Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Jiangsu Lopal Tech. Co., Ltd. (SHSE:603906) does carry debt. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company's use of debt, we first look at cash and debt together.

How Much Debt Does Jiangsu Lopal Tech Carry?

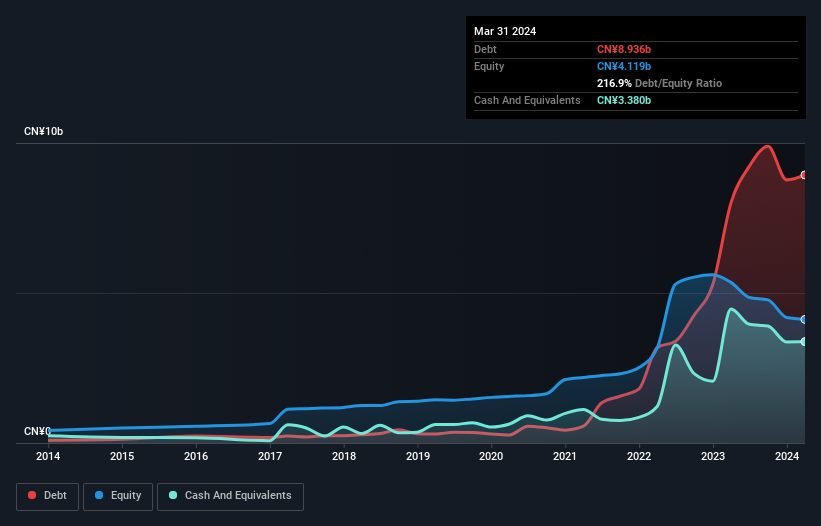

As you can see below, at the end of March 2024, Jiangsu Lopal Tech had CN¥8.94b of debt, up from CN¥8.00b a year ago. Click the image for more detail. However, because it has a cash reserve of CN¥3.38b, its net debt is less, at about CN¥5.56b.

A Look At Jiangsu Lopal Tech's Liabilities

Zooming in on the latest balance sheet data, we can see that Jiangsu Lopal Tech had liabilities of CN¥9.38b due within 12 months and liabilities of CN¥4.02b due beyond that. On the other hand, it had cash of CN¥3.38b and CN¥2.25b worth of receivables due within a year. So it has liabilities totalling CN¥7.78b more than its cash and near-term receivables, combined.

When you consider that this deficiency exceeds the company's CN¥5.49b market capitalization, you might well be inclined to review the balance sheet intently. Hypothetically, extremely heavy dilution would be required if the company were forced to pay down its liabilities by raising capital at the current share price. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Jiangsu Lopal Tech can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

In the last year Jiangsu Lopal Tech had a loss before interest and tax, and actually shrunk its revenue by 40%, to CN¥8.1b. To be frank that doesn't bode well.

Caveat Emptor

Not only did Jiangsu Lopal Tech's revenue slip over the last twelve months, but it also produced negative earnings before interest and tax (EBIT). Its EBIT loss was a whopping CN¥930m. When we look at that alongside the significant liabilities, we're not particularly confident about the company. It would need to improve its operations quickly for us to be interested in it. Not least because it burned through CN¥716m in negative free cash flow over the last year. So suffice it to say we consider the stock to be risky. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. We've identified 2 warning signs with Jiangsu Lopal Tech , and understanding them should be part of your investment process.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.