三大美股指收跌超1%,道指再创硅谷银行倒闭以来最大周跌,标普周跌幅五个月最大。科技“七姐妹”仅苹果收涨、一周涨超4%,芯片股指跌超3%,英特尔收跌超5%,AMD跌超4%;摩根大通创近四年最大跌幅。中概股指收跌4.6%,小鹏汽车跌近10%,蔚来跌近8%。泛欧股指反弹仍连跌两周,油气板块涨2.5%至2008年来新高。十年期美债收益率盘中较周四的近五个月高位回落10个基点。美元指数创五个月新高;日元三日连创1990年来新低;离岸人民币盘中跌超百点下逼7.27。比特币一度跌超6000美元、跌穿6.6万美元。原油反弹但全周累跌,美油盘中涨超3%创近半年新高,后回吐过半涨幅。黄金连创盘中历史新高后转跌,一度较高位回落4%。伦铜反弹至近两年高位,伦锡一周涨12%。

拉开财报季序幕的华尔街大行财报引发投资者对高利率冲击银行的忧虑。中东地缘紧张局势升级,助长原油等商品走高,进一步加剧高通胀持久的担忧。周四刚有反弹起色的美股大盘掉头下行,三大股指齐跌超1%,因周五回落,纳指抹平本周累计涨幅,和标普、道指均连跌两周,道指继上周后再创硅谷银行倒闭以来最惨周跌。

周五公布的财报显示,即使是最大银行也面临更高的利率挑战。一季度摩根大通、富国银行和花旗的关键指标净利息收入(NII)分别环比下降4%、4%和2%。摩根大通的NII略低于预期,终结连续七季创纪录之势,不计市场业务的NII指引上调10亿美元后仍低于预期。CEO戴蒙警告持久的通胀压力影响经济,称对“多种重大不确定因素”保持警惕。摩根大通股价重挫,创将近四年来最差单日表现。

周四强力支持大盘的科技巨头大多回落,仅传出酝酿Mac全线采用AI加持M4芯片消息的苹果早盘保住涨势,午盘曾转跌。媒体称,中国电信运营商将推行三年内网络核心部件的国产芯片替代。芯片股带头打压大盘,AMD和英特尔曾均跌超5%,英伟达回吐周三和周四大反弹的大部分涨幅,本周险些累跌。

据参考消息援引媒体报道,美国情报显示,伊朗可能在未来24至48小时内对以色列领土发动袭击。此外,白宫周五表示,伊朗对以色列进行报复性打击是“真实”、“可信”的威胁,美方密切关注。据央视报道,以色列国防部长加兰特周五会见到访的美国中央司令部司令库里拉,讨论应对伊朗可能发动的袭击。

地缘风险激发市场避险情绪,美国国债价格反弹,美元走强。上测4.60%、处于近五个月高位的基准十年期美债收益率持续下行,和对利率敏感的两年期美债收益率均一度回落超过10个基点,本周仍集体累计攀升逾10个基点,体现3月CPI再度超预期增长、美联储官员一再放话暗示不急于降息后,市场对联储的降息预期明显降温。

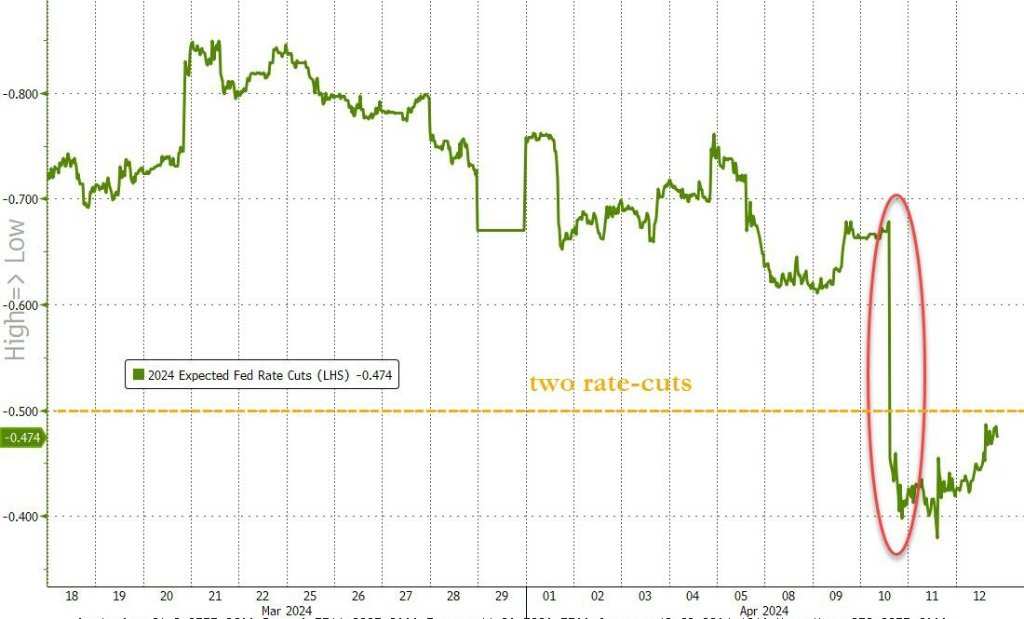

到本周,市场预计的今年美联储降息次数降至不足两次

到本周,市场预计的今年美联储降息次数降至不足两次美元指数继续上探去年11月以来高位,欧元和英镑均跌至五个月低谷,在欧洲央行暗示年中有望降息,同时市场预计的美联储首次降息时间推迟到9月之际,本周美元强劲反弹。周四日本官员再度警告可能干预汇市,财相铃木俊一称不排除采取任何措施应对汇率过度波动,日元周五连续第三日创1990年来新低,后虽抹平日内跌幅,但全周颓势不改。风险资产遭抛售,加密货币未能幸免。比特币盘中跳水,一度跌穿较日高跌去超过6000美元,抹平本周内所有涨幅,尽管周一冲向上月所创的历史高位,本周仍累跌收官。

