Jiangsu Phoenix Publishing & Media Corporation Limited Just Beat Earnings Expectations: Here's What Analysts Think Will Happen Next

Jiangsu Phoenix Publishing & Media Corporation Limited Just Beat Earnings Expectations: Here's What Analysts Think Will Happen Next

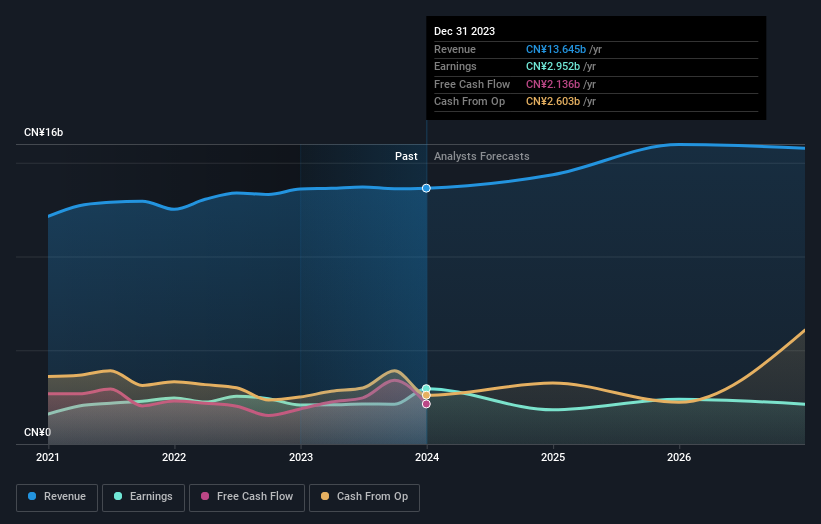

Last week, you might have seen that Jiangsu Phoenix Publishing & Media Corporation Limited (SHSE:601928) released its annual result to the market. The early response was not positive, with shares down 9.9% to CN¥10.14 in the past week. It looks to have been a decent result overall - while revenue fell marginally short of analyst estimates at CN¥14b, statutory earnings beat expectations by a notable 21%, coming in at CN¥1.16 per share. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. With this in mind, we've gathered the latest statutory forecasts to see what the analysts are expecting for next year.

上週,你可能已經看到江蘇鳳凰出版傳媒股份有限公司(SHSE: 601928)向市場發佈了年度業績。早期的反應並不樂觀,過去一週股價下跌9.9%,至10.14元人民幣。總體而言,這似乎是一個不錯的業績——雖然收入略低於分析師預期的140億元人民幣,但法定收益明顯超出預期21%,爲每股1.16元人民幣。分析師通常會在每份收益報告中更新他們的預測,我們可以從他們的估計中判斷他們對公司的看法是否發生了變化,或者是否有任何新的問題需要注意。考慮到這一點,我們收集了最新的法定預測,以了解分析師對明年的預期。

Taking into account the latest results, the most recent consensus for Jiangsu Phoenix Publishing & Media from four analysts is for revenues of CN¥14.4b in 2024. If met, it would imply an okay 5.2% increase on its revenue over the past 12 months. Statutory earnings per share are expected to dive 38% to CN¥0.71 in the same period. Yet prior to the latest earnings, the analysts had been anticipated revenues of CN¥15.6b and earnings per share (EPS) of CN¥0.78 in 2024. It's pretty clear that pessimism has reared its head after the latest results, leading to a weaker revenue outlook and a minor downgrade to earnings per share estimates.

考慮到最新業績,四位分析師對江蘇鳳凰出版傳媒的最新共識是,2024年的收入爲144億元人民幣。如果得到滿足,這意味着其收入在過去12個月中增長了5.2%。同期,法定每股收益預計將下降38%,至0.71元人民幣。然而,在最新業績公佈之前,分析師曾預計2024年的收入爲156億元人民幣,每股收益(EPS)爲0.78元人民幣。很明顯,在最新業績公佈後,悲觀情緒已經抬頭,導致收入前景疲軟,每股收益預期略有下調。

The consensus price target fell 5.3% to CN¥12.30, with the weaker earnings outlook clearly leading valuation estimates. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. Currently, the most bullish analyst values Jiangsu Phoenix Publishing & Media at CN¥13.00 per share, while the most bearish prices it at CN¥11.90. Still, with such a tight range of estimates, it suggeststhe analysts have a pretty good idea of what they think the company is worth.

