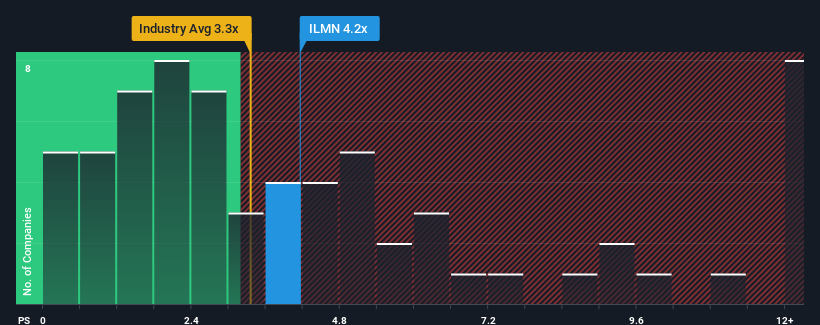

Illumina, Inc.'s (NASDAQ:ILMN) price-to-sales (or "P/S") ratio of 4.2x may not look like an appealing investment opportunity when you consider close to half the companies in the Life Sciences industry in the United States have P/S ratios below 3.3x. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/S.

NasdaqGS:ILMN Price to Sales Ratio vs Industry April 22nd 2024

What Does Illumina's Recent Performance Look Like?

Illumina's negative revenue growth of late has neither been better nor worse than most other companies. One possibility is that the P/S ratio is high because investors think the company can turn things around and break free from the broader downward trend in revenue. If not, then existing shareholders may be a little nervous about the viability of the share price.

Keen to find out how analysts think Illumina's future stacks up against the industry? In that case, our free report is a great place to start.

How Is Illumina's Revenue Growth Trending?

In order to justify its P/S ratio, Illumina would need to produce impressive growth in excess of the industry.

Retrospectively, the last year delivered a frustrating 1.8% decrease to the company's top line. Still, the latest three year period has seen an excellent 39% overall rise in revenue, in spite of its unsatisfying short-term performance. Accordingly, while they would have preferred to keep the run going, shareholders would definitely welcome the medium-term rates of revenue growth.

Shifting to the future, estimates from the analysts covering the company suggest revenue should grow by 6.3% per annum over the next three years. Meanwhile, the rest of the industry is forecast to expand by 6.4% per year, which is not materially different.

In light of this, it's curious that Illumina's P/S sits above the majority of other companies. Apparently many investors in the company are more bullish than analysts indicate and aren't willing to let go of their stock right now. These shareholders may be setting themselves up for disappointment if the P/S falls to levels more in line with the growth outlook.

What Does Illumina's P/S Mean For Investors?

We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Analysts are forecasting Illumina's revenues to only grow on par with the rest of the industry, which has lead to the high P/S ratio being unexpected. Right now we are uncomfortable with the relatively high share price as the predicted future revenues aren't likely to support such positive sentiment for long. This places shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

Many other vital risk factors can be found on the company's balance sheet. Our free balance sheet analysis for Illumina with six simple checks will allow you to discover any risks that could be an issue.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Illumina, Inc. '考慮到美國生命科學行業將近一半的公司的市盈率低於3.3倍,s(納斯達克股票代碼:ILMN)4.2倍的市銷率(或 “市盈率”)可能不是一個有吸引力的投資機會。但是,我們需要更深入地挖掘,以確定市銷率上升是否有合理的基礎。

Retrospectively, the last year delivered a frustrating 1.8% decrease to the company's top line. Still, the latest three year period has seen an excellent 39% overall rise in revenue, in spite of its unsatisfying short-term performance. Accordingly, while they would have preferred to keep the run going, shareholders would definitely welcome the medium-term rates of revenue growth.

Retrospectively, the last year delivered a frustrating 1.8% decrease to the company's top line. Still, the latest three year period has seen an excellent 39% overall rise in revenue, in spite of its unsatisfying short-term performance. Accordingly, while they would have preferred to keep the run going, shareholders would definitely welcome the medium-term rates of revenue growth.

回顧過去,去年該公司的收入下降了令人沮喪的1.8%。儘管如此,儘管短期表現不令人滿意,但最近三年的總體收入仍增長了39%。因此,儘管股東們本來希望繼續經營,但他們肯定會歡迎中期收入增長率。

回顧過去,去年該公司的收入下降了令人沮喪的1.8%。儘管如此,儘管短期表現不令人滿意,但最近三年的總體收入仍增長了39%。因此,儘管股東們本來希望繼續經營,但他們肯定會歡迎中期收入增長率。