An Intrinsic Calculation For The Kroger Co. (NYSE:KR) Suggests It's 40% Undervalued

An Intrinsic Calculation For The Kroger Co. (NYSE:KR) Suggests It's 40% Undervalued

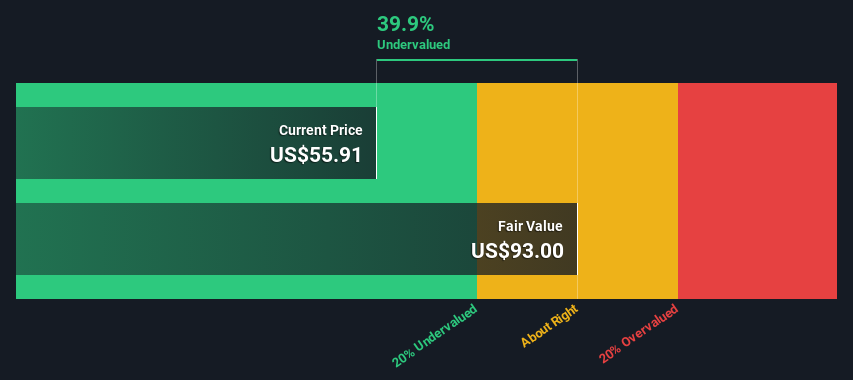

Key Insights

- The projected fair value for Kroger is US$93.00 based on 2 Stage Free Cash Flow to Equity

- Kroger's US$55.91 share price signals that it might be 40% undervalued

- Analyst price target for KR is US$58.21 which is 37% below our fair value estimate

Today we will run through one way of estimating the intrinsic value of The Kroger Co. (NYSE:KR) by taking the expected future cash flows and discounting them to today's value. The Discounted Cash Flow (DCF) model is the tool we will apply to do this. Models like these may appear beyond the comprehension of a lay person, but they're fairly easy to follow.

We would caution that there are many ways of valuing a company and, like the DCF, each technique has advantages and disadvantages in certain scenarios. Anyone interested in learning a bit more about intrinsic value should have a read of the Simply Wall St analysis model.

What's The Estimated Valuation?

We use what is known as a 2-stage model, which simply means we have two different periods of growth rates for the company's cash flows. Generally the first stage is higher growth, and the second stage is a lower growth phase. To start off with, we need to estimate the next ten years of cash flows. Where possible we use analyst estimates, but when these aren't available we extrapolate the previous free cash flow (FCF) from the last estimate or reported value. We assume companies with shrinking free cash flow will slow their rate of shrinkage, and that companies with growing free cash flow will see their growth rate slow, over this period. We do this to reflect that growth tends to slow more in the early years than it does in later years.

A DCF is all about the idea that a dollar in the future is less valuable than a dollar today, so we need to discount the sum of these future cash flows to arrive at a present value estimate:

10-year free cash flow (FCF) estimate

| 2024 | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | 2033 | |

| Levered FCF ($, Millions) | US$2.56b | US$2.67b | US$3.25b | US$3.29b | US$3.63b | US$3.12b | US$3.14b | US$3.17b | US$3.21b | US$3.27b |

| Growth Rate Estimate Source | Analyst x5 | Analyst x6 | Analyst x6 | Analyst x5 | Analyst x2 | Analyst x1 | Est @ 0.55% | Est @ 1.07% | Est @ 1.44% | Est @ 1.69% |

| Present Value ($, Millions) Discounted @ 6.3% | US$2.4k | US$2.4k | US$2.7k | US$2.6k | US$2.7k | US$2.2k | US$2.0k | US$1.9k | US$1.8k | US$1.8k |

("Est" = FCF growth rate estimated by Simply Wall St)

Present Value of 10-year Cash Flow (PVCF) = US$22b

The second stage is also known as Terminal Value, this is the business's cash flow after the first stage. For a number of reasons a very conservative growth rate is used that cannot exceed that of a country's GDP growth. In this case we have used the 5-year average of the 10-year government bond yield (2.3%) to estimate future growth. In the same way as with the 10-year 'growth' period, we discount future cash flows to today's value, using a cost of equity of 6.3%.

Terminal Value (TV)= FCF2033 × (1 + g) ÷ (r – g) = US$3.3b× (1 + 2.3%) ÷ (6.3%– 2.3%) = US$83b

Present Value of Terminal Value (PVTV)= TV / (1 + r)10= US$83b÷ ( 1 + 6.3%)10= US$45b

The total value, or equity value, is then the sum of the present value of the future cash flows, which in this case is US$67b. To get the intrinsic value per share, we divide this by the total number of shares outstanding. Compared to the current share price of US$55.9, the company appears quite undervalued at a 40% discount to where the stock price trades currently. Remember though, that this is just an approximate valuation, and like any complex formula - garbage in, garbage out.