大宗商品中,多种工业金属走高,中国公布进口铜矿强劲、1到3月进口量增长超5%后,伦铜反弹至将近两年来高位,今年内累计涨幅扩大到10%以上。评论称,投资者押注,矿石供应减少将难以跟上不断增长的全球需求。地缘风险助推下,黄金再创盘中历史新高后跳水,但美股午盘纽约期金和现货黄金双双转跌,一度较高位回落4%,全周涨势不改。

地缘局势推升供应干扰风险,国际原油盘中强劲反弹,美油一度涨超3%至近半年来高位,后回吐过半涨幅。周五反弹未能扭转原油全周跌势,美联储降息预期时间推迟、国际能源署(IEA)下调今年油需增长预期、美国上周原油库存不降反增,都是打压油价因素。

周五黄金、比特币盘中跳水、原油冲高回落、回吐多数盘中涨幅

周五黄金、比特币盘中跳水、原油冲高回落、回吐多数盘中涨幅道指连创逾一年最大周跌 科技“七姐妹”仅苹果收涨 摩根大通创近四年最大跌幅 小盘股、芯片股和中概股跑输大盘

三大美国股指总体低开低走。午盘跌幅均超过1%,刷新日低时,纳斯达克综合指数跌逾1.9%,标普500指数跌近1.8%,道琼斯工业平均指数跌超580点,跌逾1.5%,最终继周三之后本周第二日集体收跌,道指本周第二日跌超1%、连跌五日。

道指收跌475.84点,跌幅1.24%,报37983.24点,1月24日以来首次收盘跌穿38000点。周四反弹的标普收跌1.46%,创1月31日鲍威尔讲话打击3月降息预期以来最大跌幅,报5123.41点,刷新3月15日以来收盘低位。周四反弹至创纪录收盘高位的纳指收跌1.62%,创3月5日以来最大跌幅,报16175.09点,刷新4月4日以来一周低位。

![标普500指数收创近一个月新低,中盘股收创两个月新低]() 标普500指数收创近一个月新低,中盘股收创两个月新低

标普500指数收创近一个月新低,中盘股收创两个月新低价值股为主的小盘股指罗素2000收跌1.93%,跑输大盘,回落到2月21日以来低位。科技股为重的纳斯达克100指数收跌1.66%,在周四反弹至3月22日以来高位后回落到4月4日以来低位。衡量纳斯达克100指数中科技业成份股表现的纳斯达克科技市值加权指数(NDXTMC)收跌1.84%,跌落周四反弹所创的收盘历史高位,本周累涨0.01%。

本周主要美股指全线累跌,道指累跌2.37%,刷新上周所创的2023年3月10日一周、即硅谷银行倒闭当周以来最大周跌幅,标普累跌1.56%,创2023年10月27日一周以来最大周跌幅,和累跌2.92%的罗素2000均连跌两周。纳指累跌0.45%,纳斯达克100跌0.58%,均连跌三周。

![本周主要美股指总体周三CPI公布后大跌,周四PPI公布后有所反弹,周五又大跌]() 本周主要美股指总体周三CPI公布后大跌,周四PPI公布后有所反弹,周五又大跌

本周主要美股指总体周三CPI公布后大跌,周四PPI公布后有所反弹,周五又大跌标普500各大板块全军覆没,除跌逾0.7%的公用事业和跌0.9%的必需消费品以外,其他板块收跌至少1%,材料收跌近1.8%领跌,芯片股所在的IT板块午盘曾跌近1.9%、收跌逾1.6%。本周这些板块均累跌,除了跌逾0.2%的IT、跌0.5%的通信服务、跌近0.7%的非必需消费品,其他板块至少跌超1%,金融跌3.6%领跌,材料、房产、医疗也均跌逾3%,工业跌超2%。

![标普500各板块ETF中,金融本周跌幅居首]() 标普500各板块ETF中,金融本周跌幅居首

标普500各板块ETF中,金融本周跌幅居首包括微软、苹果、英伟达、谷歌母公司Alphabet、亚马逊、Facebook母公司Meta、特斯拉在内,科技巨头“七姐妹”盘中均曾下跌,仅苹果收涨。特斯拉午盘曾跌超2%,收跌约2%,抹平周四反弹的涨幅,在上周公布一季度交付量远逊预期当周大跌超6%后,本周有所反弹,累涨3.73%。

FAANMG六大科技股中,Meta收跌近2.2%,微软收跌1.4%,均回落至4月4日以来收盘低位;周四连涨四日至纪录高位的亚马逊收跌1.5%,周四反弹至纪录高位的Alphabet早盘曾刷新盘中历史高位、日内涨超0.4%,市值达2万亿美元,后转跌,收跌1%;奈飞早盘转跌后收跌近1%;而周四大涨超4%的苹果早盘曾涨近1.9%,后持续回吐涨幅,午盘曾短线转跌,收涨近0.9%。

这六大科技股本周涨跌各异,上周独跌的苹果本周累涨4.1%,表现最佳,Alphabet涨3.4%,亚马逊涨近0.6%,而Meta跌近3%,奈飞跌超2%,微软跌近0.9%。

