Analysts Are More Bearish On Guanghui Energy Co., Ltd. (SHSE:600256) Than They Used To Be

Analysts Are More Bearish On Guanghui Energy Co., Ltd. (SHSE:600256) Than They Used To Be

The analysts covering Guanghui Energy Co., Ltd. (SHSE:600256) delivered a dose of negativity to shareholders today, by making a substantial revision to their statutory forecasts for this year. Revenue and earnings per share (EPS) forecasts were both revised downwards, with the analysts seeing grey clouds on the horizon.

報道光輝能源有限公司(SHSE: 600256)的分析師今天對今年的法定預測進行了重大修訂,從而向股東傳遞了一定負面情緒。收入和每股收益(EPS)的預測均向下修正,分析師認爲灰雲即將出現。

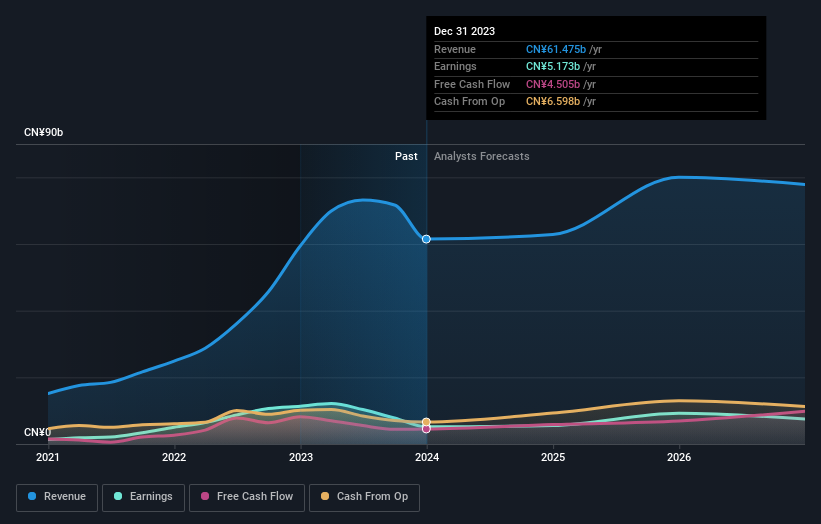

Following the downgrade, the current consensus from Guanghui Energy's five analysts is for revenues of CN¥63b in 2024 which - if met - would reflect a reasonable 2.3% increase on its sales over the past 12 months. Statutory earnings per share are presumed to increase 6.3% to CN¥0.85. Previously, the analysts had been modelling revenues of CN¥76b and earnings per share (EPS) of CN¥1.29 in 2024. It looks like analyst sentiment has declined substantially, with a substantial drop in revenue estimates and a large cut to earnings per share numbers as well.

評級下調之後,光輝能源的五位分析師目前的共識是,2024年的收入爲630億元人民幣,如果得到滿足,將反映其在過去12個月中銷售額的合理增長2.3%。預計每股法定收益將增長6.3%,至0.85元人民幣。此前,分析師一直在模擬2024年的收入爲760億元人民幣,每股收益(EPS)爲1.29元人民幣。看來分析師的情緒已大幅下降,收入預期大幅下降,每股收益也大幅下調。

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Guanghui Energy's past performance and to peers in the same industry. It's pretty clear that there is an expectation that Guanghui Energy's revenue growth will slow down substantially, with revenues to the end of 2024 expected to display 2.3% growth on an annualised basis. This is compared to a historical growth rate of 41% over the past five years. Compare this against other companies (with analyst forecasts) in the industry, which are in aggregate expected to see revenue growth of 3.9% annually. Factoring in the forecast slowdown in growth, it seems obvious that Guanghui Energy is also expected to grow slower than other industry participants.

這些估計很有趣,但是在查看預測與光輝能源過去的表現以及與同一行業的同行進行比較時,可以更粗略地描繪一些線索。很明顯,預計光輝能源的收入增長將大幅放緩,預計到2024年底的收入將按年計算增長2.3%。相比之下,過去五年的歷史增長率爲41%。相比之下,該行業的其他公司(根據分析師的預測),後者的總體收入預計每年將增長3.9%。考慮到增長放緩的預測,很明顯,光輝能源的增長速度預計也將低於其他行業參與者。

The Bottom Line

底線

The biggest issue in the new estimates is that analysts have reduced their earnings per share estimates, suggesting business headwinds lay ahead for Guanghui Energy. Regrettably, they also downgraded their revenue estimates, and the latest forecasts imply the business will grow sales slower than the wider market. Given the serious cut to this year's outlook, it's clear that analysts have turned more bearish on Guanghui Energy, and we wouldn't blame shareholders for feeling a little more cautious themselves.

新估計中最大的問題是,分析師下調了每股收益預期,這表明光輝能源面臨業務不利因素。遺憾的是,他們還下調了收入預期,最新的預測表明該業務的銷售增長將慢於整個市場。鑑於今年的前景大幅下調,很明顯,分析師對光輝能源的看跌情緒更加看跌,我們不會責怪股東自己感到更加謹慎。

Worse, Guanghui Energy is labouring under a substantial debt burden, which - if today's forecasts prove accurate - the forecast downgrade could potentially exacerbate. You can learn more about our debt analysis for free on our platform here.

更糟糕的是,光輝能源揹負着沉重的債務負擔,如果今天的預測證明準確的話,下調預測可能會加劇這種負擔。您可以進一步了解我們的債務分析 免費 在我們的平台上

You can also see our analysis of Guanghui Energy's Board and CEO remuneration and experience, and whether company insiders have been buying stock.

您還可以看到我們對光輝能源董事會和首席執行官薪酬和經驗的分析,以及公司內部人士是否一直在購買股票。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對這篇文章有反饋嗎?對內容感到擔憂?直接聯繫我們。 或者,給編輯團隊 (at) simplywallst.com 發送電子郵件。

Simply Wall St的這篇文章本質上是籠統的。我們僅使用公正的方法根據歷史數據和分析師的預測提供評論,我們的文章無意作爲財務建議。它不構成買入或賣出任何股票的建議,也沒有考慮到您的目標或財務狀況。我們的目標是爲您提供由基本數據驅動的長期重點分析。請注意,我們的分析可能不考慮最新的價格敏感型公司公告或定性材料。簡而言之,華爾街沒有持有任何上述股票的頭寸。

譯文內容由第三人軟體翻譯。