Revenues Tell The Story For Asana, Inc. (NYSE:ASAN)

Revenues Tell The Story For Asana, Inc. (NYSE:ASAN)

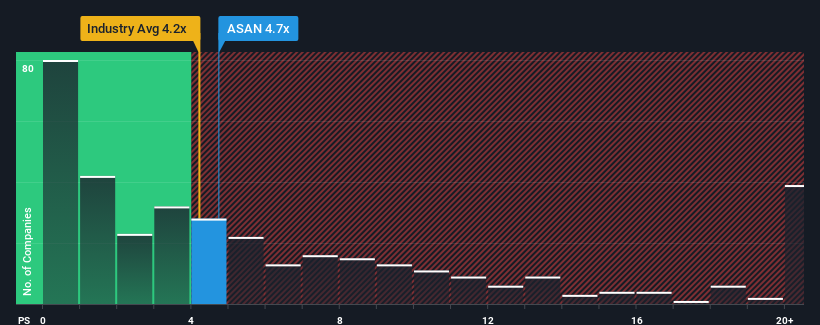

With a median price-to-sales (or "P/S") ratio of close to 4.2x in the Software industry in the United States, you could be forgiven for feeling indifferent about Asana, Inc.'s (NYSE:ASAN) P/S ratio of 4.7x. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

How Asana Has Been Performing

With revenue growth that's superior to most other companies of late, Asana has been doing relatively well. It might be that many expect the strong revenue performance to wane, which has kept the P/S ratio from rising. If not, then existing shareholders have reason to be feeling optimistic about the future direction of the share price.

Keen to find out how analysts think Asana's future stacks up against the industry? In that case, our free report is a great place to start.What Are Revenue Growth Metrics Telling Us About The P/S?

The only time you'd be comfortable seeing a P/S like Asana's is when the company's growth is tracking the industry closely.

Retrospectively, the last year delivered an exceptional 19% gain to the company's top line. The strong recent performance means it was also able to grow revenue by 187% in total over the last three years. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Shifting to the future, estimates from the analysts covering the company suggest revenue should grow by 16% per annum over the next three years. Meanwhile, the rest of the industry is forecast to expand by 15% each year, which is not materially different.

With this information, we can see why Asana is trading at a fairly similar P/S to the industry. It seems most investors are expecting to see average future growth and are only willing to pay a moderate amount for the stock.

The Final Word

Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've seen that Asana maintains an adequate P/S seeing as its revenue growth figures match the rest of the industry. At this stage investors feel the potential for an improvement or deterioration in revenue isn't great enough to push P/S in a higher or lower direction. All things considered, if the P/S and revenue estimates contain no major shocks, then it's hard to see the share price moving strongly in either direction in the near future.

Don't forget that there may be other risks. For instance, we've identified 3 warning signs for Asana that you should be aware of.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

由於美國軟件行業的中位數市銷率(或 “市銷率”)接近4.2倍,你對Asana, Inc.感到漠不關心是可以原諒的。”s(紐約證券交易所代碼:ASAN)市銷率爲4.7倍。但是,不加解釋地忽略市銷率是不明智的,因爲投資者可能會忽視一個明顯的機會或一個代價高昂的錯誤。

Asana 的表現如何

Asana最近的收入增長優於大多數其他公司,因此表現相對較好。許多人可能預計強勁的收入表現將減弱,這阻礙了市銷率的上升。如果不是,那麼現有股東就有理由對股價的未來走向感到樂觀。

想了解分析師如何看待Asana的未來與該行業的對立嗎?在這種情況下,我們的免費報告是一個很好的起點。收入增長指標告訴我們有關市銷率的哪些信息?

你唯一能放心地看到像Asana這樣的市銷率的時候是公司的增長密切關注行業的時候。

回顧過去,去年的公司收入實現了19%的驚人增長。最近的強勁表現意味着它在過去三年中總收入增長了187%。因此,股東們肯定會對這些中期收入增長率表示歡迎。

展望未來,報道該公司的分析師的估計表明,未來三年收入將每年增長16%。同時,預計該行業的其他部門每年將增長15%,這沒有實質性區別。

有了這些信息,我們可以明白爲何Asana的市銷率與該行業相當相似。看來大多數投資者都期望未來的平均增長,只願意爲股票支付適度的費用。

最後一句話

通常,在做出投資決策時,我們會謹慎行事,不要過多地閱讀市售比率,儘管這可以充分揭示其他市場參與者對公司的看法。

我們已經看到,Asana保持了足夠的市銷率,因爲其收入增長數據與該行業的其他部門相匹配。在現階段,投資者認爲,收入改善或惡化的可能性不足以將市銷率推向更高或更低的方向。綜合考慮,如果市銷率和收入估計不包含重大沖擊,那麼很難看到股價在不久的將來雙向強勁走勢。

別忘了可能還有其他風險。例如,我們已經確定了你應該注意的3種Asana警告信號。

重要的是要確保你尋找一家優秀的公司,而不僅僅是你遇到的第一個想法。因此,如果盈利能力的增長與你對一家優秀公司的想法一致,那就來看看這份免費名單吧,列出了最近收益增長強勁(市盈率低)的有趣公司。

對這篇文章有反饋嗎?對內容感到擔憂?直接聯繫我們。 或者,給編輯團隊 (at) simplywallst.com 發送電子郵件。

Simply Wall St的這篇文章本質上是籠統的。我們僅使用公正的方法根據歷史數據和分析師的預測提供評論,我們的文章無意作爲財務建議。它不構成買入或賣出任何股票的建議,也沒有考慮到您的目標或財務狀況。我們的目標是爲您提供由基本數據驅動的長期重點分析。請注意,我們的分析可能不考慮最新的價格敏感型公司公告或定性材料。簡而言之,華爾街沒有持有任何上述股票的頭寸。

譯文內容由第三人軟體翻譯。

風險及免責聲明

- 分享到weixin

- 分享到qq

- 分享到facebook

- 分享到twitter

- 分享到微博

- 粘贴板

使用瀏覽器的分享功能,分享給你的好友吧