芯片股总体回落、跑输大盘,费城半导体指数和半导体行业ETF SOXX均收跌约3.3%,回落至3月19日以来收盘低位,本周分别累跌近1.6%和约1.6%。芯片股中,英伟达收跌近2.7%,在连涨两日至3月26日以来收盘高位后回落,本周累涨0.2%;传出中国电信领域国产芯片替代的相关消息后,英特尔收跌近5.2%,AMD盘初曾跌超5%,收跌4.2%;收盘时,美光科技跌近4%,博通跌近3%,台积电美股跌超3%。

![苹果、英伟达等七大科技股本周总体小幅累涨]() 苹果、英伟达等七大科技股本周总体小幅累涨

苹果、英伟达等七大科技股本周总体小幅累涨AI概念股普跌,大多跑输大盘。 SoundHound.ai(SOUN)跌超8%,C3.ai(AI)跌超5%,超微电脑(SMCI)跌超4%,被称为“小英伟达”、出售数据中心互连芯片的Astera Labs(ALAB)跌近4%,Adobe(ADBE)跌超2%,甲骨文(ORCL)跌近2%,Palantir(PLTR)跌逾0.7%,BigBear.ai(BBAI)跌近0.6%。

银行股指数齐跌。整体银行业指标KBW银行指数(BKX)收跌近1.5%,连跌三日至3月15日以来低位,本周累跌近3.8%;地区银行指数KBW Nasdaq Regional Banking Index(KRX)收跌近0.8%,地区银行股ETF SPDR标普地区银行ETF(KRE)收跌近0.9%,均在周四反弹后回落到2023年11月30日以来低位,本周分别累跌约3.4%和3.5%。

公布财报的大银行中,摩根大通收跌近6.5%,创2020年6月11日以来最大跌幅;一季度NII也低于预期、管理层称无法提供有关监管方何时撤除对其资产上限时间的更新、具体时间最终取决于监管方后,富国银行盘初跌超2%,早盘几度转涨后小幅转跌,收跌近0.4%;一季度营收同比下降2%、利润下降27%仍高于预期的花旗盘初曾涨超1%,早盘转跌,午盘曾跌超3%,收跌1.7%。

其他大银行中,到收盘,高盛跌2%,美国银行跌1.5%,周四媒体称财务管理业务遭监管调查后跌超5%的摩根士丹利收跌近0.8%。此外,公布一季度管理资产规模同比增长15%至创纪录水平、但资金净流入规模几乎减半后,资管巨头贝莱德收跌近2.9%。

热门中概股多数下跌,跑输大盘。纳斯达克金龙中国指数(HXC)收跌近4.6%,本周因周五下挫而累跌3.22%,在上周反弹后回落,进入龙年以来九周内第四周累跌。中概ETF KWEB和CQQQ午盘分别跌超3%和2%。造车新势力中,小鹏汽车收跌近9.8%,蔚来汽车收跌近7.9%,理想汽车收跌4.7%,而小米粉单早盘涨近2%收平。其他个股中,收盘时,B站跌超6%,京东跌近6%,网易跌超5%,阿里巴巴、百度、拼多多跌超4%,腾讯粉单跌近3%。

波动较大的个股中,媒体曝出其治疗关节炎药物Librela 和 Solensia可能有副作用后,宠物药品公司Zoetis(ZTS)盘中跌超8%,收跌7.8%;在Fuzzy Panda Research发布沽空报告指控其保险欺诈次日,人寿险公司Globe Life(GL)收涨近20.2%,仍未抹平发布报告当天周四超过50%的跌幅。

欧股方面,能源股力挺周四回落的泛欧股指反弹。欧洲斯托克600指数暂别周四刷新的3月18日以来收盘低位。主要欧洲国家股指涨跌互见。德股和法股分别连跌两日和四日,而英股逼近去年2月所创的收盘历史高位,和意股均在周四回落后反弹,连跌五日的西班牙股指也反弹。

各板块中,原油力挺的油气收涨近2.5%,创2008年来新高,成分股中,伦敦上市的BP涨近3.7%、壳牌涨2.8%,巴黎上市的道达尔涨逾2%,股价创历史新高;得益于铜价创近两年新高,矿业股所在的基础资源涨2.4%,伦敦上市的成分股嘉能可收涨约5%,和油气股共同支持英国股指在欧洲各国中表现最佳,而汽车和旅游板块收跌近1.2%。

本周斯托克600指数在连涨十周后连跌两周,但跌幅不及跌近1.2%、创1月19日以来最大跌幅的上周。各国股指大多连跌两周,英股一枝独秀,在上周回落后反弹。各板块中,基础资源累涨超4%,油气涨近4%,尽显商品突出表现,而受累于周五下跌的旅游板块跌超2%,银行和奢侈品巨头所在的个人与家庭用品跌近2%,对利率敏感的房产跌超1%。

十年期美债收益率盘中较周四高位回落10个基点 本周仍升逾10个基点

美国10年期基准国债收益率在亚市早盘上逼4.59%,逼近周四刷新的2023年11月14日以来高位,后持续下行,美股盘前下破4.50%,美股早盘曾下侧4.48%刷新日低,较日高回落超过10个基点,到债市尾盘时约为4.52%,日内降近6个基点,在连升两日后回落,本周累计升约12个基点,连升两周。

对利率前景更敏感的2年期美债收益率在亚市早盘曾处于4.95%上方,美股盘前曾下破4.86%刷新日低,较日内高位回落逾10个基点,也远离周四突破5.0%所创的2023年11月14日以来高位,到债市尾盘时约为4.90%,日内降约6个基点,连降两日,本周仍累计升约15个基点,连升三周。