共識目標股價下跌5.3%,至12.30元人民幣,盈利前景疲軟顯然領先於估值預期。但是,固定單一價格目標可能是不明智的,因爲共識目標實際上是分析師目標股價的平均值。因此,一些投資者喜歡查看估計範圍,看看對公司的估值是否有任何分歧。目前,最看漲的分析師估值江蘇鳳凰出版傳媒爲每股13.00元人民幣,而最看跌的分析師估值爲11.90元人民幣。儘管如此,由於估計範圍如此之窄,這表明分析師對他們認爲該公司的價值有了很好的了解。

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Jiangsu Phoenix Publishing & Media's past performance and to peers in the same industry. It's clear from the latest estimates that Jiangsu Phoenix Publishing & Media's rate of growth is expected to accelerate meaningfully, with the forecast 5.2% annualised revenue growth to the end of 2024 noticeably faster than its historical growth of 3.1% p.a. over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 13% per year. It seems obvious that, while the future growth outlook is brighter than the recent past, Jiangsu Phoenix Publishing & Media is expected to grow slower than the wider industry.

這些估計很有趣,但是在查看預測與江蘇鳳凰出版傳媒過去的表現以及與同一行業的同行進行比較時,可以更粗略地描述一些細節。從最新估計中可以明顯看出,江蘇鳳凰出版傳媒的增長率預計將大幅加快,預計到2024年底的年化收入增長率爲5.2%,明顯快於過去五年3.1%的歷史增長。相比之下,我們的數據表明,預計類似行業的其他公司(有分析師報道)的收入將以每年13%的速度增長。顯而易見,儘管未來的增長前景比最近更加光明,但預計江蘇鳳凰出版傳媒的增長將慢於整個行業。

The Bottom Line

底線

The most important thing to take away is that the analysts downgraded their earnings per share estimates, showing that there has been a clear decline in sentiment following these results. On the negative side, they also downgraded their revenue estimates, and forecasts imply they will perform worse than the wider industry. The consensus price target fell measurably, with the analysts seemingly not reassured by the latest results, leading to a lower estimate of Jiangsu Phoenix Publishing & Media's future valuation.

要了解的最重要的一點是,分析師下調了每股收益的預期,這表明公佈這些業績後,市場情緒明顯下降。不利的一面是,他們還下調了收入預期,預測表明他們的表現將比整個行業差。共識目標股價大幅下降,最新業績似乎並未讓分析師放心,這導致對江蘇鳳凰出版傳媒未來估值的估計降低。

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have estimates - from multiple Jiangsu Phoenix Publishing & Media analysts - going out to 2026, and you can see them free on our platform here.

話雖如此,公司收益的長期軌跡比明年重要得多。根據多位江蘇鳳凰出版傳媒分析師的估計,到2026年,你可以在我們的平台上免費查看。

Before you take the next step you should know about the 2 warning signs for Jiangsu Phoenix Publishing & Media (1 shouldn't be ignored!) that we have uncovered.

在你採取下一步行動之前,你應該了解江蘇鳳凰出版傳媒的兩個警告標誌(其中一個不容忽視!)這是我們發現的。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對這篇文章有反饋嗎?對內容感到擔憂?直接聯繫我們。 或者,給編輯團隊 (at) simplywallst.com 發送電子郵件。

Simply Wall St的這篇文章本質上是籠統的。我們僅使用公正的方法根據歷史數據和分析師的預測提供評論,我們的文章無意作爲財務建議。它不構成買入或賣出任何股票的建議,也沒有考慮到您的目標或財務狀況。我們的目標是爲您提供由基本數據驅動的長期重點分析。請注意,我們的分析可能不考慮最新的價格敏感型公司公告或定性材料。簡而言之,華爾街沒有持有任何上述股票的頭寸。

譯文內容由第三人軟體翻譯。