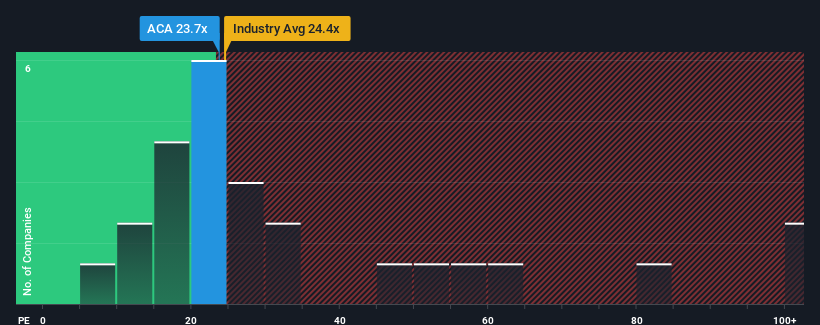

Arcosa, Inc.'s (NYSE:ACA) price-to-earnings (or "P/E") ratio of 23.7x might make it look like a sell right now compared to the market in the United States, where around half of the companies have P/E ratios below 16x and even P/E's below 9x are quite common. However, the P/E might be high for a reason and it requires further investigation to determine if it's justified.

Arcosa has been struggling lately as its earnings have declined faster than most other companies. One possibility is that the P/E is high because investors think the company will turn things around completely and accelerate past most others in the market. If not, then existing shareholders may be very nervous about the viability of the share price.

NYSE:ACA Price to Earnings Ratio vs Industry April 29th 2024 Want the full picture on analyst estimates for the company? Then our free report on Arcosa will help you uncover what's on the horizon.

How Is Arcosa's Growth Trending?

In order to justify its P/E ratio, Arcosa would need to produce impressive growth in excess of the market.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 36%. Still, the latest three year period has seen an excellent 48% overall rise in EPS, in spite of its unsatisfying short-term performance. Although it's been a bumpy ride, it's still fair to say the earnings growth recently has been more than adequate for the company.

Shifting to the future, estimates from the five analysts covering the company suggest earnings should grow by 0.1% over the next year. That's shaping up to be materially lower than the 12% growth forecast for the broader market.

In light of this, it's alarming that Arcosa's P/E sits above the majority of other companies. Apparently many investors in the company are way more bullish than analysts indicate and aren't willing to let go of their stock at any price. There's a good chance these shareholders are setting themselves up for future disappointment if the P/E falls to levels more in line with the growth outlook.

The Key Takeaway

Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Arcosa currently trades on a much higher than expected P/E since its forecast growth is lower than the wider market. Right now we are increasingly uncomfortable with the high P/E as the predicted future earnings aren't likely to support such positive sentiment for long. Unless these conditions improve markedly, it's very challenging to accept these prices as being reasonable.

Don't forget that there may be other risks. For instance, we've identified 2 warning signs for Arcosa that you should be aware of.

You might be able to find a better investment than Arcosa. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Arcosa, Inc. 's(紐約證券交易所代碼:ACA)市盈率(或 “市盈率”)爲23.7倍,與美國市場相比,目前可能看起來像賣出。在美國,約有一半公司的市盈率低於16倍,甚至市盈率低於9倍也很常見。但是,市盈率之高可能是有原因的,需要進一步調查以確定其是否合理。