Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that Expro Group Holdings N.V. (NYSE:XPRO) does use debt in its business. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

What Is Expro Group Holdings's Net Debt?

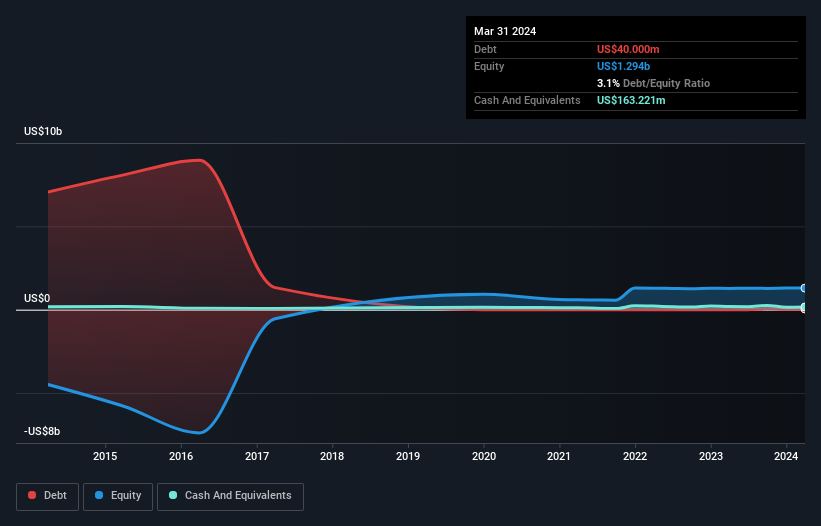

As you can see below, at the end of March 2024, Expro Group Holdings had US$40.0m of debt, up from none a year ago. Click the image for more detail. But it also has US$163.2m in cash to offset that, meaning it has US$123.2m net cash.

How Healthy Is Expro Group Holdings' Balance Sheet?

The latest balance sheet data shows that Expro Group Holdings had liabilities of US$465.8m due within a year, and liabilities of US$240.4m falling due after that. Offsetting this, it had US$163.2m in cash and US$467.9m in receivables that were due within 12 months. So it has liabilities totalling US$75.0m more than its cash and near-term receivables, combined.

Of course, Expro Group Holdings has a market capitalization of US$2.10b, so these liabilities are probably manageable. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time. Despite its noteworthy liabilities, Expro Group Holdings boasts net cash, so it's fair to say it does not have a heavy debt load!

On top of that, Expro Group Holdings grew its EBIT by 39% over the last twelve months, and that growth will make it easier to handle its debt. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Expro Group Holdings's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. While Expro Group Holdings has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. In the last two years, Expro Group Holdings's free cash flow amounted to 46% of its EBIT, less than we'd expect. That weak cash conversion makes it more difficult to handle indebtedness.

Summing Up

We could understand if investors are concerned about Expro Group Holdings's liabilities, but we can be reassured by the fact it has has net cash of US$123.2m. And we liked the look of last year's 39% year-on-year EBIT growth. So we don't think Expro Group Holdings's use of debt is risky. We'd be motivated to research the stock further if we found out that Expro Group Holdings insiders have bought shares recently. If you would too, then you're in luck, since today we're sharing our list of reported insider transactions for free.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.