![美债收益率周五回落,但全周集体攀升,短债的收益率升幅居前]() 美债收益率周五回落,但全周集体攀升,短债的收益率升幅居前

美债收益率周五回落,但全周集体攀升,短债的收益率升幅居前美元指数创五个月新高 日元三日连创1990年来新低 比特币一度跳水超6000美元

追踪美元兑欧元等六种主要货币一篮子汇价的ICE美元指数(DXY)在亚市早盘早盘微幅转跌时下逼105.20刷新日低,欧美交易时段持续上行,美股早盘,自2023年11月10日以来首次涨破106.00,后曾涨破106.10, 刷新2023年11月3日以来高位,日内涨近0.8%。

到周五美股收盘时,美元指数略高于106.00,日内涨近0.7%,在上周回落后本周累涨超1.6%;追踪美元兑其他十种货币汇率的彭博美元现货指数日内涨近0.7%,两日刷新2023年11月13日以来同时段高位,在连跌两周后本周累涨逾1.3%,和美元指数均连涨三日、创2022年9月以来最大周涨幅。

![彭博美元现货指数处于去年11月以来高位,本周创2022年9月以来最大周涨幅]() 彭博美元现货指数处于去年11月以来高位,本周创2022年9月以来最大周涨幅

彭博美元现货指数处于去年11月以来高位,本周创2022年9月以来最大周涨幅非美货币大多下跌,欧元兑美元在美股早盘曾跌破1.0630,刷新2023年10月末以来低位,日内跌逾0.9%,美股收盘时处于1.0640上方;英镑兑美元 在美股早盘曾跌破1.2430,刷新2023年11月以来低位,日内跌近1%,美股收盘时徘徊1.2450;而日元再创1990年来新低后小幅转涨,美元兑日元在欧股盘前曾逼近153.40,连续第三日创1990年来新高,日内涨不足0.1%,欧股盘中转跌后美股盘前跌破152.60刷新日低,日内跌超0.4%,美股收盘时日内微跌。

离岸人民币(CNH)兑美元在亚市早盘刷新日高至7.2531,亚市盘中转跌后保持跌势,欧股盘中曾险些失守7.27至7.2690,刷新3月25日来低位,较日高回落159点。北京时间4月13日4点59分,离岸人民币兑美元报7.2673元,较周四纽约尾盘跌115点,在周四反弹后回落,在连涨两周后本周累跌195点。

比特币(BTC)在亚市早盘曾涨破7.1万美元刷新日高,欧股盘中起加速下跌,美股盘初跌破7万美元,午盘跌破6.6万美元,部分平台跌至6.52万美元下方,较日高跌超6000美元、跌近9%,刷新4月4日上周四以来低位,远离周一涨破7.27万美元所创的3月14日以来盘中高位,后跌幅收窄,重上6.7万美元,美股收盘时处于6.72万美元上方,最近24小时跌近5%,最近七日累计跌不足1%。

![周五跳水后,比特币抹平本周前几日涨幅、累计转跌]() 周五跳水后,比特币抹平本周前几日涨幅、累计转跌

周五跳水后,比特币抹平本周前几日涨幅、累计转跌原油反弹但全周累跌 美油盘中涨超3%后回吐过半涨幅

周四回落的国际原油期货周五全天保持涨势,美股早盘,美国WTI曾原油靠近87.70美元,刷新2023年10月下旬以来盘中高位,日内涨约3.1%,布伦特原油曾接近92.20美元,日内涨约2.7%,后逐步回吐大部分盘中涨幅。

最终,WTI 5月原油期货收涨0.64美元,涨幅超过0.75%,报85.66美元/桶,告别周四报85.02美元刷新的4月1日收报83.71美元以来收盘低位;布伦特6月原油期货收涨0.71美元,涨幅0.79%,报90.45美元/桶 ,收复周四失守的90美元关口。

本周美油累跌近1.44%,布油本周累跌近0.8%,均在连涨两周后回落,最近13周内第七周累跌,也是巴以冲突爆发以来27周内第15周累跌,在一季度大涨超10%后,二季度第二周未能保住涨势。

![国际原油周五冲高回落,周五反弹未能扭转全周累跌]() 国际原油周五冲高回落,周五反弹未能扭转全周累跌

国际原油周五冲高回落,周五反弹未能扭转全周累跌美国汽油和天然气期货齐反弹。周四止步两连阳的NYMEX 5月汽油期货收涨约1%,报2.8029美元/加仑,本周累涨约0.5%,连涨三周;NYMEX 5月天然气期货收涨0.34%,报1.770美元/百万英热单位,告别周四回落刷新的3月28日以来低位,在上周反弹后本周累跌0.84%。

伦铜反弹至近两年高位,伦锡一周涨12% 黄金连创盘中历史新高 后一度较高位回落4%

伦敦基本金属期货周五大多上涨。伦锌涨超2.5%,连涨五日,四日创去年4月以来新高。周四回落的伦锡涨逾2%,和连跌两日的伦铜均反弹至2022年6月以来高位。两连跌的伦铝反弹至去年2月以来高位。周四回落的伦铅刷新周三所创的1月末以来新高。而伦镍连跌两日,继续跌离连涨八日所创的四周来高位。

本周这些金属多数继续累涨,领涨的伦锡涨逾12%,伦锌涨超7%,伦铜涨超1%,均连涨两周,伦铝涨近2%,连涨五周,伦铅涨超2%,连涨三周,而上周反弹超6%的伦镍微幅累跌。

周五美股早盘,纽约黄金期货曾接近2449美元至2448.8美元,日内涨约3.2%,现货黄金曾涨至2431美元上方,日内涨近2.5%,均连续第二日创盘中历史新高,后持续回落,美股午盘均转跌。

