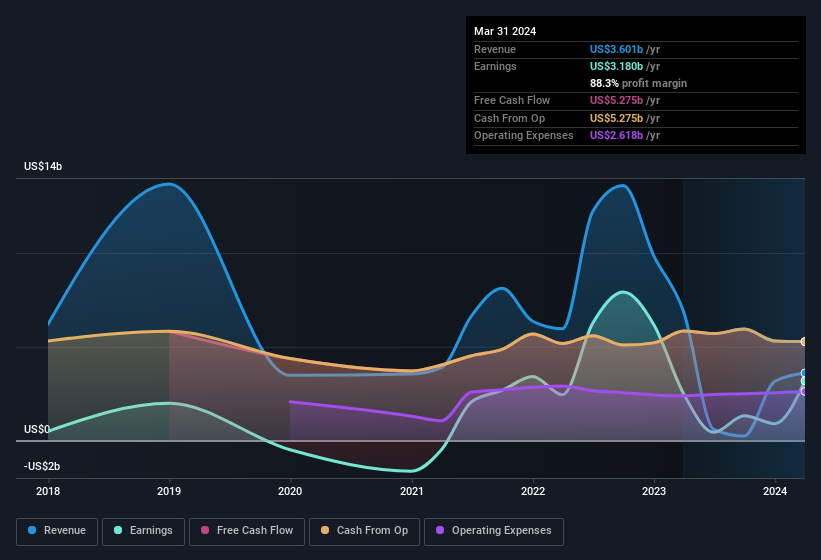

How Quickly Is Jackson Financial Increasing Earnings Per Share?

傑克遜金融每股收益的增長速度有多快?

Generally, companies experiencing growth in earnings per share (EPS) should see similar trends in share price. That makes EPS growth an attractive quality for any company. Over the last three years, Jackson Financial has grown EPS by 5.1% per year. While that sort of growth rate isn't anything to write home about, it does show the business is growing.

通常,每股收益(EPS)增長的公司的股價應該會出現類似的趨勢。這使得每股收益的增長對任何公司來說都是一種有吸引力的品質。在過去的三年中,傑克遜金融的每股收益每年增長5.1%。儘管這種增長率並不例外,但它確實表明業務正在增長。

Top-line growth is a great indicator that growth is sustainable, and combined with a high earnings before interest and taxation (EBIT) margin, it's a great way for a company to maintain a competitive advantage in the market. It's noted that Jackson Financial's revenue from operations was lower than its revenue in the last twelve months, so that could distort our analysis of its margins. To cut to the chase Jackson Financial's EBIT margins dropped last year, and so did its revenue. That will not make it easy to grow profits, to say the least.

收入增長是可持續增長的重要指標,再加上較高的息稅前收益(EBIT)利潤率,這是公司保持市場競爭優勢的好方法。值得注意的是,傑克遜金融的收入 來自運營 低於過去十二個月的收入,因此這可能會扭曲我們對其利潤率的分析。切入正題,傑克遜金融去年的息稅前利潤率下降,收入也有所下降。至少可以說,這並不容易增加利潤。

In the chart below, you can see how the company has grown earnings and revenue, over time. To see the actual numbers, click on the chart.

在下圖中,您可以看到公司如何隨着時間的推移實現收益和收入的增長。要查看實際數字,請單擊圖表。

You don't drive with your eyes on the rear-view mirror, so you might be more interested in this free report showing analyst forecasts for Jackson Financial's future profits.

你開車時不要注視後視鏡,因此你可能會對這份顯示分析師對傑克遜金融未來利潤預測的免費報告更感興趣。

Are Jackson Financial Insiders Aligned With All Shareholders?

傑克遜金融內部人士是否與所有股東保持一致?

It's said that there's no smoke without fire. For investors, insider buying is often the smoke that indicates which stocks could set the market alight. That's because insider buying often indicates that those closest to the company have confidence that the share price will perform well. However, insiders are sometimes wrong, and we don't know the exact thinking behind their acquisitions.

據說沒有火就沒有煙霧。對於投資者來說,內幕買入通常是煙霧,表明哪些股票可能點燃市場。那是因爲內幕買盤通常表明與公司最親近的人對股價表現良好有信心。但是,內部人士有時會犯錯,我們不知道他們收購背後的確切想法。

It's good to see Jackson Financial insiders walking the walk, by spending US$291k on shares in just twelve months. This, combined with the lack of sales from insiders, should be a great signal for shareholders in what's to come. Zooming in, we can see that the biggest insider purchase was by Independent Director Derek Kirkland for US$195k worth of shares, at about US$55.67 per share.

很高興看到傑克遜金融內部人士走上正軌,在短短十二個月內花費29.1萬美元購買股票。再加上內部人士的銷售不足,對股東來說,未來應該是一個很好的信號。放大,我們可以看到,最大的內幕收購是獨立董事德里克·柯克蘭購買了價值19.5萬美元的股票,每股價格約爲55.67美元。

On top of the insider buying, it's good to see that Jackson Financial insiders have a valuable investment in the business. Holding US$97m worth of stock in the company is no laughing matter and insiders will be committed in delivering the best outcomes for shareholders. This should keep them focused on creating long term value for shareholders.

除了內幕收購外,很高興看到傑克遜金融內部人士對該業務進行了寶貴的投資。持有該公司價值9700萬美元的股票不是笑話,內部人士將致力於爲股東帶來最佳業績。這應該使他們專注於爲股東創造長期價值。

Does Jackson Financial Deserve A Spot On Your Watchlist?

傑克遜金融值得在您的關注清單上佔有一席之地嗎?

As previously touched on, Jackson Financial is a growing business, which is encouraging. In addition, insiders have been busy adding to their sizeable holdings in the company. These factors alone make the company an interesting prospect for your watchlist, as well as continuing research. What about risks? Every company has them, and we've spotted 2 warning signs for Jackson Financial (of which 1 is significant!) you should know about.

如前所述,傑克遜金融是一家成長中的企業,這令人鼓舞。此外,內部人士一直在忙於增加他們在公司的大量持股。光是這些因素就使該公司成爲您的關注清單和持續研究的有趣前景。那風險呢?每家公司都有它們,我們發現了傑克遜金融的兩個警告信號(其中一個很重要!)你應該知道。

Keen growth investors love to see insider buying. Thankfully, Jackson Financial isn't the only one. You can see a a curated list of companies which have exhibited consistent growth accompanied by recent insider buying.

敏銳的成長型投資者喜歡看到內幕買盤。值得慶幸的是,傑克遜金融並不是唯一的。你可以看到一份精選的公司名單,這些公司表現出持續增長,同時還有近期的內幕收購。

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

請注意,本文中討論的內幕交易是指相關司法管轄區內應報告的交易。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對這篇文章有反饋嗎?對內容感到擔憂?直接聯繫我們。 或者,給編輯團隊 (at) simplywallst.com 發送電子郵件。

Simply Wall St的這篇文章本質上是籠統的。我們僅使用公正的方法根據歷史數據和分析師的預測提供評論,我們的文章無意作爲財務建議。它不構成買入或賣出任何股票的建議,也沒有考慮到您的目標或財務狀況。我們的目標是爲您提供由基本數據驅動的長期重點分析。請注意,我們的分析可能不考慮最新的價格敏感型公司公告或定性材料。簡而言之,華爾街沒有持有任何上述股票的頭寸。

譯文內容由第三人軟體翻譯。