Shareholders Would Enjoy A Repeat Of A. O. Smith's (NYSE:AOS) Recent Growth In Returns

Shareholders Would Enjoy A Repeat Of A. O. Smith's (NYSE:AOS) Recent Growth In Returns

If we want to find a stock that could multiply over the long term, what are the underlying trends we should look for? One common approach is to try and find a company with returns on capital employed (ROCE) that are increasing, in conjunction with a growing amount of capital employed. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. So when we looked at the ROCE trend of A. O. Smith (NYSE:AOS) we really liked what we saw.

如果我们想找到一只可以长期成倍增长的股票,我们应该寻找哪些潜在趋势?一种常见的方法是尝试找一家公司 回报 论资本使用率(ROCE)在增加的同时增长 金额 所用资本的比例。归根结底,这表明这是一家以不断提高的回报率对利润进行再投资的企业。因此,当我们观察A.O. Smith(纽约证券交易所代码:AOS)的投资回报率趋势时,我们真的很喜欢我们所看到的。

Return On Capital Employed (ROCE): What Is It?

资本使用回报率(ROCE):这是什么?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. Analysts use this formula to calculate it for A. O. Smith:

如果你以前没有与ROCE合作过,它会衡量公司从其业务中使用的资本中产生的 “回报”(税前利润)。分析师使用这个公式来计算 A. O. Smith 的值:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

已动用资本回报率 = 息税前收益 (EBIT) ¥(总资产-流动负债)

0.32 = US$746m ÷ (US$3.2b - US$883m) (Based on the trailing twelve months to March 2024).

0.32 = 7.46 亿美元 ÷(32 亿美元-8.83 亿美元) (基于截至2024年3月的过去十二个月)。

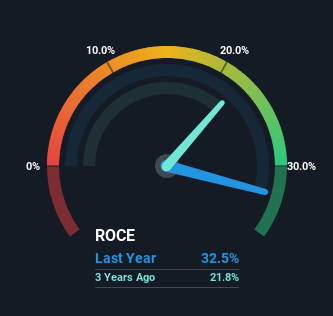

So, A. O. Smith has an ROCE of 32%. That's a fantastic return and not only that, it outpaces the average of 17% earned by companies in a similar industry.

因此,A.O.Smith的投资回报率为32%。这是一个了不起的回报,不仅如此,它还超过了同类行业公司平均收入的17%。

In the above chart we have measured A. O. Smith's prior ROCE against its prior performance, but the future is arguably more important. If you're interested, you can view the analysts predictions in our free analyst report for A. O. Smith .

在上图中,我们将A.O. Smith先前的投资回报率与之前的表现进行了对比,但可以说,未来更为重要。如果您有兴趣,可以在我们的A.O. Smith免费分析师报告中查看分析师的预测。

How Are Returns Trending?

退货趋势如何?

A. O. Smith is showing promise given that its ROCE is trending up and to the right. Looking at the data, we can see that even though capital employed in the business has remained relatively flat, the ROCE generated has risen by 48% over the last five years. So our take on this is that the business has increased efficiencies to generate these higher returns, all the while not needing to make any additional investments. The company is doing well in that sense, and it's worth investigating what the management team has planned for long term growth prospects.

鉴于其投资回报率呈上升和向右倾斜的趋势,A.O. Smith表现出希望。从数据来看,我们可以看到,尽管该业务中使用的资本保持相对平稳,但在过去五年中,产生的投资回报率增长了48%。因此,我们的看法是,企业提高了效率以产生更高的回报,同时无需进行任何额外投资。从这个意义上讲,该公司表现良好,值得研究管理团队对长期增长前景的计划。

What We Can Learn From A. O. Smith's ROCE

我们可以从 A.O. Smith 的 ROCE 中学到什么

To bring it all together, A. O. Smith has done well to increase the returns it's generating from its capital employed. And investors seem to expect more of this going forward, since the stock has rewarded shareholders with a 94% return over the last five years. In light of that, we think it's worth looking further into this stock because if A. O. Smith can keep these trends up, it could have a bright future ahead.

综上所述,A.O. Smith在提高其使用资本产生的回报方面做得很好。投资者似乎对未来有更多这样的期望,因为该股在过去五年中为股东提供了94%的回报。有鉴于此,我们认为值得进一步研究这只股票,因为如果A. O. Smith能够保持这些趋势,那么它的前途可能会很光明。

While A. O. Smith looks impressive, no company is worth an infinite price. The intrinsic value infographic for AOS helps visualize whether it is currently trading for a fair price.

尽管A.O.Smith看上去令人印象深刻,但没有一家公司值得付出无限的代价。AOS 的内在价值信息图有助于可视化其当前是否以公平的价格进行交易。

If you'd like to see other companies earning high returns, check out our free list of companies earning high returns with solid balance sheets here.

如果您想看到其他公司获得高回报,请在此处查看我们的免费高回报且资产负债表稳健的公司名单。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

对这篇文章有反馈吗?对内容感到担忧?直接联系我们。 或者,给编辑团队 (at) simplywallst.com 发送电子邮件。

Simply Wall St的这篇文章本质上是笼统的。我们仅使用公正的方法根据历史数据和分析师的预测提供评论,我们的文章无意作为财务建议。它不构成买入或卖出任何股票的建议,也没有考虑到您的目标或财务状况。我们的目标是为您提供由基本数据驱动的长期重点分析。请注意,我们的分析可能不考虑最新的价格敏感型公司公告或定性材料。简而言之,华尔街没有持有任何上述股票的头寸。

译文内容由第三方软件翻译。