Important Assumptions

We would point out that the most important inputs to a discounted cash flow are the discount rate and of course the actual cash flows. You don't have to agree with these inputs, I recommend redoing the calculations yourself and playing with them. The DCF also does not consider the possible cyclicality of an industry, or a company's future capital requirements, so it does not give a full picture of a company's potential performance. Given that we are looking at Kroger as potential shareholders, the cost of equity is used as the discount rate, rather than the cost of capital (or weighted average cost of capital, WACC) which accounts for debt. In this calculation we've used 6.3%, which is based on a levered beta of 0.880. Beta is a measure of a stock's volatility, compared to the market as a whole. We get our beta from the industry average beta of globally comparable companies, with an imposed limit between 0.8 and 2.0, which is a reasonable range for a stable business.

SWOT Analysis for Kroger

- Debt is well covered by earnings and cashflows.

- Dividends are covered by earnings and cash flows.

- Dividend information for KR.

- Earnings declined over the past year.

- Dividend is low compared to the top 25% of dividend payers in the Consumer Retailing market.

- Annual earnings are forecast to grow for the next 3 years.

- Good value based on P/E ratio and estimated fair value.

- Annual earnings are forecast to grow slower than the American market.

- What else are analysts forecasting for KR?

Moving On:

Valuation is only one side of the coin in terms of building your investment thesis, and it shouldn't be the only metric you look at when researching a company. The DCF model is not a perfect stock valuation tool. Instead the best use for a DCF model is to test certain assumptions and theories to see if they would lead to the company being undervalued or overvalued. If a company grows at a different rate, or if its cost of equity or risk free rate changes sharply, the output can look very different. Why is the intrinsic value higher than the current share price? For Kroger, we've compiled three fundamental factors you should assess:

- Risks: Consider for instance, the ever-present spectre of investment risk. We've identified 2 warning signs with Kroger , and understanding these should be part of your investment process.

- Future Earnings: How does KR's growth rate compare to its peers and the wider market? Dig deeper into the analyst consensus number for the upcoming years by interacting with our free analyst growth expectation chart.

- Other Solid Businesses: Low debt, high returns on equity and good past performance are fundamental to a strong business. Why not explore our interactive list of stocks with solid business fundamentals to see if there are other companies you may not have considered!

PS. Simply Wall St updates its DCF calculation for every American stock every day, so if you want to find the intrinsic value of any other stock just search here.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

關鍵見解

- 根據兩階段股權自由現金流,克羅格的預計公允價值爲93.00美元

- 克羅格55.91美元的股價表明其估值可能被低估了40%

- 分析師對韓元的目標股價爲58.21美元,比我們的公允價值估計低37%

今天,我們將介紹一種估算克羅格公司內在價值的方法。(紐約證券交易所代碼:KR)通過計算預期的未來現金流並將其折現爲今天的價值。折扣現金流(DCF)模型是我們將應用的工具。像這樣的模型可能看起來超出外行人的理解,但它們很容易理解。

我們要提醒的是,對公司進行估值的方法有很多,就像DCF一樣,每種技術在某些情況下都有優點和缺點。任何有興趣進一步了解內在價值的人都應該讀一讀 Simply Wall St 分析模型。

估計估值是多少?

我們使用所謂的兩階段模型,這僅意味着公司的現金流有兩個不同的增長期。通常,第一階段是較高的增長階段,第二階段是較低的增長階段。首先,我們需要估計未來十年的現金流。在可能的情況下,我們會使用分析師的估計值,但是當這些估計值不可用時,我們會從最新的估計值或報告的價值中推斷出之前的自由現金流(FCF)。我們假設自由現金流萎縮的公司將減緩其萎縮速度,而自由現金流不斷增長的公司在此期間的增長率將放緩。我們這樣做是爲了反映早期增長的放緩幅度往往比後來的幾年更大。

差價合約完全是關於未來一美元的價值低於今天一美元的想法,因此我們需要對這些未來現金流的總和進行折現才能得出現值估計:

10 年自由現金流 (FCF) 估計

| 2024 | 2025 | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | 2033 | |

| Levered FCF(美元,百萬) | 25.6 億美元 | 26.7 億美元 | 32.5 億美元 | 32.9億美元 | 363 億美元 | 312 億美元 | 31.4 億美元 | 31.7 億美元 | 32.1 億美元 | 32.7 億美元 |

| 增長率估算來源 | 分析師 x5 | 分析師 x6 | 分析師 x6 | 分析師 x5 | 分析師 x2 | 分析師 x1 | Est @ 0.55% | 東部標準時間 @ 1.07% | Est @ 1.44% | 美國東部時間 @ 1.69% |

| 現值(美元,百萬)折扣 @ 6.3% | 2.4 萬美元 | 2.4 萬美元 | 27k 美元 | 2.6k 美元 | 27k 美元 | 2.2 萬美元 | 200 萬美元 | 19k 美元 | 180 萬美元 | 180 萬美元 |