期金转跌前已收盘,COMEX 6月黄金期货收涨0.06%,报2374.1美元/盎司,连续两日、本周第三日创收盘最高纪录,本周累涨1.23%,连涨三周,巴以冲突爆发以来27周内第19周累涨,涨幅远不及涨近4.8%的上周,上周创去年10月巴以冲突升级当周以来最大周涨幅。

收盘后美股午盘刷新日低时,期金曾跌至2350.6美元,日内跌逾0.9%,现货黄金跌至2334美元下方,日内跌逾1.6%,均较日内高位跌去约4%。美股收盘时,现货黄金处于2340美元上方,日内跌逾1.2%,仍连涨四周。

![现货黄金盘中创历史新高后一度较高位回落4%]() 现货黄金盘中创历史新高后一度较高位回落4%

现货黄金盘中创历史新高后一度较高位回落4%编辑/tolk

三大美股指收跌超1%,道指再創硅谷銀行倒閉以來最大周跌,標普周跌幅五個月最大。科技“七姐妹”僅蘋果收漲、一週漲超4%,芯片股指跌超3%,英特爾收跌超5%,AMD跌超4%;摩根大通創近四年最大跌幅。中概股指收跌4.6%,小鵬汽車跌近10%,蔚來跌近8%。泛歐股指反彈仍連跌兩週,油氣板塊漲2.5%至2008年來新高。十年期美債收益率盤中較週四的近五個月高位回落10個點子。美元指數創五個月新高;日元三日連創1990年來新低;離岸人民幣盤中跌超百點下逼7.27。比特幣一度跌超6000美元、跌穿6.6萬美元。原油反彈但全周累跌,美油盤中漲超3%創近半年新高,後回吐過半漲幅。黃金連創盤中歷史新高後轉跌,一度較高位回落4%。倫銅反彈至近兩年高位,倫錫一週漲12%。

拉開業績季序幕的華爾街大行業績引發投資者對高利率衝擊銀行的憂慮。中東地緣緊張局勢升級,助長原油等商品走高,進一步加劇高通脹持久的擔憂。週四剛有反彈起色的美股大盤掉頭下行,三大股指齊跌超1%,因週五回落,納指抹平本週累計漲幅,和標普、道指均連跌兩週,道指繼上週後再創硅谷銀行倒閉以來最慘周跌。

週五公佈的業績顯示,即使是最大銀行也面臨更高的利率挑戰。一季度摩根大通、富國銀行和花旗的關鍵指標淨利息收入(NII)分別環比下降4%、4%和2%。摩根大通的NII略低於預期,終結連續七季創紀錄之勢,不計市場業務的NII指引上調10億美元后仍低於預期。CEO戴蒙警告持久的通脹壓力影響經濟,稱對“多種重大不確定因素”保持警惕。摩根大通股價重挫,創將近四年來最差單日表現。

週四強力支持大盤的科技巨頭大多回落,僅傳出醞釀Mac全線採用AI加持M4芯片消息的蘋果早盤保住漲勢,午盤曾轉跌。媒體稱,中國電信運營商將推行三年內網絡核心部件的國產芯片替代。芯片股帶頭打壓大盤,AMD和英特爾曾均跌超5%,英偉達回吐週三和週四大反彈的大部分漲幅,本週險些累跌。

據參考消息援引媒體報道,美國情報顯示,伊朗可能在未來24至48小時內對以色列領土發動襲擊。此外,白宮週五表示,伊朗對以色列進行報復性打擊是“真實”、“可信”的威脅,美方密切關注。據央視報道,以色列國防部長加蘭特週五會見到訪的美國中央司令部司令庫里拉,討論應對伊朗可能發動的襲擊。

地緣風險激發市場避險情緒,美國國債價格反彈,美元走強。上測4.60%、處於近五個月高位的基準十年期美債收益率持續下行,和對利率敏感的兩年期美債收益率均一度回落超過10個點子,本週仍集體累計攀升逾10個點子,體現3月CPI再度超預期增長、聯儲局官員一再放話暗示不急於降息後,市場對聯儲的降息預期明顯降溫。

到本週,市場預計的今年聯儲局降息次數降至不足兩次 美元指數繼續上探去年11月以來高位,歐元和英鎊均跌至五個月低谷,在歐洲央行暗示年中有望降息,同時市場預計的聯儲局首次降息時間推遲到9月之際,本週美元強勁反彈。週四日本官員再度警告可能干預匯市,財相鈴木俊一稱不排除採取任何措施應對匯率過度波動,日元週五連續第三日創1990年來新低,後雖抹平日內跌幅,但全周頹勢不改。風險資產遭拋售,加密貨幣未能倖免。比特幣盤中跳水,一度跌穿較日高跌去超過6000美元,抹平本週內所有漲幅,儘管週一衝向上月所創的歷史高位,本週仍累跌收官。

大宗商品中,多種工業金屬走高,中國公佈進口銅礦強勁、1到3月進口量增長超5%後,倫銅反彈至將近兩年來高位,今年內累計漲幅擴大到10%以上。評論稱,投資者押注,礦石供應減少將難以跟上不斷增長的全球需求。地緣風險助推下,黃金再創盤中歷史新高後跳水,但美股午盤紐約期金和現貨黃金雙雙轉跌,一度較高位回落4%,全周漲勢不改。

地緣局勢推升供應干擾風險,國際原油盤中強勁反彈,美油一度漲超3%至近半年來高位,後回吐過半漲幅。週五反彈未能扭轉原油全周跌勢,聯儲局降息預期時間推遲、國際能源署(IEA)下調今年油需增長預期、美國上週原油庫存不降反增,都是打壓油價因素。

