Subdued Growth No Barrier To MayAir Technology (China) Co., Ltd.'s (SHSE:688376) Price

Subdued Growth No Barrier To MayAir Technology (China) Co., Ltd.'s (SHSE:688376) Price

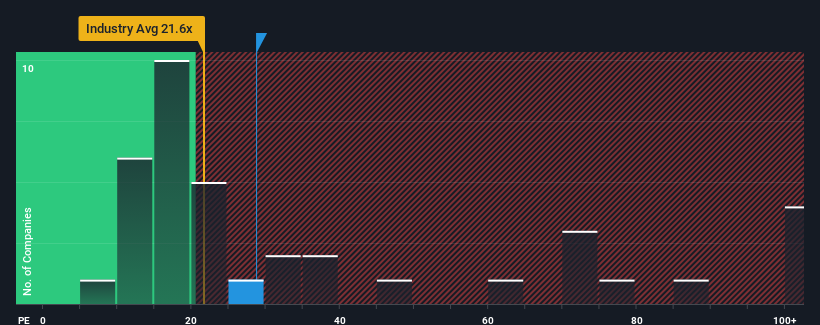

With a median price-to-earnings (or "P/E") ratio of close to 31x in China, you could be forgiven for feeling indifferent about MayAir Technology (China) Co., Ltd.'s (SHSE:688376) P/E ratio of 28.7x. While this might not raise any eyebrows, if the P/E ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

Earnings have risen firmly for MayAir Technology (China) recently, which is pleasing to see. One possibility is that the P/E is moderate because investors think this respectable earnings growth might not be enough to outperform the broader market in the near future. If that doesn't eventuate, then existing shareholders probably aren't too pessimistic about the future direction of the share price.

Is There Some Growth For MayAir Technology (China)?

The only time you'd be comfortable seeing a P/E like MayAir Technology (China)'s is when the company's growth is tracking the market closely.

If we review the last year of earnings growth, the company posted a worthy increase of 8.4%. The latest three year period has also seen an excellent 57% overall rise in EPS, aided somewhat by its short-term performance. So we can start by confirming that the company has done a great job of growing earnings over that time.

Weighing that recent medium-term earnings trajectory against the broader market's one-year forecast for expansion of 39% shows it's noticeably less attractive on an annualised basis.

In light of this, it's curious that MayAir Technology (China)'s P/E sits in line with the majority of other companies. It seems most investors are ignoring the fairly limited recent growth rates and are willing to pay up for exposure to the stock. Maintaining these prices will be difficult to achieve as a continuation of recent earnings trends is likely to weigh down the shares eventually.

The Bottom Line On MayAir Technology (China)'s P/E

While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

Our examination of MayAir Technology (China) revealed its three-year earnings trends aren't impacting its P/E as much as we would have predicted, given they look worse than current market expectations. Right now we are uncomfortable with the P/E as this earnings performance isn't likely to support a more positive sentiment for long. If recent medium-term earnings trends continue, it will place shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

A lot of potential risks can sit within a company's balance sheet. Our free balance sheet analysis for MayAir Technology (China) with six simple checks will allow you to discover any risks that could be an issue.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

中國的市盈率(或 “市盈率”)中位數接近31倍,你對美埃科技(中國)有限公司漠不關心是可以原諒的。”s(上海證券交易所代碼:688376)市盈率爲28.7倍。儘管這可能不會引起任何關注,但如果市盈率不合理,投資者可能會錯過潛在的機會或無視迫在眉睫的失望。

最近,美埃科技(中國)的收益穩步增長,這令人高興。一種可能性是市盈率適中,因爲投資者認爲這種可觀的收益增長可能不足以在不久的將來跑贏大盤。如果最終沒有發生這種情況,那麼現有股東對股價的未來走向可能不會太悲觀。

美埃科技(中國)有增長嗎?

只有當公司的增長密切關注市場時,你才能放心地看到像美埃科技(中國)這樣的市盈率。

如果我們回顧一下去年的收益增長,該公司公佈了8.4%的可觀增長。在最近三年中,每股收益總體增長了57%,這在一定程度上得益於其短期表現。因此,我們可以首先確認該公司在這段時間內在增加收益方面做得很好。

將最近的中期收益軌跡與整個市場對39%的擴張預測進行權衡,可以看出,按年計算,其吸引力明顯降低。

有鑑於此,奇怪的是,美埃科技(中國)的市盈率與其他大多數公司持平。看來大多數投資者都無視近期相當有限的增長率,願意爲股票敞口付出代價。維持這些價格將很難實現,因爲近期收益趨勢的延續最終可能會壓低股價。

美埃科技(中國)市盈率的底線

雖然市盈率不應該是決定你是否買入股票的決定性因素,但它是衡量收益預期的有力晴雨表。

我們對美埃科技(中國)的審查顯示,其三年收益趨勢對市盈率的影響沒有我們預期的那麼大,因爲這些趨勢看起來比當前的市場預期還要糟糕。目前,我們對市盈率感到不舒服,因爲這種收益表現不太可能長期支撐更積極的情緒。如果最近的中期收益趨勢持續下去,將使股東的投資面臨風險,潛在投資者面臨支付不必要的溢價的危險。

公司的資產負債表中可能存在許多潛在風險。我們對MayAir Technology(中國)的免費資產負債表分析包括六張簡單的檢查,將使您發現任何可能存在問題的風險。

重要的是要確保你尋找一家優秀的公司,而不僅僅是你遇到的第一個想法。因此,來看看這份免費名單,列出了最近收益增長強勁(市盈率低)的有趣公司。

對這篇文章有反饋嗎?對內容感到擔憂?直接聯繫我們。 或者,給編輯團隊 (at) simplywallst.com 發送電子郵件。

Simply Wall St的這篇文章本質上是籠統的。我們僅使用公正的方法根據歷史數據和分析師的預測提供評論,我們的文章無意作爲財務建議。它不構成買入或賣出任何股票的建議,也沒有考慮到您的目標或財務狀況。我們的目標是爲您提供由基本數據驅動的長期重點分析。請注意,我們的分析可能不考慮最新的價格敏感型公司公告或定性材料。簡而言之,華爾街沒有持有任何上述股票的頭寸。

譯文內容由第三人軟體翻譯。

風險及免責聲明

- 分享到weixin

- 分享到qq

- 分享到facebook

- 分享到twitter

- 分享到微博

- 粘贴板

使用瀏覽器的分享功能,分享給你的好友吧