Source: Barron Weekly Author: Nicolas Jasinski

The loose financial situation will make it unlikely that the data will have the kind of performance expected by the Federal Reserve.

Whether it's a job seeker entering the final round of interviews, a baseball player heading to the batting zone, or a US Federal Reserve official looking for signs that inflation continues to fall towards the 2% target, they all want more confidence in themselves.

Unfortunately, people have lacked confidence that inflation will cool down this year. Prices have continued to rise longer than expected, and the US economy continues to grow rapidly. As Powell and many other Federal Reserve officials recently pointed out, there is no sufficient reason for the Federal Reserve to cut interest rates in the short term.

The futures market has lowered expectations for how many times the Fed will cut interest rates this year, and some economists even think that the Fed will not cut interest rates this year.

What is the reason behind inflationary resilience? Although Powell and other Federal Reserve officials insist that current monetary policy is restrictive, America's loose financial environment is a major reason.

Looking at the numbers, Powell and other Federal Reserve officials are probably right. According to the “Taylor Rule” (Taylor Rule) proposed by Stanford University economist John Taylor (John Taylor) in a 1993 paper, the federal funds rate calculated from recent inflation and economic growth data is around 4.75%, lower than the current 5.25%-5.5%, marking the first time in ten years that policy interest rates measured according to “Taylor's Law” are in a restricted area (with the exception of 2020, when the US economy stagnated due to the pandemic, and even the 0% federal funds rate was limited).

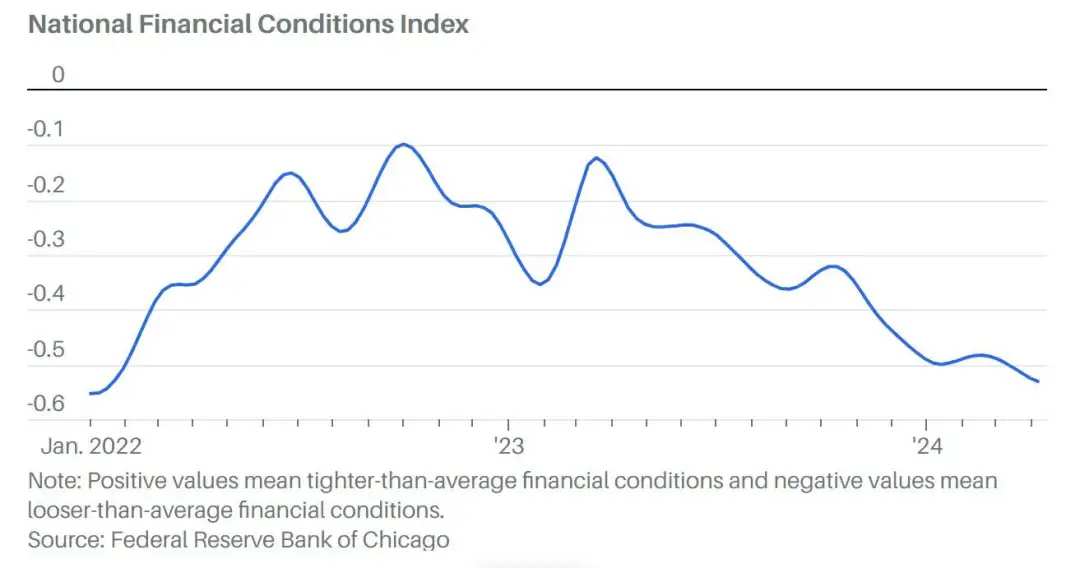

But that's just theoretical. Currently, indicators that measure financial conditions in the real world show that monetary policy is in a fairly relaxed region. The National Financial Conditions Index (National Financial Conditions Index) compiled by the Chicago Federal Reserve is as relaxed as January 2022, two months before the Federal Reserve began raising interest rates.

The National Financial Condition Index is updated weekly. The index includes 105 sub-indicators, including bank loan standards, differences in yield on treasury bonds, corporate bonds, and mortgaged bonds, the level of outstanding debt and newly issued debt, the US dollar index, and the level of the stock market.

However, the Federal Reserve directly controls only one factor — interest rates. Before the Federal Reserve began raising interest rates in 2022, a large number of companies were refinancing to convert short-term debt into long-term debt. Millions of landlords currently enjoy 30-year fixed mortgage rates lower than what they earn on savings accounts. The steady growth in corporate profits and the investment boom fueled by artificial intelligence drove stock indexes to record highs. Housing prices remain high due to structural supply shortages in the US housing market.

With financial conditions in other areas being relaxed, the fact that the federal funds rate is much higher than 5% does not explain the whole story.

The strategist at Jefferies (Jefferies) said, “We believe that such loose financial conditions will make the data unlikely to have the kind of performance expected by the Federal Reserve, that is, a slowdown in the labor market and a decline in inflation.”

Private markets, such as venture capital, are an area where financial conditions are less relaxed. According to Terminal.ai data, venture capital in 2023 fell to its low during the 2020 pandemic, or even lower, and has been fluctuating horizontally since then. Arjun Sethi (Arjun Sethi), co-founder of Terminal.ai, said, “Capital flows are stabilizing, but today companies that receive financing tend to have more stable businesses and have clear profit paths.”

This may be a healthy shift compared to 2021 and 2022, when investors often “check before asking questions.”

The Chicago Federal Reserve's National Financial Condition Index is as relaxed as before the Federal Reserve began raising interest rates in 2022. A positive index indicates that the financial situation is tighter than the average, and a negative index indicates that the financial situation is looser than the average.

The loose financial situation is supporting other sectors: According to Bloomberg (Bloomberg), corporate bond issuance reached a record high in the first quarter. Torsten Sløk (Torsten Sløk), chief economist at Apollo Global Management (Apollo Global Management), said, “Easy financial conditions continue to provide an important driving force for economic growth and inflation. Therefore, the Federal Reserve's fight against inflation is not over, and interest rates will remain high for a longer period of time.”

Slock expects that the Federal Reserve will not cut interest rates this year. In a month or two, after strong inflation and economic growth data are released, the market's view may also change to not cutting interest rates this year, which means that bond yields will rise, which in turn will lead to a tightening of financial conditions.

David Page (David Page), head of macroeconomic research at AXA Investment Management (AXA Investment Management), pointed out that there is another technical reason why financial conditions will tighten later this year. The Federal Reserve's use of overnight reverse repurchase agreements (RRPs) has been declining over the past year. The Federal Reserve currently allows 60 billion US dollars of treasury bonds and 35 billion US dollars of mortgage-backed securities to mature naturally every month, and does not reinvest them. Last week, the balance of overnight reverse repurchase agreements fell below $400 billion from $2.4 trillion a year ago, with an average monthly decrease of about $167 billion. At the current rate, the balance of the overnight reverse repurchase agreement will be exhausted around the end of June.

At that point, quantitative austerity will begin to come directly from bank reserves, thereby draining liquidity from the system. Page pointed out that this is the complete opposite of last year's situation, and it will be a negative factor for all types of risk assets.

However, Federal Reserve officials know that this day is coming and have begun discussions on slowing down the pace of quantitative austerity. The relevant plans may be announced as early as May 1 at the policy meeting ending on May 1. However, Wilshire's chief investment officer Josh Emanuel (Josh Emanuel) believes that in the current environment, “the Federal Reserve does not need to cut interest rates for liquidity reasons.”

edit/lambor