週五黃金、比特幣盤中跳水、原油衝高回落、回吐多數盤中漲幅 道指連創逾一年最大周跌 科技“七姐妹”僅蘋果收漲 摩根大通創近四年最大跌幅 小盤股、芯片股和中概股跑輸大盤

三大美國股指總體低開低走。午盤跌幅均超過1%,刷新日低時,納斯達克綜合指數跌逾1.9%,標普500指數跌近1.8%,道瓊斯工業平均指數跌超580點,跌逾1.5%,最終繼週三之後本週第二日集體收跌,道指本週第二日跌超1%、連跌五日。

道指收跌475.84點,跌幅1.24%,報37983.24點,1月24日以來首次收盤跌穿38000點。週四反彈的標普收跌1.46%,創1月31日鮑威爾講話打擊3月降息預期以來最大跌幅,報5123.41點,刷新3月15日以來收盤低位。週四反彈至創紀錄收盤高位的納指收跌1.62%,創3月5日以來最大跌幅,報16175.09點,刷新4月4日以來一週低位。

![標普500指數收創近一個月新低,中盤股收創兩個月新低]() 標普500指數收創近一個月新低,中盤股收創兩個月新低

標普500指數收創近一個月新低,中盤股收創兩個月新低價值股爲主的小盤股指羅素2000收跌1.93%,跑輸大盤,回落到2月21日以來低位。科技股爲重的納斯達克100指數收跌1.66%,在週四反彈至3月22日以來高位後回落到4月4日以來低位。衡量納斯達克100指數中科技業成份股表現的納斯達克科技市值加權指數(NDXTMC)收跌1.84%,跌落週四反彈所創的收盤歷史高位,本週累漲0.01%。

本週主要美股指全線累跌,道指累跌2.37%,刷新上週所創的2023年3月10日一週、即硅谷銀行倒閉當週以來最大周跌幅,標普累跌1.56%,創2023年10月27日一週以來最大周跌幅,和累跌2.92%的羅素2000均連跌兩週。納指累跌0.45%,納斯達克100跌0.58%,均連跌三週。

![本週主要美股指總體週三CPI公佈後大跌,週四PPI公佈後有所反彈,週五又大跌]() 本週主要美股指總體週三CPI公佈後大跌,週四PPI公佈後有所反彈,週五又大跌

本週主要美股指總體週三CPI公佈後大跌,週四PPI公佈後有所反彈,週五又大跌標普500各大板塊全軍覆沒,除跌逾0.7%的公用事業和跌0.9%的必需消費品以外,其他板塊收跌至少1%,材料收跌近1.8%領跌,芯片股所在的IT板塊午盤曾跌近1.9%、收跌逾1.6%。本週這些板塊均累跌,除了跌逾0.2%的IT、跌0.5%的通信服務、跌近0.7%的非必需消費品,其他板塊至少跌超1%,金融跌3.6%領跌,材料、房產、醫療也均跌逾3%,工業跌超2%。

![標普500各板塊ETF中,金融本週跌幅居首]() 標普500各板塊ETF中,金融本週跌幅居首

標普500各板塊ETF中,金融本週跌幅居首包括微軟、蘋果、英偉達、谷歌母公司Alphabet、亞馬遜、Facebook母公司Meta、特斯拉在內,科技巨頭“七姐妹”盤中均曾下跌,僅蘋果收漲。特斯拉午盤曾跌超2%,收跌約2%,抹平週四反彈的漲幅,在上週公佈一季度交付量遠遜預期當週大跌超6%後,本週有所反彈,累漲3.73%。

FAANMG六大科技股中,Meta收跌近2.2%,微軟收跌1.4%,均回落至4月4日以來收盤低位;週四連漲四日至紀錄高位的亞馬遜收跌1.5%,週四反彈至紀錄高位的Alphabet早盤曾刷新盤中歷史高位、日內漲超0.4%,市值達2萬億美元,後轉跌,收跌1%;奈飛早盤轉跌後收跌近1%;而週四大漲超4%的蘋果早盤曾漲近1.9%,後持續回吐漲幅,午盤曾短線轉跌,收漲近0.9%。

這六大科技股本週漲跌各異,上週獨跌的蘋果本週累漲4.1%,表現最佳,Alphabet漲3.4%,亞馬遜漲近0.6%,而Meta跌近3%,奈飛跌超2%,微軟跌近0.9%。

芯片股總體回落、跑輸大盤,費城半導體指數和半導體行業ETF SOXX均收跌約3.3%,回落至3月19日以來收盤低位,本週分別累跌近1.6%和約1.6%。芯片股中,英偉達收跌近2.7%,在連漲兩日至3月26日以來收盤高位後回落,本週累漲0.2%;傳出中國電信領域國產芯片替代的相關消息後,英特爾收跌近5.2%,AMD盤初曾跌超5%,收跌4.2%;收盤時,美光科技跌近4%,博通跌近3%,台積電美股跌超3%。

![蘋果、英偉達等七大科技股本週總體小幅累漲]() 蘋果、英偉達等七大科技股本週總體小幅累漲

蘋果、英偉達等七大科技股本週總體小幅累漲AI概念股普跌,大多跑輸大盤。 SoundHound.ai(SOUN)跌超8%,C3.ai(AI)跌超5%,超微電腦(SMCI)跌超4%,被稱爲“小英偉達”、出售數據中心互連芯片的Astera Labs(ALAB)跌近4%,Adobe(ADBE)跌超2%,甲骨文(ORCL)跌近2%,Palantir(PLTR)跌逾0.7%,BigBear.ai(BBAI)跌近0.6%。

