There's No Escaping Journey Medical Corporation's (NASDAQ:DERM) Muted Revenues Despite A 30% Share Price Rise

There's No Escaping Journey Medical Corporation's (NASDAQ:DERM) Muted Revenues Despite A 30% Share Price Rise

Those holding Journey Medical Corporation (NASDAQ:DERM) shares would be relieved that the share price has rebounded 30% in the last thirty days, but it needs to keep going to repair the recent damage it has caused to investor portfolios. The annual gain comes to 195% following the latest surge, making investors sit up and take notice.

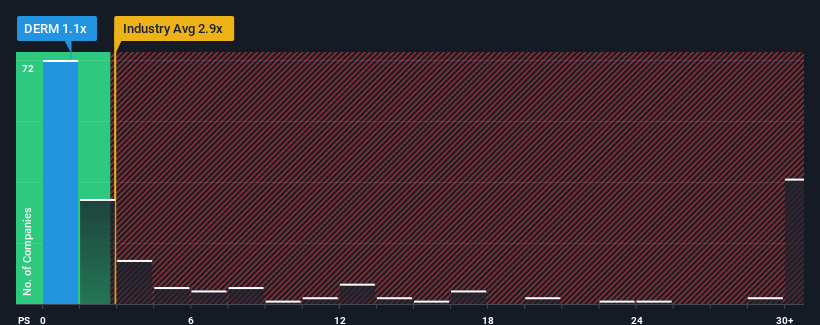

In spite of the firm bounce in price, Journey Medical may still be sending buy signals at present with its price-to-sales (or "P/S") ratio of 1.1x, considering almost half of all companies in the Pharmaceuticals industry in the United States have P/S ratios greater than 2.9x and even P/S higher than 16x aren't out of the ordinary. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's limited.

What Does Journey Medical's Recent Performance Look Like?

With revenue growth that's inferior to most other companies of late, Journey Medical has been relatively sluggish. Perhaps the market is expecting the current trend of poor revenue growth to continue, which has kept the P/S suppressed. If this is the case, then existing shareholders will probably struggle to get excited about the future direction of the share price.

Keen to find out how analysts think Journey Medical's future stacks up against the industry? In that case, our free report is a great place to start.Is There Any Revenue Growth Forecasted For Journey Medical?

There's an inherent assumption that a company should underperform the industry for P/S ratios like Journey Medical's to be considered reasonable.

Retrospectively, the last year delivered a decent 7.5% gain to the company's revenues. This was backed up an excellent period prior to see revenue up by 78% in total over the last three years. So we can start by confirming that the company has done a great job of growing revenues over that time.

Turning to the outlook, the next three years should generate growth of 0.2% per annum as estimated by the dual analysts watching the company. Meanwhile, the rest of the industry is forecast to expand by 14% per annum, which is noticeably more attractive.

With this information, we can see why Journey Medical is trading at a P/S lower than the industry. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The Key Takeaway

Journey Medical's stock price has surged recently, but its but its P/S still remains modest. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

As expected, our analysis of Journey Medical's analyst forecasts confirms that the company's underwhelming revenue outlook is a major contributor to its low P/S. At this stage investors feel the potential for an improvement in revenue isn't great enough to justify a higher P/S ratio. The company will need a change of fortune to justify the P/S rising higher in the future.

And what about other risks? Every company has them, and we've spotted 4 warning signs for Journey Medical (of which 1 is significant!) you should know about.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

那些持有Journey Medical Corporation(納斯達克股票代碼:DERM)股票的人會鬆一口氣,因爲股價在過去三十天中反彈了30%,但它需要繼續修復最近對投資者投資組合造成的損失。在最近的激增之後,年收益達到195%,這使投資者坐下來注意了。

儘管價格穩步反彈,但Journey Medical目前可能仍在發出買入信號,其市銷率(或 “市盈率”)爲1.1倍,因爲美國製藥行業幾乎有一半公司的市銷率大於2.9倍,即使市盈率高於16倍也並非不尋常。但是,僅按面值計算市銷率是不明智的,因爲可以解釋其有限的原因。

Journey Medical最近的表現如何?

由於最近的收入增長不及大多數其他公司,Journey Medical一直相對疲軟。也許市場預計當前收入增長不佳的趨勢將繼續下去,這使市銷售率一直受到抑制。如果是這樣的話,那麼現有股東可能很難對股價的未來走向感到興奮。

想了解分析師如何看待Journey Medical的未來與行業的對立嗎?在這種情況下,我們的免費報告是一個很好的起點。預計Journey Medical的收入會增長嗎?

人們固有的假設是,如果像Journey Medical這樣的市銷率被認爲是合理的,公司的表現應該低於該行業。

回顧過去,去年的公司收入實現了7.5%的可觀增長。在過去三年中,總收入增長了78%,此前這是一個很好的時期。因此,我們可以首先確認該公司在此期間在增加收入方面做得很好。

談到前景,根據關注該公司的雙重分析師的估計,未來三年將實現每年0.2%的增長。同時,預計該行業的其他部門每年將增長14%,這明顯更具吸引力。

通過這些信息,我們可以了解爲何Journey Medical的市銷率低於該行業。顯然,許多股東不願堅持下去,而該公司可能正在考慮不那麼繁榮的未來。

關鍵要點

Journey Medical的股價最近飆升,但其市銷率仍然不高。通常,在做出投資決策時,我們謹慎行事,不要過多地考慮市售比率,儘管這可以揭示其他市場參與者對公司的看法。

正如預期的那樣,我們對Journey Medical分析師預測的分析證實,該公司糟糕的收入前景是其低市銷率的主要原因。在現階段,投資者認爲,收入改善的可能性不足以證明更高的市銷率是合理的。該公司將需要改變命運,以證明未來市銷率上升是合理的。

那其他風險呢?每家公司都有,我們發現了 Journey Medical 的 4 個警告信號(其中 1 個很重要!)你應該知道。

如果你喜歡實力雄厚的公司盈利,那麼你會想看看這份以低市盈率(但已證明可以增加收益)的有趣公司的免費名單。

對這篇文章有反饋嗎?對內容感到擔憂?直接聯繫我們。 或者,給編輯團隊 (at) simplywallst.com 發送電子郵件。

Simply Wall St的這篇文章本質上是籠統的。我們僅使用公正的方法根據歷史數據和分析師的預測提供評論,我們的文章無意作爲財務建議。它不構成買入或賣出任何股票的建議,也沒有考慮到您的目標或財務狀況。我們的目標是爲您提供由基本數據驅動的長期重點分析。請注意,我們的分析可能不考慮最新的價格敏感型公司公告或定性材料。簡而言之,華爾街沒有持有任何上述股票的頭寸。

譯文內容由第三人軟體翻譯。

風險及免責聲明

- 分享到weixin

- 分享到qq

- 分享到facebook

- 分享到twitter

- 分享到微博

- 粘贴板

使用瀏覽器的分享功能,分享給你的好友吧