Here's Why We Think Saia (NASDAQ:SAIA) Is Well Worth Watching

Here's Why We Think Saia (NASDAQ:SAIA) Is Well Worth Watching

The excitement of investing in a company that can reverse its fortunes is a big draw for some speculators, so even companies that have no revenue, no profit, and a record of falling short, can manage to find investors. But the reality is that when a company loses money each year, for long enough, its investors will usually take their share of those losses. Loss-making companies are always racing against time to reach financial sustainability, so investors in these companies may be taking on more risk than they should.

對一些投機者來說,投資一家能夠扭轉命運的公司的興奮感是一個很大的吸引力,因此,即使是沒有收入、沒有利潤、有虧損記錄的公司,也可以設法找到投資者。但現實是,當一家公司每年虧損時,在足夠長的時間內,其投資者通常會從虧損中分擔自己的份額。虧損的公司總是與時間賽跑以實現財務可持續性,因此這些公司的投資者承擔的風險可能超出了應有的範圍。

So if this idea of high risk and high reward doesn't suit, you might be more interested in profitable, growing companies, like Saia (NASDAQ:SAIA). While profit isn't the sole metric that should be considered when investing, it's worth recognising businesses that can consistently produce it.

因此,如果這種高風險和高回報的想法不適合,你可能會對像Saia(納斯達克股票代碼:SAIA)這樣盈利的成長型公司更感興趣。儘管利潤不是投資時應考慮的唯一指標,但值得表彰能夠持續生產利潤的企業。

How Quickly Is Saia Increasing Earnings Per Share?

Saia 增加每股收益的速度有多快?

Generally, companies experiencing growth in earnings per share (EPS) should see similar trends in share price. So it makes sense that experienced investors pay close attention to company EPS when undertaking investment research. Shareholders will be happy to know that Saia's EPS has grown 35% each year, compound, over three years. As a general rule, we'd say that if a company can keep up that sort of growth, shareholders will be beaming.

通常,每股收益(EPS)增長的公司的股價應該會出現類似的趨勢。因此,經驗豐富的投資者在進行投資研究時密切關注公司的每股收益是有道理的。股東們會很高興得知Saia的每股收益在三年內複合每年增長35%。一般來說,如果一家公司能跟上步伐,我們會這麼說 那個 有點像增長,股東們會喜氣洋洋。

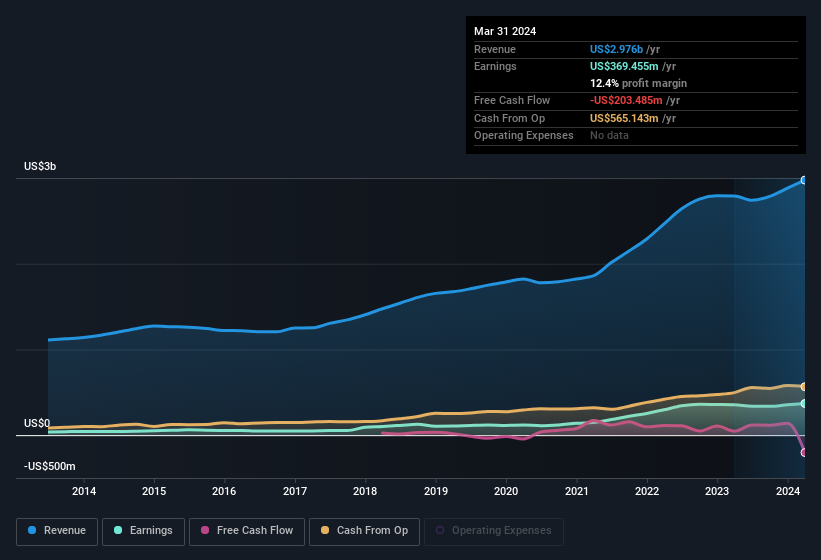

Top-line growth is a great indicator that growth is sustainable, and combined with a high earnings before interest and taxation (EBIT) margin, it's a great way for a company to maintain a competitive advantage in the market. EBIT margins for Saia remained fairly unchanged over the last year, however the company should be pleased to report its revenue growth for the period of 6.6% to US$3.0b. That's encouraging news for the company!

收入增長是可持續增長的重要指標,再加上較高的息稅前收益(EBIT)利潤率,這是公司保持市場競爭優勢的好方法。去年,Saia的息稅前利潤率基本保持不變,但該公司應該很高興地報告其收入增長6.6%至30億美元。這對公司來說是個令人鼓舞的消息!

You can take a look at the company's revenue and earnings growth trend, in the chart below. To see the actual numbers, click on the chart.

您可以在下表中查看該公司的收入和收益增長趨勢。要查看實際數字,請單擊圖表。

While we live in the present moment, there's little doubt that the future matters most in the investment decision process. So why not check this interactive chart depicting future EPS estimates, for Saia?

