Shanying International Holdings Co.,Ltd (SHSE:600567) Analysts Are More Bearish Than They Used To Be

Shanying International Holdings Co.,Ltd (SHSE:600567) Analysts Are More Bearish Than They Used To Be

The latest analyst coverage could presage a bad day for Shanying International Holdings Co.,Ltd (SHSE:600567), with the analysts making across-the-board cuts to their statutory estimates that might leave shareholders a little shell-shocked. Both revenue and earnings per share (EPS) forecasts went under the knife, suggesting analysts have soured majorly on the business.

分析师的最新报道可能预示着山鹰国际控股有限公司将迎来糟糕的一天。, Ltd(上海证券交易所代码:600567),分析师全面下调了法定预算,这可能会让股东感到震惊。收入和每股收益(EPS)的预测都出现了偏差,这表明分析师对该业务的表现主要不佳。

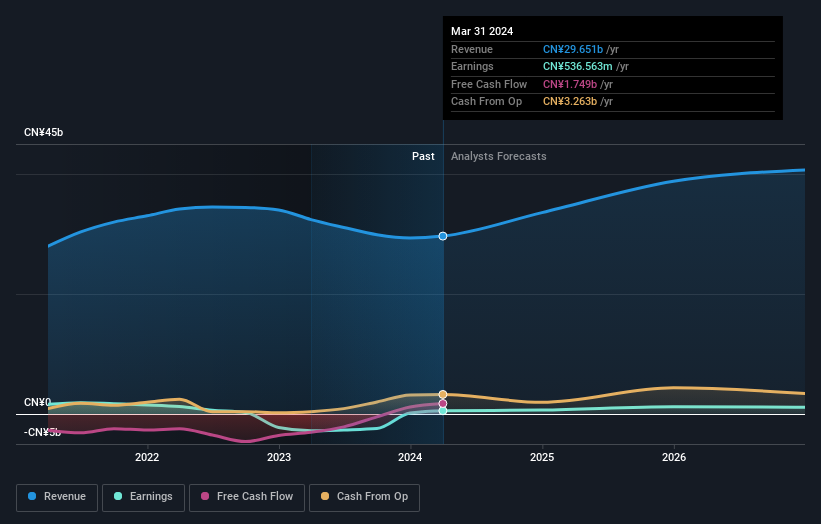

Following the downgrade, the current consensus from Shanying International HoldingsLtd's seven analysts is for revenues of CN¥34b in 2024 which - if met - would reflect a notable 13% increase on its sales over the past 12 months. Per-share earnings are expected to jump 34% to CN¥0.17. Previously, the analysts had been modelling revenues of CN¥37b and earnings per share (EPS) of CN¥0.22 in 2024. It looks like analyst sentiment has declined substantially, with a substantial drop in revenue estimates and a large cut to earnings per share numbers as well.

降级之后,山鹰国际控股有限公司的七位分析师目前的共识是,2024年的收入为340亿元人民币,如果达到,这将反映出其在过去12个月中销售额的显著增长13%。每股收益预计将增长34%,至0.17元人民币。此前,分析师一直在模拟2024年的收入为370亿元人民币,每股收益(EPS)为0.22元人民币。看来分析师的情绪已大幅下降,收入预期大幅下降,每股收益也大幅下调。

The consensus price target fell 7.1% to CN¥2.14, with the weaker earnings outlook clearly leading analyst valuation estimates.

共识目标股价下跌7.1%,至2.14元人民币,疲软的盈利前景显然领先于分析师的估值预期。

Of course, another way to look at these forecasts is to place them into context against the industry itself. It's clear from the latest estimates that Shanying International HoldingsLtd's rate of growth is expected to accelerate meaningfully, with the forecast 13% annualised revenue growth to the end of 2024 noticeably faster than its historical growth of 7.7% p.a. over the past five years. Compare this with other companies in the same industry, which are forecast to grow their revenue 13% annually. Shanying International HoldingsLtd is expected to grow at about the same rate as its industry, so it's not clear that we can draw any conclusions from its growth relative to competitors.

当然,看待这些预测的另一种方法是将它们与行业本身联系起来。从最新估计中可以明显看出,山鹰国际控股有限公司的增长率预计将大幅加速,预计到2024年底的年化收入增长为13%,明显快于其过去五年中每年7.7%的历史增长。相比之下,同行业的其他公司预计收入每年将增长13%。预计山鹰国际控股有限公司的增长速度将与其行业大致相同,因此目前尚不清楚我们能否从其相对于竞争对手的增长中得出任何结论。

The Bottom Line

底线

The most important thing to take away is that analysts cut their earnings per share estimates, expecting a clear decline in business conditions. There was also a drop in their revenue estimates, although as we saw earlier, forecast growth is only expected to be about the same as the wider market. With a serious cut to this year's expectations and a falling price target, we wouldn't be surprised if investors were becoming wary of Shanying International HoldingsLtd.

要了解的最重要的一点是,分析师下调了每股收益预期,预计业务状况将明显下降。他们的收入估计也有所下降,尽管正如我们之前看到的那样,预计增长仅与整个市场大致相同。随着今年的预期大幅下调和目标股价的下降,如果投资者对山鹰国际控股有限公司保持警惕,我们也不会感到惊讶。

Even so, the longer term trajectory of the business is much more important for the value creation of shareholders. We have estimates - from multiple Shanying International HoldingsLtd analysts - going out to 2026, and you can see them free on our platform here.

即便如此,业务的长期发展轨迹对于股东的价值创造更为重要。根据多位山英国际控股有限公司分析师的估计,预计将持续到2026年,你可以在这里在我们的平台上免费查看。

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are downgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

当然,看到公司管理层将大量资金投资于股票与了解分析师是否在下调预期一样有用。因此,您可能还希望搜索这份内部人士正在购买的免费股票清单。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

对这篇文章有反馈吗?对内容感到担忧?直接联系我们。 或者,给编辑团队 (at) simplywallst.com 发送电子邮件。

Simply Wall St的这篇文章本质上是笼统的。我们仅使用公正的方法根据历史数据和分析师的预测提供评论,我们的文章无意作为财务建议。它不构成买入或卖出任何股票的建议,也没有考虑到您的目标或财务状况。我们的目标是为您提供由基本数据驱动的长期重点分析。请注意,我们的分析可能不考虑最新的价格敏感型公司公告或定性材料。简而言之,华尔街没有持有任何上述股票的头寸。

译文内容由第三方软件翻译。