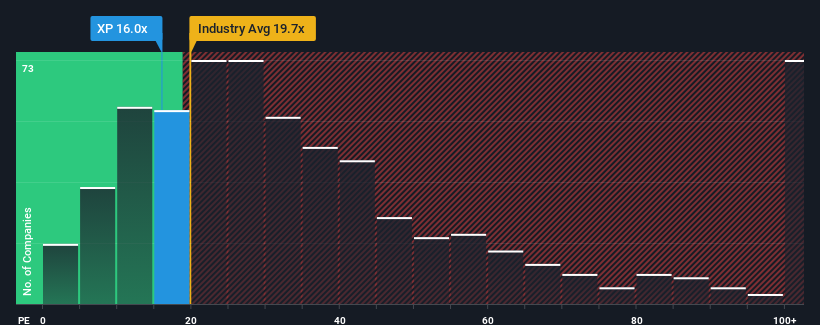

It's not a stretch to say that XP Inc.'s (NASDAQ:XP) price-to-earnings (or "P/E") ratio of 16x right now seems quite "middle-of-the-road" compared to the market in the United States, where the median P/E ratio is around 17x. Although, it's not wise to simply ignore the P/E without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

Recent times have been pleasing for XP as its earnings have risen in spite of the market's earnings going into reverse. One possibility is that the P/E is moderate because investors think the company's earnings will be less resilient moving forward. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's not quite in favour.

NasdaqGS:XP Price to Earnings Ratio vs Industry May 6th 2024 If you'd like to see what analysts are forecasting going forward, you should check out our free report on XP.

Is There Some Growth For XP?

There's an inherent assumption that a company should be matching the market for P/E ratios like XP's to be considered reasonable.

Retrospectively, the last year delivered a decent 12% gain to the company's bottom line. This was backed up an excellent period prior to see EPS up by 89% in total over the last three years. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Looking ahead now, EPS is anticipated to climb by 17% each year during the coming three years according to the eight analysts following the company. That's shaping up to be materially higher than the 10% per annum growth forecast for the broader market.

In light of this, it's curious that XP's P/E sits in line with the majority of other companies. It may be that most investors aren't convinced the company can achieve future growth expectations.

What We Can Learn From XP's P/E?

We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Our examination of XP's analyst forecasts revealed that its superior earnings outlook isn't contributing to its P/E as much as we would have predicted. There could be some unobserved threats to earnings preventing the P/E ratio from matching the positive outlook. It appears some are indeed anticipating earnings instability, because these conditions should normally provide a boost to the share price.

It is also worth noting that we have found 1 warning sign for XP that you need to take into consideration.

You might be able to find a better investment than XP. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

说 XP Inc. 并不夸张。”与市盈率中位数约为17倍的美国市场相比,s(纳斯达克股票代码:XP)市盈率(或 “市盈率”)目前的16倍似乎相当 “中间路段”。但是,不加解释地忽略市盈率是不明智的,因为投资者可能无视一个特殊的机会或一个代价高昂的错误。