雖然我們生活在當下,但毫無疑問,未來在投資決策過程中最重要。那麼,爲什麼不查看這張描繪Saia未來每股收益估計值的交互式圖表呢?

Are Saia Insiders Aligned With All Shareholders?

Saia 內部人士是否與所有股東保持一致?

Owing to the size of Saia, we wouldn't expect insiders to hold a significant proportion of the company. But thanks to their investment in the company, it's pleasing to see that there are still incentives to align their actions with the shareholders. To be specific, they have US$28m worth of shares. That shows significant buy-in, and may indicate conviction in the business strategy. While their ownership only accounts for 0.2%, this is still a considerable amount at stake to encourage the business to maintain a strategy that will deliver value to shareholders.

由於Saia的規模,我們預計內部人士不會持有該公司的很大一部分股份。但是,由於他們對公司的投資,令人高興的是,仍然有激勵措施使他們的行動與股東保持一致。具體而言,他們擁有價值2800萬美元的股票。這表明了大量的支持,也可能表明對業務戰略的信念。儘管他們的所有權僅佔0.2%,但要鼓勵企業維持爲股東創造價值的戰略,這仍然是一個相當大的風險。

It's good to see that insiders are invested in the company, but are remuneration levels reasonable? Our quick analysis into CEO remuneration would seem to indicate they are. Our analysis has discovered that the median total compensation for the CEOs of companies like Saia, with market caps over US$8.0b, is about US$14m.

很高興看到內部人士投資於公司,但是薪酬水平是否合理?我們對首席執行官薪酬的快速分析似乎表明確實如此。我們的分析發現,市值超過80億美元的Saia等公司的首席執行官的總薪酬中位數約爲1400萬美元。

The Saia CEO received total compensation of just US$5.7m in the year to December 2023. That looks like a modest pay packet, and may hint at a certain respect for the interests of shareholders. CEO remuneration levels are not the most important metric for investors, but when the pay is modest, that does support enhanced alignment between the CEO and the ordinary shareholders. It can also be a sign of a culture of integrity, in a broader sense.

截至2023年12月的一年中,Saia首席執行官的總薪酬僅爲570萬美元。這看起來像是微不足道的工資待遇,可能暗示着對股東利益的某種尊重。首席執行官薪酬水平並不是投資者最重要的指標,但是當薪酬適度時,這確實支持加強首席執行官與普通股東之間的協調。從更廣泛的意義上講,它也可以是誠信文化的標誌。

Does Saia Deserve A Spot On Your Watchlist?

Saia 值得在你的關注名單上佔有一席之地嗎?

If you believe that share price follows earnings per share you should definitely be delving further into Saia's strong EPS growth. If you still have your doubts, remember too that company insiders have a considerable investment aligning themselves with the shareholders and CEO pay is quite modest compared to similarly sized companiess. This may only be a fast rundown, but the key takeaway is that Saia is worth keeping an eye on. Even so, be aware that Saia is showing 2 warning signs in our investment analysis , and 1 of those makes us a bit uncomfortable...

如果你認爲股價跟隨每股收益,那麼你肯定應該進一步研究Saia強勁的每股收益增長。如果你還有疑問,還要記住,公司內部人士有大量的投資與股東保持一致,與類似規模的公司相比,首席執行官的薪酬相當適中。這可能只是一個簡短的概述,但關鍵要點是賽亞值得關注。即便如此,請注意,Saia在我們的投資分析中顯示了2個警告信號,其中一個讓我們有點不舒服...

While opting for stocks without growing earnings and absent insider buying can yield results, for investors valuing these key metrics, here is a carefully selected list of companies in the US with promising growth potential and insider confidence.

雖然選擇收益不增長且沒有內幕買盤的股票可以產生業績,但對於估值這些關鍵指標的投資者來說,以下是精心挑選的具有良好增長潛力和內部信心的美國公司名單。

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

請注意,本文中討論的內幕交易是指相關司法管轄區內應報告的交易。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對這篇文章有反饋嗎?對內容感到擔憂?直接聯繫我們。 或者,給編輯團隊 (at) simplywallst.com 發送電子郵件。

Simply Wall St的這篇文章本質上是籠統的。我們僅使用公正的方法根據歷史數據和分析師的預測提供評論,我們的文章無意作爲財務建議。它不構成買入或賣出任何股票的建議,也沒有考慮到您的目標或財務狀況。我們的目標是爲您提供由基本數據驅動的長期重點分析。請注意,我們的分析可能不考慮最新的價格敏感型公司公告或定性材料。簡而言之,華爾街沒有持有任何上述股票的頭寸。

譯文內容由第三人軟體翻譯。