Increases to Intercontinental Exchange, Inc.'s (NYSE:ICE) CEO Compensation Might Cool off for Now

Increases to Intercontinental Exchange, Inc.'s (NYSE:ICE) CEO Compensation Might Cool off for Now

Key Insights

关键见解

- Intercontinental Exchange will host its Annual General Meeting on 17th of May

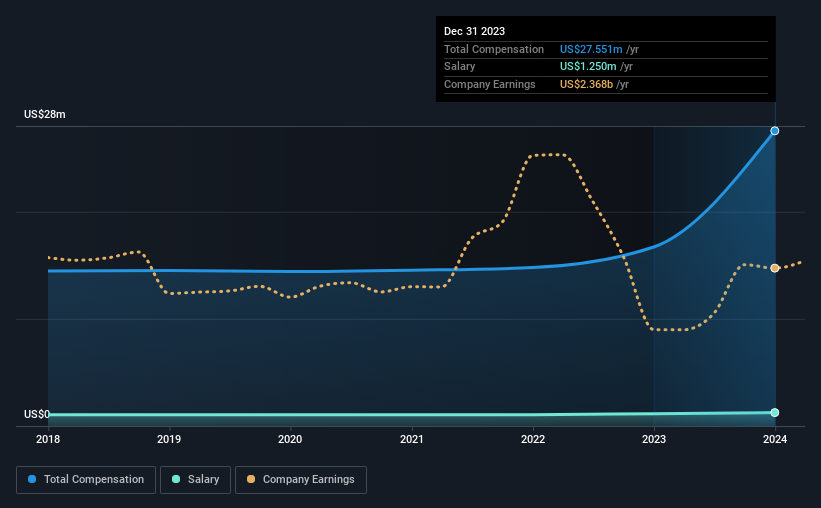

- Total pay for CEO Jeff Sprecher includes US$1.25m salary

- The total compensation is 63% higher than the average for the industry

- Intercontinental Exchange's total shareholder return over the past three years was 23% while its EPS grew by 4.8% over the past three years

- 洲际交易所将于5月17日举办年度股东大会

- 首席执行官杰夫·斯普雷彻的总薪水包括125万美元的工资

- 总薪酬比该行业的平均水平高63%

- 洲际交易所过去三年的股东总回报率为23%,而其每股收益在过去三年中增长了4.8%

CEO Jeff Sprecher has done a decent job of delivering relatively good performance at Intercontinental Exchange, Inc. (NYSE:ICE) recently. In light of this performance, CEO compensation will probably not be the main focus for shareholders as they go into the AGM on 17th of May. However, some shareholders may still be hesitant of being overly generous with CEO compensation.

首席执行官杰夫·斯普雷彻最近在洲际交易所公司(纽约证券交易所代码:ICE)取得了相对不错的业绩。鉴于这种表现,在股东将于5月17日参加股东周年大会之际,首席执行官薪酬可能不会成为他们的主要关注点。但是,一些股东可能仍对过于慷慨地提供首席执行官薪酬犹豫不决。

Comparing Intercontinental Exchange, Inc.'s CEO Compensation With The Industry

比较洲际交易所公司。”s 首席执行官向业界提供的薪酬

Our data indicates that Intercontinental Exchange, Inc. has a market capitalization of US$77b, and total annual CEO compensation was reported as US$28m for the year to December 2023. Notably, that's an increase of 65% over the year before. We think total compensation is more important but our data shows that the CEO salary is lower, at US$1.3m.

我们的数据显示,洲际交易所的市值为770亿美元,截至2023年12月的一年中,首席执行官的年薪酬总额报告为2,800万美元。值得注意的是,这比上年增长了65%。我们认为总薪酬更为重要,但我们的数据显示,首席执行官的薪水较低,为130万美元。

On comparing similar companies in the American Capital Markets industry with market capitalizations above US$8.0b, we found that the median total CEO compensation was US$17m. This suggests that Jeff Sprecher is paid more than the median for the industry. Furthermore, Jeff Sprecher directly owns US$516m worth of shares in the company, implying that they are deeply invested in the company's success.

