QingCloud Technologies Corp.'s (SHSE:688316) 30% Share Price Plunge Could Signal Some Risk

QingCloud Technologies Corp.'s (SHSE:688316) 30% Share Price Plunge Could Signal Some Risk

Unfortunately for some shareholders, the QingCloud Technologies Corp. (SHSE:688316) share price has dived 30% in the last thirty days, prolonging recent pain. For any long-term shareholders, the last month ends a year to forget by locking in a 52% share price decline.

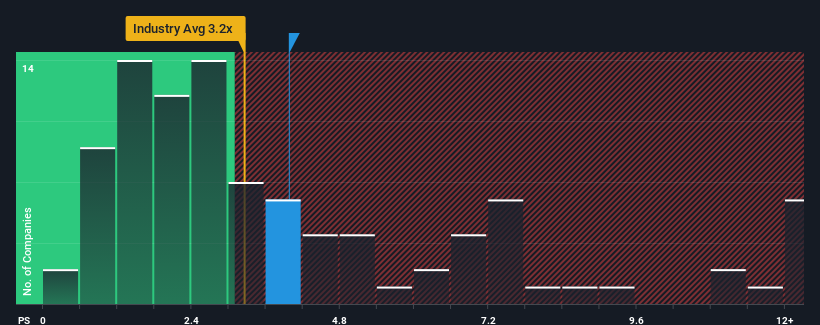

Even after such a large drop in price, given close to half the companies operating in China's IT industry have price-to-sales ratios (or "P/S") below 3.2x, you may still consider QingCloud Technologies as a stock to potentially avoid with its 4x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's as high as it is.

What Does QingCloud Technologies' P/S Mean For Shareholders?

The revenue growth achieved at QingCloud Technologies over the last year would be more than acceptable for most companies. One possibility is that the P/S ratio is high because investors think this respectable revenue growth will be enough to outperform the broader industry in the near future. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Although there are no analyst estimates available for QingCloud Technologies, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.Is There Enough Revenue Growth Forecasted For QingCloud Technologies?

In order to justify its P/S ratio, QingCloud Technologies would need to produce impressive growth in excess of the industry.

If we review the last year of revenue growth, the company posted a worthy increase of 9.9%. Ultimately though, it couldn't turn around the poor performance of the prior period, with revenue shrinking 22% in total over the last three years. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenue over that time.

In contrast to the company, the rest of the industry is expected to grow by 40% over the next year, which really puts the company's recent medium-term revenue decline into perspective.

In light of this, it's alarming that QingCloud Technologies' P/S sits above the majority of other companies. It seems most investors are ignoring the recent poor growth rate and are hoping for a turnaround in the company's business prospects. Only the boldest would assume these prices are sustainable as a continuation of recent revenue trends is likely to weigh heavily on the share price eventually.

What Does QingCloud Technologies' P/S Mean For Investors?

There's still some elevation in QingCloud Technologies' P/S, even if the same can't be said for its share price recently. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

We've established that QingCloud Technologies currently trades on a much higher than expected P/S since its recent revenues have been in decline over the medium-term. Right now we aren't comfortable with the high P/S as this revenue performance is highly unlikely to support such positive sentiment for long. Should recent medium-term revenue trends persist, it would pose a significant risk to existing shareholders' investments and prospective investors will have a hard time accepting the current value of the stock.

You should always think about risks. Case in point, we've spotted 2 warning signs for QingCloud Technologies you should be aware of, and 1 of them is a bit unpleasant.

If these risks are making you reconsider your opinion on QingCloud Technologies, explore our interactive list of high quality stocks to get an idea of what else is out there.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對於一些股東來說,不幸的是,青雲科技公司(上海證券交易所代碼:688316)的股價在過去三十天中下跌了30%,延續了最近的痛苦。對於任何長期股東來說,最後一個月的股價下跌幅度爲52%,從而結束了令人難忘的一年。

即使在價格大幅下跌之後,鑑於在中國IT行業運營的近一半公司的市銷率(或 “市銷率”)低於3.2倍,您仍然可以將QingCloud Technologies視爲可以避免的股票,因爲其市銷率爲4倍。但是,僅按面值計算市銷率是不明智的,因爲可以解釋其爲何如此之高。

青雲科技的市銷率對股東意味着什麼?

對於大多數公司來說,QingCloud Technologies去年實現的收入增長是完全可以接受的。一種可能性是市銷率很高,因爲投資者認爲這種可觀的收入增長足以在不久的將來跑贏整個行業。你真的希望如此,否則你會無緣無故地付出相當大的代價。

儘管沒有分析師對QingCloud Technologies的估計,但看看這個免費的數據豐富的可視化工具,看看該公司在收益、收入和現金流方面的積累情況。預計青雲科技的收入增長是否足夠?

爲了證明其市銷率是合理的,QingCloud Technologies需要實現超過該行業的驚人增長。

如果我們回顧一下去年的收入增長,該公司公佈了9.9%的可觀增長。但是,最終,它無法扭轉前一時期的糟糕表現,在過去三年中,總收入下降了22%。因此,不幸的是,我們必須承認,在這段時間內,該公司在增加收入方面做得不好。

與該公司形成鮮明對比的是,該行業的其他部門預計將在明年增長40%,這確實可以看出該公司最近的中期收入下降。

有鑑於此,令人震驚的是,青雲科技的市銷率高於其他多數公司。看來大多數投資者都忽視了最近的糟糕增長率,並希望公司的業務前景有所好轉。只有最大膽的人才會假設這些價格是可持續的,因爲近期收入趨勢的延續最終可能會嚴重壓制股價。

青雲科技的市銷率對投資者意味着什麼?

QingCloud Technologies的市銷率仍然有所提高,儘管其最近的股價不能這樣說。儘管市銷率不應該成爲決定你是否買入股票的決定性因素,但它是衡量收入預期的有力晴雨表。

我們已經確定,QingCloud Technologies目前的市銷率遠高於預期,因爲其最近的收入在中期內有所下降。目前,我們對高市銷率不滿意,因爲這種收入表現極不可能長期支撐這種積極情緒。如果最近的中期收入趨勢持續下去,將對現有股東的投資構成重大風險,潛在投資者將很難接受股票的當前價值。

你應該時刻考慮風險。舉個例子,我們發現了你應該注意的青雲科技的兩個警告信號,其中一個有點不愉快。

如果這些風險讓你重新考慮你對QingCloud Technologies的看法,請瀏覽我們的高質量股票互動清單,了解還有什麼。

對這篇文章有反饋嗎?對內容感到擔憂?直接聯繫我們。 或者,給編輯團隊 (at) simplywallst.com 發送電子郵件。

Simply Wall St的這篇文章本質上是籠統的。我們僅使用公正的方法根據歷史數據和分析師的預測提供評論,我們的文章無意作爲財務建議。它不構成買入或賣出任何股票的建議,也沒有考慮到您的目標或財務狀況。我們的目標是爲您提供由基本數據驅動的長期重點分析。請注意,我們的分析可能不考慮最新的價格敏感型公司公告或定性材料。簡而言之,華爾街沒有持有任何上述股票的頭寸。

譯文內容由第三人軟體翻譯。

風險及免責聲明

- 分享到weixin

- 分享到qq

- 分享到facebook

- 分享到twitter

- 分享到微博

- 粘贴板

使用瀏覽器的分享功能,分享給你的好友吧