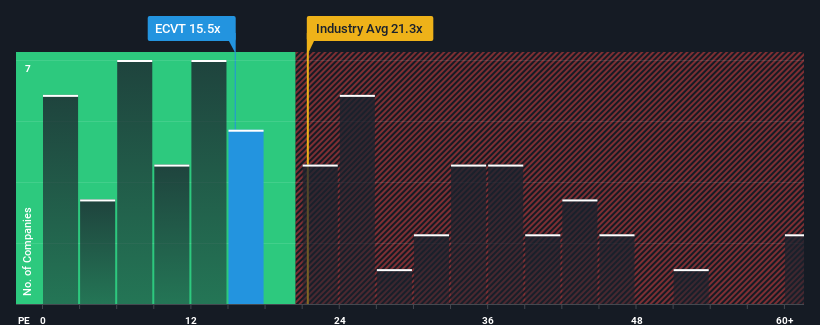

There wouldn't be many who think Ecovyst Inc.'s (NYSE:ECVT) price-to-earnings (or "P/E") ratio of 15.5x is worth a mention when the median P/E in the United States is similar at about 17x. Although, it's not wise to simply ignore the P/E without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

Ecovyst certainly has been doing a good job lately as its earnings growth has been positive while most other companies have been seeing their earnings go backwards. It might be that many expect the strong earnings performance to deteriorate like the rest, which has kept the P/E from rising. If not, then existing shareholders have reason to be feeling optimistic about the future direction of the share price.

NYSE:ECVT Price to Earnings Ratio vs Industry May 1st 2024 Keen to find out how analysts think Ecovyst's future stacks up against the industry? In that case, our free report is a great place to start.

Is There Some Growth For Ecovyst?

In order to justify its P/E ratio, Ecovyst would need to produce growth that's similar to the market.

If we review the last year of earnings growth, the company posted a terrific increase of 15%. Pleasingly, EPS has also lifted 52% in aggregate from three years ago, thanks to the last 12 months of growth. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Turning to the outlook, the next three years should generate growth of 27% per year as estimated by the six analysts watching the company. Meanwhile, the rest of the market is forecast to only expand by 11% per year, which is noticeably less attractive.

In light of this, it's curious that Ecovyst's P/E sits in line with the majority of other companies. Apparently some shareholders are skeptical of the forecasts and have been accepting lower selling prices.

The Key Takeaway

Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We've established that Ecovyst currently trades on a lower than expected P/E since its forecast growth is higher than the wider market. There could be some unobserved threats to earnings preventing the P/E ratio from matching the positive outlook. At least the risk of a price drop looks to be subdued, but investors seem to think future earnings could see some volatility.

It is also worth noting that we have found 2 warning signs for Ecovyst (1 makes us a bit uncomfortable!) that you need to take into consideration.

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with a strong growth track record, trading on a low P/E.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

想到 Ecovyst Inc. 的人不会很多。”s(纽约证券交易所代码:ECVT)市盈率(或 “市盈率”)15.5倍值得一提,因为美国的市盈率中位数相似,约为17倍。但是,不加解释地忽略市盈率是不明智的,因为投资者可能无视一个特殊的机会或一个代价高昂的错误。