V.F. Corporation's (NYSE:VFC) Shareholders Might Be Looking For Exit

V.F. Corporation's (NYSE:VFC) Shareholders Might Be Looking For Exit

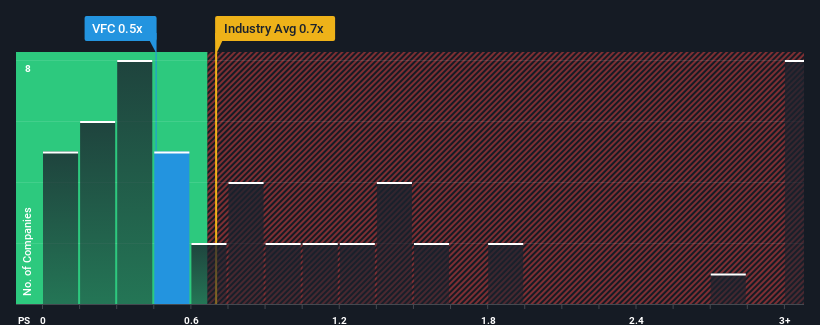

It's not a stretch to say that V.F. Corporation's (NYSE:VFC) price-to-sales (or "P/S") ratio of 0.5x right now seems quite "middle-of-the-road" for companies in the Luxury industry in the United States, where the median P/S ratio is around 0.7x. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

What Does V.F's P/S Mean For Shareholders?

While the industry has experienced revenue growth lately, V.F's revenue has gone into reverse gear, which is not great. It might be that many expect the dour revenue performance to strengthen positively, which has kept the P/S from falling. You'd really hope so, otherwise you're paying a relatively elevated price for a company with this sort of growth profile.

Want the full picture on analyst estimates for the company? Then our free report on V.F will help you uncover what's on the horizon.What Are Revenue Growth Metrics Telling Us About The P/S?

V.F's P/S ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the industry.

Retrospectively, the last year delivered a frustrating 7.5% decrease to the company's top line. Regardless, revenue has managed to lift by a handy 24% in aggregate from three years ago, thanks to the earlier period of growth. Accordingly, while they would have preferred to keep the run going, shareholders would be roughly satisfied with the medium-term rates of revenue growth.

Turning to the outlook, the next three years should generate growth of 2.5% per annum as estimated by the analysts watching the company. That's shaping up to be materially lower than the 6.7% per year growth forecast for the broader industry.

In light of this, it's curious that V.F's P/S sits in line with the majority of other companies. It seems most investors are ignoring the fairly limited growth expectations and are willing to pay up for exposure to the stock. Maintaining these prices will be difficult to achieve as this level of revenue growth is likely to weigh down the shares eventually.

What We Can Learn From V.F's P/S?

Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

When you consider that V.F's revenue growth estimates are fairly muted compared to the broader industry, it's easy to see why we consider it unexpected to be trading at its current P/S ratio. When we see companies with a relatively weaker revenue outlook compared to the industry, we suspect the share price is at risk of declining, sending the moderate P/S lower. Circumstances like this present a risk to current and prospective investors who may see share prices fall if the low revenue growth impacts the sentiment.

It is also worth noting that we have found 2 warning signs for V.F that you need to take into consideration.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

可以毫不誇張地說,對於美國奢侈品行業的公司來說,VF Corporation(紐約證券交易所代碼:VFC)0.5倍的市銷率(或 “市盈率”)目前似乎相當 “處於中間位置”,那裏的市銷率中位數約爲0.7倍。儘管這可能不會引起任何關注,但如果市銷率不合理,投資者可能會錯過潛在的機會或無視迫在眉睫的失望情緒。

VF的市銷率對股東意味着什麼?

儘管該行業最近經歷了收入增長,但V.F的收入卻倒退了,這並不好。許多人可能預計,糟糕的收入表現將積極增強,這使市銷售率沒有下降。你真的希望如此,否則你會爲一傢俱有這種增長概況的公司付出相對較高的代價。

想全面了解分析師對公司的估計嗎?然後,我們的免費VF報告將幫助您發現即將發生的事情。收入增長指標告訴我們有關市銷率的哪些信息?

對於一家預計只會實現適度增長且重要的是表現與行業持平的公司來說,VF的市銷率是典型的。

回顧過去,去年的公司收入下降了7.5%,令人沮喪。無論如何,得益於較早的增長,收入總共比三年前增長了24%。因此,儘管股東本來希望繼續經營,但他們會對中期收入增長率大致滿意。

談到前景,根據關注該公司的分析師的估計,未來三年將實現每年2.5%的增長。這將大大低於整個行業每年6.7%的增長預期。

有鑑於此,奇怪的是,V.F的市銷率與其他大部分公司持平。看來大多數投資者無視相當有限的增長預期,願意爲股票敞口付出代價。維持這些價格將很難實現,因爲這種收入增長水平最終可能會壓低股價。

我們可以從V.F的市銷率中學到什麼?

通常,我們傾向於限制使用市銷率來確定市場對公司整體健康狀況的看法。

當你考慮到與整個行業相比,V.F的收入增長預期相當低時,不難理解我們爲何認爲以目前的市銷率進行交易是出乎意料的。當我們看到與該行業相比收入前景相對疲軟的公司時,我們懷疑股價有下跌的風險,從而使溫和的市銷售率走低。像這樣的情況給當前和潛在的投資者帶來了風險,如果低收入增長影響市場情緒,他們可能會看到股價下跌。

還值得注意的是,我們發現了 2 個 V.F 警告信號,你需要考慮。

當然,具有良好收益增長曆史的盈利公司通常是更安全的選擇。因此,您可能希望看到這些免費收集的市盈率合理且收益增長強勁的其他公司。

對這篇文章有反饋嗎?對內容感到擔憂?直接聯繫我們。 或者,給編輯團隊 (at) simplywallst.com 發送電子郵件。

Simply Wall St的這篇文章本質上是籠統的。我們僅使用公正的方法根據歷史數據和分析師的預測提供評論,我們的文章無意作爲財務建議。它不構成買入或賣出任何股票的建議,也沒有考慮到您的目標或財務狀況。我們的目標是爲您提供由基本數據驅動的長期重點分析。請注意,我們的分析可能不考慮最新的價格敏感型公司公告或定性材料。簡而言之,華爾街沒有持有任何上述股票的頭寸。

譯文內容由第三人軟體翻譯。

風險及免責聲明

- 分享到weixin

- 分享到qq

- 分享到facebook

- 分享到twitter

- 分享到微博

- 粘贴板

使用瀏覽器的分享功能,分享給你的好友吧