Why Investors Shouldn't Be Surprised By Seatrium Limited's (SGX:S51) P/S

Why Investors Shouldn't Be Surprised By Seatrium Limited's (SGX:S51) P/S

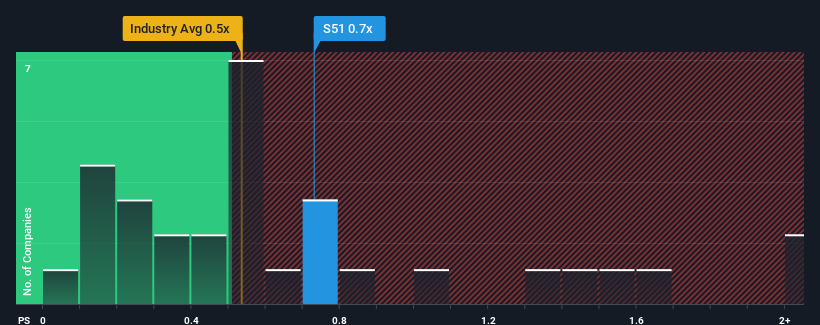

There wouldn't be many who think Seatrium Limited's (SGX:S51) price-to-sales (or "P/S") ratio of 0.7x is worth a mention when the median P/S for the Machinery industry in Singapore is similar at about 0.5x. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

How Seatrium Has Been Performing

With revenue growth that's superior to most other companies of late, Seatrium has been doing relatively well. Perhaps the market is expecting this level of performance to taper off, keeping the P/S from soaring. If the company manages to stay the course, then investors should be rewarded with a share price that matches its revenue figures.

Want the full picture on analyst estimates for the company? Then our free report on Seatrium will help you uncover what's on the horizon.Do Revenue Forecasts Match The P/S Ratio?

There's an inherent assumption that a company should be matching the industry for P/S ratios like Seatrium's to be considered reasonable.

Retrospectively, the last year delivered an explosive gain to the company's top line. The latest three year period has also seen an incredible overall rise in revenue, aided by its incredible short-term performance. So we can start by confirming that the company has done a tremendous job of growing revenue over that time.

Looking ahead now, revenue is anticipated to climb by 7.8% per year during the coming three years according to the nine analysts following the company. That's shaping up to be similar to the 9.0% each year growth forecast for the broader industry.

With this in mind, it makes sense that Seatrium's P/S is closely matching its industry peers. Apparently shareholders are comfortable to simply hold on while the company is keeping a low profile.

The Key Takeaway

It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've seen that Seatrium maintains an adequate P/S seeing as its revenue growth figures match the rest of the industry. At this stage investors feel the potential for an improvement or deterioration in revenue isn't great enough to push P/S in a higher or lower direction. Unless these conditions change, they will continue to support the share price at these levels.

The company's balance sheet is another key area for risk analysis. You can assess many of the main risks through our free balance sheet analysis for Seatrium with six simple checks.

If these risks are making you reconsider your opinion on Seatrium, explore our interactive list of high quality stocks to get an idea of what else is out there.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

當新加坡機械行業的市盈率中位數相似約爲0.5倍時,不會有多少人認爲Seatrium Limited(新加坡證券交易所股票代碼:S51)的0.7倍市銷率(或 “市盈率”)值得一提。但是,不加解釋地忽略市銷率是不明智的,因爲投資者可能會忽視一個明顯的機會或一個代價高昂的錯誤。

Seatrium 的表現如何

由於最近的收入增長優於大多數其他公司,Seatrium的表現相對較好。也許市場預計這種表現水平將逐漸減弱,從而防止市銷率飆升。如果公司設法堅持下去,那麼投資者應該獲得與其收入數字相匹配的股價作爲獎勵。

想全面了解分析師對公司的估計嗎?然後,我們關於Seatrium的免費報告將幫助您發現即將發生的事情。收入預測與市銷率相匹配嗎?

人們固有的假設是,公司應該與行業相匹配,以使像Seatrium這樣的市銷率被認爲是合理的。

回顧過去,去年爲公司的收入帶來了爆炸式增長。在最近的三年中,收入也出現了令人難以置信的總體增長,這得益於其令人難以置信的短期表現。因此,我們可以先確認該公司在那段時間內在增加收入方面做得非常出色。

根據關注該公司的九位分析師的說法,展望未來,預計未來三年收入每年將增長7.8%。這將與整個行業每年9.0%的增長預測相似。

考慮到這一點,Seatrium的市銷率與業內同行緊密匹配是有道理的。顯然,在公司保持低調的同時,股東們很樂意堅持下去。

關鍵要點

有人認爲,在某些行業中,市銷率是衡量價值的較差指標,但它可以是一個有力的商業信心指標。

我們已經看到,Seatrium保持了足夠的市銷率,因爲其收入增長數據與行業其他部門相當。在現階段,投資者認爲,收入改善或惡化的可能性不足以將市銷率推向更高或更低的方向。除非這些條件發生變化,否則它們將繼續在這些水平上支撐股價。

該公司的資產負債表是風險分析的另一個關鍵領域。您可以通過我們對Seatrium的免費資產負債表分析,通過六張簡單的檢查來評估許多主要風險。

如果這些風險讓你重新考慮你對Seatrium的看法,請瀏覽我們的高質量股票互動清單,了解還有什麼。

對這篇文章有反饋嗎?對內容感到擔憂?直接聯繫我們。 或者,給編輯團隊 (at) simplywallst.com 發送電子郵件。

Simply Wall St的這篇文章本質上是籠統的。我們僅使用公正的方法根據歷史數據和分析師的預測提供評論,我們的文章無意作爲財務建議。它不構成買入或賣出任何股票的建議,也沒有考慮到您的目標或財務狀況。我們的目標是爲您提供由基本數據驅動的長期重點分析。請注意,我們的分析可能不考慮最新的價格敏感型公司公告或定性材料。簡而言之,華爾街沒有持有任何上述股票的頭寸。

譯文內容由第三人軟體翻譯。

風險及免責聲明

- 分享到weixin

- 分享到qq

- 分享到facebook

- 分享到twitter

- 分享到微博

- 粘贴板

使用瀏覽器的分享功能,分享給你的好友吧