(“Est” = Simply Wall St估計的FCF增長率)

十年期現金流(PVCF)的現值 = 220億美元

第二階段也稱爲終值,這是第一階段之後的企業現金流。出於多種原因,使用的增長率非常保守,不能超過一個國家的GDP增長。在這種情況下,我們使用10年期國債收益率的5年平均值(2.3%)來估計未來的增長。與10年 “增長” 期一樣,我們使用6.3%的股本成本將未來的現金流折現爲今天的價值。

終端價值 (TV) = FCF2033 × (1 + g) ÷ (r — g) = 33億美元× (1 + 2.3%) ÷ (6.3% — 2.3%) = 830億美元

終端價值的現值 (PVTV) = 電視/ (1 + r)10= 830億美元÷ (1 + 6.3%)10= 450 億美元

因此,總價值或權益價值是未來現金流現值的總和,在本例中爲670億美元。爲了得出每股內在價值,我們將其除以已發行股票總數。與目前的55.9美元股價相比,該公司的估值似乎被嚴重低估,比目前的股價折扣了40%。但請記住,這只是一個近似的估值,就像任何複雜的公式一樣,垃圾進出。

重要假設

我們要指出的是,貼現現金流的最重要投入是貼現率,當然還有實際的現金流。你不必同意這些輸入,我建議你自己重做計算然後試一試。DCF也沒有考慮一個行業可能的週期性,也沒有考慮公司未來的資本需求,因此它沒有全面反映公司的潛在表現。鑑於我們將克羅格視爲潛在股東,因此使用權益成本作爲貼現率,而不是構成債務的資本成本(或加權平均資本成本,WACC)。在此計算中,我們使用了6.3%,這是基於0.880的槓桿測試版。Beta是衡量股票與整個市場相比波動性的指標。我們的測試版來自全球可比公司的行業平均貝塔值,設定在0.8到2.0之間,這是一個穩定的業務的合理範圍。

克羅格的 SWOT 分析

- 收益和現金流足以彌補債務。

- 股息由收益和現金流支付。

- 韓元的股息信息

- 在過去的一年中,收益有所下降。

- 與消費零售市場前25%的股息支付者相比,股息很低。

- 預計未來三年的年收入將增長。

- 根據市盈率和估計的公允價值,物有所值。

- 預計年收益的增長速度將低於美國市場。

- 分析師對韓國還有什麼預測?

繼續前進:

就建立投資論點而言,估值只是硬幣的一面,它不應該是你研究公司時唯一考慮的指標。DCF模型不是完美的股票估值工具。相反,DCF模型的最佳用途是測試某些假設和理論,看看它們是否會導致公司被低估或高估。如果一家公司以不同的速度增長,或者其股本成本或無風險利率急劇變化,則產出可能會大不相同。爲什麼內在價值高於當前股價?對於克羅格,我們整理了你應該評估的三個基本因素:

- 風險:舉例來說,投資風險的幽靈無處不在。我們已經向克羅格確定了兩個警告信號,了解這些信號應該是您投資過程的一部分。

- 未來收益:與同行和整個市場相比,KR的增長率如何?通過與我們的免費分析師增長預期圖表互動,深入了解未來幾年的分析師共識數字。

- 其他穩健的業務:低債務、高股本回報率和良好的過去表現是強大業務的基礎。爲什麼不瀏覽我們具有堅實業務基礎的股票互動清單,看看是否還有其他你可能沒有考慮過的公司!

PS。Simply Wall St每天都會更新每隻美國股票的差價合約計算結果,因此,如果您想找到任何其他股票的內在價值,請在此處搜索。

對這篇文章有反饋嗎?對內容感到擔憂?直接聯繫我們。 或者,給編輯團隊 (at) simplywallst.com 發送電子郵件。

Simply Wall St的這篇文章本質上是籠統的。我們僅使用公正的方法根據歷史數據和分析師的預測提供評論,我們的文章無意作爲財務建議。它不構成買入或賣出任何股票的建議,也沒有考慮到您的目標或財務狀況。我們的目標是爲您提供由基本數據驅動的長期重點分析。請注意,我們的分析可能不考慮最新的價格敏感型公司公告或定性材料。簡而言之,華爾街沒有持有任何上述股票的頭寸。

譯文內容由第三人軟體翻譯。

風險及免責聲明

- 分享到weixin

- 分享到qq

- 分享到facebook

- 分享到twitter

- 分享到微博

- 粘贴板

使用瀏覽器的分享功能,分享給你的好友吧