銀行股指數齊跌。整體銀行業指標KBW銀行指數(BKX)收跌近1.5%,連跌三日至3月15日以來低位,本週累跌近3.8%;地區銀行指數KBW Nasdaq Regional Banking Index(KRX)收跌近0.8%,地區銀行股ETF SPDR標普地區銀行ETF(KRE)收跌近0.9%,均在週四反彈後回落到2023年11月30日以來低位,本週分別累跌約3.4%和3.5%。

公佈業績的大銀行中,摩根大通收跌近6.5%,創2020年6月11日以來最大跌幅;一季度NII也低於預期、管理層稱無法提供有關監管方何時撤除對其資產上限時間的更新、具體時間最終取決於監管方後,富國銀行盤初跌超2%,早盤幾度轉漲後小幅轉跌,收跌近0.4%;一季度營收同比下降2%、利潤下降27%仍高於預期的花旗盤初曾漲超1%,早盤轉跌,午盤曾跌超3%,收跌1.7%。

其他大銀行中,到收盤,高盛跌2%,美國銀行跌1.5%,週四媒體稱財務管理業務遭監管調查後跌超5%的摩根士丹利收跌近0.8%。此外,公佈一季度管理資產規模同比增長15%至創紀錄水平、但資金淨流入規模幾乎減半後,資管巨頭貝萊德收跌近2.9%。

熱門中概股多數下跌,跑輸大盤。納斯達克金龍中國指數(HXC)收跌近4.6%,本週因週五下挫而累跌3.22%,在上週反彈後回落,進入龍年以來九周內第四周累跌。中概ETF KWEB和CQQQ午盤分別跌超3%和2%。造車新勢力中,小鵬汽車收跌近9.8%,蔚來汽車收跌近7.9%,理想汽車收跌4.7%,而小米粉單早盤漲近2%收平。其他個股中,收盤時,B站跌超6%,京東跌近6%,網易跌超5%,阿里巴巴、百度、拼多多跌超4%,騰訊粉單跌近3%。

波動較大的個股中,媒體曝出其治療關節炎藥物Librela 和 Solensia可能有副作用後,寵物藥品公司Zoetis(ZTS)盤中跌超8%,收跌7.8%;在Fuzzy Panda Research發佈沽空報告指控其保險欺詐次日,人壽險公司Globe Life(GL)收漲近20.2%,仍未抹平發佈報告當天週四超過50%的跌幅。

歐股方面,能源股力挺週四回落的泛歐股指反彈。歐洲斯托克600指數暫別週四刷新的3月18日以來收盤低位。主要歐洲國家股指漲跌互見。德股和法股分別連跌兩日和四日,而英股逼近去年2月所創的收盤歷史高位,和意股均在週四回落後反彈,連跌五日的西班牙股指也反彈。

各板塊中,原油力挺的油氣收漲近2.5%,創2008年來新高,成分股中,倫敦上市的BP漲近3.7%、殼牌漲2.8%,巴黎上市的道達爾漲逾2%,股價創歷史新高;得益於銅價創近兩年新高,礦業股所在的基礎資源漲2.4%,倫敦上市的成分股嘉能可收漲約5%,和油氣股共同支持英國股指在歐洲各國中表現最佳,而汽車和旅遊板塊收跌近1.2%。

本週斯托克600指數在連漲十週後連跌兩週,但跌幅不及跌近1.2%、創1月19日以來最大跌幅的上週。各國股指大多連跌兩週,英股一枝獨秀,在上週回落後反彈。各板塊中,基礎資源累漲超4%,油氣漲近4%,盡顯商品突出表現,而受累於週五下跌的旅遊板塊跌超2%,銀行和奢侈品巨頭所在的個人與家庭用品跌近2%,對利率敏感的房產跌超1%。

十年期美債收益率盤中較週四高位回落10個點子 本週仍升逾10個點子

美國10年期基準國債收益率在亞市早盤上逼4.59%,逼近週四刷新的2023年11月14日以來高位,後持續下行,美股盤前下破4.50%,美股早盤曾下側4.48%刷新日低,較日高回落超過10個點子,到債市尾盤時約爲4.52%,日內降近6個點子,在連升兩日後回落,本週累計升約12個點子,連升兩週。

對利率前景更敏感的2年期美債收益率在亞市早盤曾處於4.95%上方,美股盤前曾下破4.86%刷新日低,較日內高位回落逾10個點子,也遠離週四突破5.0%所創的2023年11月14日以來高位,到債市尾盤時約爲4.90%,日內降約6個點子,連降兩日,本週仍累計升約15個點子,連升三週。

![美債收益率週五回落,但全周集體攀升,短債的收益率升幅居前]() 美債收益率週五回落,但全周集體攀升,短債的收益率升幅居前

美債收益率週五回落,但全周集體攀升,短債的收益率升幅居前美元指數創五個月新高 日元三日連創1990年來新低 比特幣一度跳水超6000美元

追蹤美元兌歐元等六種主要貨幣一籃子匯價的ICE美元指數(DXY)在亞市早盤早盤微幅轉跌時下逼105.20刷新日低,歐美交易時段持續上行,美股早盤,自2023年11月10日以來首次漲破106.00,後曾漲破106.10, 刷新2023年11月3日以來高位,日內漲近0.8%。

到週五美股收盤時,美元指數略高於106.00,日內漲近0.7%,在上週回落後本週累漲超1.6%;追蹤美元兌其他十種貨幣匯率的彭博美元現貨指數日內漲近0.7%,兩日刷新2023年11月13日以來同時段高位,在連跌兩週後本週累漲逾1.3%,和美元指數均連漲三日、創2022年9月以來最大周漲幅。