在比较美国资本市场行业中市值超过80亿美元的类似公司时,我们发现首席执行官的总薪酬中位数为1700万美元。这表明杰夫·斯普雷彻的薪水超过了该行业的中位数。此外,杰夫·斯普雷彻直接拥有该公司价值5.16亿美元的股份,这意味着他们对公司的成功进行了大量投资。

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | US$1.3m | US$1.2m | 5% |

| Other | US$26m | US$16m | 95% |

| Total Compensation | US$28m | US$17m | 100% |

| 组件 | 2023 | 2022 | 比例 (2023) |

| 工资 | 130 万美元 | 120 万美元 | 5% |

| 其他 | 2600 万美元 | 1600 万美元 | 95% |

| 总薪酬 | 280 万美元 | 1700 万美元 | 100% |

On an industry level, roughly 9% of total compensation represents salary and 91% is other remuneration. Intercontinental Exchange has chosen to walk a path less trodden, opting to compensate its CEO with less of a traditional salary and more non-salary rewards over the last year. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

在行业层面,总薪酬中约有9%代表工资,91%是其他薪酬。去年,洲际交易所选择走一条较少人走的道路,选择用较少的传统薪水和更多的非薪水奖励来补偿其首席执行官。如果非工资薪酬在总薪酬中占主导地位,则表明高管的薪水与公司业绩息息相关。

A Look at Intercontinental Exchange, Inc.'s Growth Numbers

看看洲际交易所公司。”s 增长数字

Intercontinental Exchange, Inc.'s earnings per share (EPS) grew 4.8% per year over the last three years. It achieved revenue growth of 15% over the last year.

洲际交易所有限公司在过去三年中,每股收益(EPS)每年增长4.8%。去年,它实现了15%的收入增长。

We think the revenue growth is good. And the improvement in EPSis modest but respectable. Although we'll stop short of calling the stock a top performer, we think the company has potential. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

我们认为收入增长良好。而且,每股收益指数的改善不大,但值得尊敬。尽管我们不会将该股称为表现最佳的股票,但我们认为该公司具有潜力。历史表现有时可以很好地衡量接下来会发生什么,但是如果你想展望公司的未来,你可能会对这种免费的分析师预测可视化感兴趣。

Has Intercontinental Exchange, Inc. Been A Good Investment?

洲际交易所是一项不错的投资吗?

With a total shareholder return of 23% over three years, Intercontinental Exchange, Inc. shareholders would, in general, be reasonably content. But they would probably prefer not to see CEO compensation far in excess of the median.

洲际交易所三年内股东总回报率为23%,总体而言,洲际交易所的股东会感到满意。但他们可能不希望看到首席执行官的薪酬远远超过中位数。

In Summary...

总而言之...

Intercontinental Exchange primarily uses non-salary benefits to reward its CEO. Given that the company's overall performance has been reasonable, the CEO remuneration policy might not be shareholders' central point of focus in the upcoming AGM. However, if the board proposes to increase the compensation, some shareholders might have questions given that the CEO is already being paid higher than the industry.

洲际交易所主要使用非薪金福利来奖励其首席执行官。鉴于公司的整体表现合理,首席执行官薪酬政策可能不是即将举行的股东周年大会的重点。但是,如果董事会提议增加薪酬,鉴于首席执行官的薪水已经高于该行业,一些股东可能会有疑问。

We can learn a lot about a company by studying its CEO compensation trends, along with looking at other aspects of the business. We identified 2 warning signs for Intercontinental Exchange (1 makes us a bit uncomfortable!) that you should be aware of before investing here.

通过研究一家公司的首席执行官薪酬趋势,以及研究业务的其他方面,我们可以学到很多关于公司的信息。我们为洲际交易所确定了两个警告信号(其中一个让我们有点不舒服!)在这里投资之前,您应该注意这一点。

Important note: Intercontinental Exchange is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

重要提示:洲际交易所是一只令人兴奋的股票,但我们知道投资者可能正在寻找未支配的资产负债表和丰厚的回报。你可能会在这份投资回报率高、负债低的有趣公司清单中找到更好的东西。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

对这篇文章有反馈吗?对内容感到担忧?直接联系我们。 或者,给编辑团队 (at) simplywallst.com 发送电子邮件。

Simply Wall St的这篇文章本质上是笼统的。我们仅使用公正的方法根据历史数据和分析师的预测提供评论,我们的文章无意作为财务建议。它不构成买入或卖出任何股票的建议,也没有考虑到您的目标或财务状况。我们的目标是为您提供由基本数据驱动的长期重点分析。请注意,我们的分析可能不考虑最新的价格敏感型公司公告或定性材料。简而言之,华尔街没有持有任何上述股票的头寸。

译文内容由第三方软件翻译。