Benign Growth For UFP Industries, Inc. (NASDAQ:UFPI) Underpins Its Share Price

Benign Growth For UFP Industries, Inc. (NASDAQ:UFPI) Underpins Its Share Price

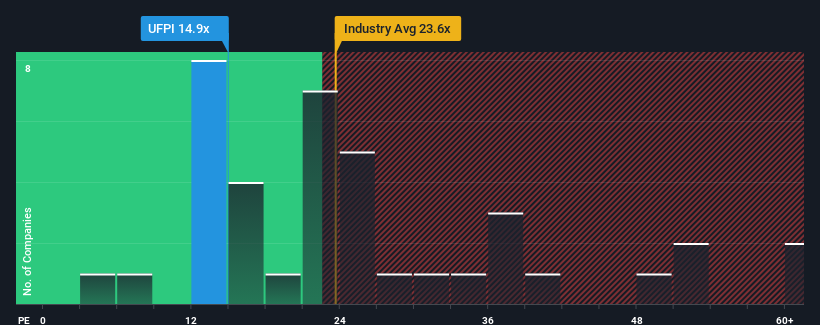

UFP Industries, Inc.'s (NASDAQ:UFPI) price-to-earnings (or "P/E") ratio of 14.9x might make it look like a buy right now compared to the market in the United States, where around half of the companies have P/E ratios above 18x and even P/E's above 33x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/E.

Recent times haven't been advantageous for UFP Industries as its earnings have been falling quicker than most other companies. The P/E is probably low because investors think this poor earnings performance isn't going to improve at all. If you still like the company, you'd want its earnings trajectory to turn around before making any decisions. If not, then existing shareholders will probably struggle to get excited about the future direction of the share price.

How Is UFP Industries' Growth Trending?

The only time you'd be truly comfortable seeing a P/E as low as UFP Industries' is when the company's growth is on track to lag the market.

Retrospectively, the last year delivered a frustrating 26% decrease to the company's bottom line. Still, the latest three year period has seen an excellent 99% overall rise in EPS, in spite of its unsatisfying short-term performance. Accordingly, while they would have preferred to keep the run going, shareholders would probably welcome the medium-term rates of earnings growth.

Turning to the outlook, the next year should bring diminished returns, with earnings decreasing 6.1% as estimated by the six analysts watching the company. Meanwhile, the broader market is forecast to expand by 11%, which paints a poor picture.

With this information, we are not surprised that UFP Industries is trading at a P/E lower than the market. However, shrinking earnings are unlikely to lead to a stable P/E over the longer term. Even just maintaining these prices could be difficult to achieve as the weak outlook is weighing down the shares.

The Bottom Line On UFP Industries' P/E

Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that UFP Industries maintains its low P/E on the weakness of its forecast for sliding earnings, as expected. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

Before you take the next step, you should know about the 1 warning sign for UFP Industries that we have uncovered.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

UFP Industries, Inc. 's(納斯達克股票代碼:UFPI)市盈率(或 “市盈率”)爲14.9倍,與美國市場相比,目前可能看起來像買入。在美國,約有一半公司的市盈率高於18倍,甚至市盈率超過33倍也很常見。儘管如此,我們需要更深入地挖掘以確定降低市盈率是否有合理的基礎。

最近對UFP Industries來說並不是有利的,因爲其收益的下降速度比大多數其他公司快。市盈率可能很低,因爲投資者認爲這種糟糕的收益表現根本不會改善。如果你仍然喜歡這家公司,那麼在做出任何決定之前,你會希望其盈利軌跡得到扭轉。如果不是,那麼現有股東可能很難對股價的未來走向感到興奮。

UFP行業的增長趨勢如何?

只有當公司的增長有望落後於市場時,你才能真正放心地看到市盈率低至UFP Industries的水平。

回顧過去,去年的公司利潤下降了26%,令人沮喪。儘管如此,儘管短期表現不令人滿意,但最近三年的每股收益總體增長了99%。因此,儘管股東們本來希望保持盈利,但他們可能會對中期收益增長率表示歡迎。

談到前景,明年的回報應該會減少,根據關注該公司的六位分析師的估計,收益將下降6.1%。同時,預計整個市場將增長11%,這描繪了一幅糟糕的畫面。

有了這些信息,UFP Industries的市盈率低於市場也就不足爲奇了。但是,從長遠來看,收益萎縮不太可能帶來穩定的市盈率。由於疲軟的前景壓低了股價,即使僅僅維持這些價格也可能難以實現。

UFP Industries 市盈率的底線

通常,在做出投資決策時,我們會謹慎行事,不要過多地閱讀市盈率,儘管這可以充分揭示其他市場參與者對公司的看法。

我們已經確定,UFP Industries維持低市盈率,原因是其對收益下滑的預測不如預期。在現階段,投資者認爲,收益改善的可能性不足以證明更高的市盈率是合理的。除非這些條件有所改善,否則它們將繼續構成股價在這些水平附近的障礙。

在採取下一步行動之前,您應該了解我們發現的UFP Industries的1個警告信號。

如果你對市盈率感興趣,你可能希望看到這批盈利增長強勁、市盈率低的免費公司。

對這篇文章有反饋嗎?對內容感到擔憂?直接聯繫我們。 或者,給編輯團隊 (at) simplywallst.com 發送電子郵件。

Simply Wall St的這篇文章本質上是籠統的。我們僅使用公正的方法根據歷史數據和分析師的預測提供評論,我們的文章無意作爲財務建議。它不構成買入或賣出任何股票的建議,也沒有考慮到您的目標或財務狀況。我們的目標是爲您提供由基本數據驅動的長期重點分析。請注意,我們的分析可能不考慮最新的價格敏感型公司公告或定性材料。簡而言之,華爾街沒有持有任何上述股票的頭寸。

譯文內容由第三人軟體翻譯。

風險及免責聲明

- 分享到weixin

- 分享到qq

- 分享到facebook

- 分享到twitter

- 分享到微博

- 粘贴板

使用瀏覽器的分享功能,分享給你的好友吧