![彭博美元現貨指數處於去年11月以來高位,本週創2022年9月以來最大周漲幅]() 彭博美元現貨指數處於去年11月以來高位,本週創2022年9月以來最大周漲幅

彭博美元現貨指數處於去年11月以來高位,本週創2022年9月以來最大周漲幅非美貨幣大多下跌,歐元兌美元在美股早盤曾跌破1.0630,刷新2023年10月末以來低位,日內跌逾0.9%,美股收盤時處於1.0640上方;英鎊兌美元 在美股早盤曾跌破1.2430,刷新2023年11月以來低位,日內跌近1%,美股收盤時徘徊1.2450;而日元再創1990年來新低後小幅轉漲,美元兌日元在歐股盤前曾逼近153.40,連續第三日創1990年來新高,日內漲不足0.1%,歐股盤中轉跌後美股盤前跌破152.60刷新日低,日內跌超0.4%,美股收盤時日內微跌。

離岸人民幣(CNH)兌美元在亞市早盤刷新日高至7.2531,亞市盤中轉跌後保持跌勢,歐股盤中曾險些失守7.27至7.2690,刷新3月25日來低位,較日高回落159點。北京時間4月13日4點59分,離岸人民幣兌美元報7.2673元,較週四紐約尾盤跌115點,在週四反彈後回落,在連漲兩週後本週累跌195點。

比特幣(BTC)在亞市早盤曾漲破7.1萬美元刷新日高,歐股盤中起加速下跌,美股盤初跌破7萬美元,午盤跌破6.6萬美元,部分平台跌至6.52萬美元下方,較日高跌超6000美元、跌近9%,刷新4月4日上週四以來低位,遠離週一漲破7.27萬美元所創的3月14日以來盤中高位,後跌幅收窄,重上6.7萬美元,美股收盤時處於6.72萬美元上方,最近24小時跌近5%,最近七日累計跌不足1%。

![週五跳水後,比特幣抹平本週前幾日漲幅、累計轉跌]() 週五跳水後,比特幣抹平本週前幾日漲幅、累計轉跌

週五跳水後,比特幣抹平本週前幾日漲幅、累計轉跌原油反彈但全周累跌 美油盤中漲超3%後回吐過半漲幅

週四回落的國際原油期貨週五全天保持漲勢,美股早盤,美國WTI曾原油靠近87.70美元,刷新2023年10月下旬以來盤中高位,日內漲約3.1%,布倫特原油曾接近92.20美元,日內漲約2.7%,後逐步回吐大部分盤中漲幅。

最終,WTI 5月原油期貨收漲0.64美元,漲幅超過0.75%,報85.66美元/桶,告別週四報85.02美元刷新的4月1日收報83.71美元以來收盤低位;布倫特6月原油期貨收漲0.71美元,漲幅0.79%,報90.45美元/桶 ,收復週四失守的90美元關口。

本週美油累跌近1.44%,布油本週累跌近0.8%,均在連漲兩週後回落,最近13周內第七週累跌,也是巴以衝突爆發以來27周內第15周累跌,在一季度大漲超10%後,二季度第二週未能保住漲勢。

![國際原油週五衝高回落,週五反彈未能扭轉全周累跌]() 國際原油週五衝高回落,週五反彈未能扭轉全周累跌

國際原油週五衝高回落,週五反彈未能扭轉全周累跌美國汽油和天然氣期貨齊反彈。週四止步兩連陽的NYMEX 5月汽油期貨收漲約1%,報2.8029美元/加侖,本週累漲約0.5%,連漲三週;NYMEX 5月天然氣期貨收漲0.34%,報1.770美元/百萬英熱單位,告別週四回落刷新的3月28日以來低位,在上週反彈後本週累跌0.84%。

倫銅反彈至近兩年高位,倫錫一週漲12% 黃金連創盤中歷史新高 後一度較高位回落4%

倫敦基本金屬期貨週五大多上漲。倫鋅漲超2.5%,連漲五日,四日創去年4月以來新高。週四回落的倫錫漲逾2%,和連跌兩日的倫銅均反彈至2022年6月以來高位。兩連跌的倫鋁反彈至去年2月以來高位。週四回落的倫鉛刷新週三所創的1月末以來新高。而倫鎳連跌兩日,繼續跌離連漲八日所創的四周來高位。

本週這些金屬多數繼續累漲,領漲的倫錫漲逾12%,倫鋅漲超7%,倫銅漲超1%,均連漲兩週,倫鋁漲近2%,連漲五週,倫鉛漲超2%,連漲三週,而上週反彈超6%的倫鎳微幅累跌。

週五美股早盤,紐約黃金期貨曾接近2449美元至2448.8美元,日內漲約3.2%,現貨黃金曾漲至2431美元上方,日內漲近2.5%,均連續第二日創盤中歷史新高,後持續回落,美股午盤均轉跌。

期金轉跌前已收盤,COMEX 6月黃金期貨收漲0.06%,報2374.1美元/盎司,連續兩日、本週第三日創收盤最高紀錄,本週累漲1.23%,連漲三週,巴以衝突爆發以來27周內第19周累漲,漲幅遠不及漲近4.8%的上週,上週創去年10月巴以衝突升級當週以來最大周漲幅。

收盤後美股午盤刷新日低時,期金曾跌至2350.6美元,日內跌逾0.9%,現貨黃金跌至2334美元下方,日內跌逾1.6%,均較日內高位跌去約4%。美股收盤時,現貨黃金處於2340美元上方,日內跌逾1.2%,仍連漲四周。

![現貨黃金盤中創歷史新高後一度較高位回落4%]() 現貨黃金盤中創歷史新高後一度較高位回落4%

現貨黃金盤中創歷史新高後一度較高位回落4%編輯/tolk