Turning Point Brands, Inc. (NYSE:TPB) shareholders would be excited to see that the share price has had a great month, posting a 28% gain and recovering from prior weakness. The last 30 days bring the annual gain to a very sharp 40%.

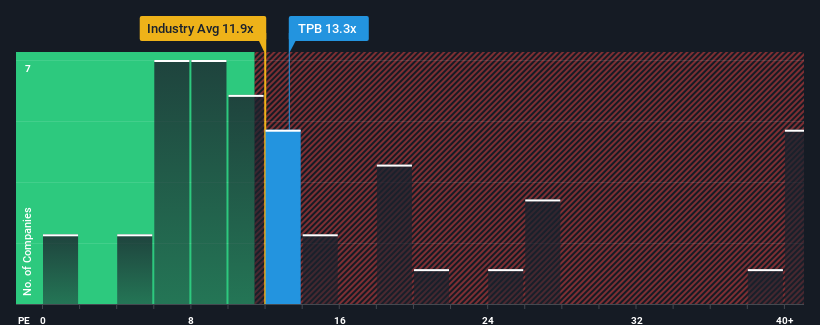

Although its price has surged higher, Turning Point Brands' price-to-earnings (or "P/E") ratio of 13.3x might still make it look like a buy right now compared to the market in the United States, where around half of the companies have P/E ratios above 17x and even P/E's above 32x are quite common. However, the P/E might be low for a reason and it requires further investigation to determine if it's justified.

With its earnings growth in positive territory compared to the declining earnings of most other companies, Turning Point Brands has been doing quite well of late. It might be that many expect the strong earnings performance to degrade substantially, possibly more than the market, which has repressed the P/E. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

NYSE:TPB Price to Earnings Ratio vs Industry March 24th 2024 If you'd like to see what analysts are forecasting going forward, you should check out our free report on Turning Point Brands.

Does Growth Match The Low P/E?

The only time you'd be truly comfortable seeing a P/E as low as Turning Point Brands' is when the company's growth is on track to lag the market.

If we review the last year of earnings growth, the company posted a terrific increase of 236%. EPS has also lifted 11% in aggregate from three years ago, mostly thanks to the last 12 months of growth. Accordingly, shareholders would have probably been satisfied with the medium-term rates of earnings growth.

Shifting to the future, estimates from the two analysts covering the company suggest earnings should grow by 23% over the next year. Meanwhile, the rest of the market is forecast to only expand by 11%, which is noticeably less attractive.

In light of this, it's peculiar that Turning Point Brands' P/E sits below the majority of other companies. Apparently some shareholders are doubtful of the forecasts and have been accepting significantly lower selling prices.

The Bottom Line On Turning Point Brands' P/E

The latest share price surge wasn't enough to lift Turning Point Brands' P/E close to the market median. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We've established that Turning Point Brands currently trades on a much lower than expected P/E since its forecast growth is higher than the wider market. When we see a strong earnings outlook with faster-than-market growth, we assume potential risks are what might be placing significant pressure on the P/E ratio. It appears many are indeed anticipating earnings instability, because these conditions should normally provide a boost to the share price.

You should always think about risks. Case in point, we've spotted 1 warning sign for Turning Point Brands you should be aware of.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Turning Point Brands, Inc.(紐約證券交易所代碼:TPB)的股東們會很高興看到股價經歷了一個不錯的月份,漲幅爲28%,並從先前的疲軟中恢復過來。在過去的30天裏,年增長率達到了非常大幅的40%。

儘管其價格飆升,但與美國市場相比,Turning Point Brands的市盈率(或 “市盈率”)爲13.3倍,目前仍可能看起來像買入。在美國,約有一半公司的市盈率超過17倍,甚至市盈率超過32倍也很常見。但是,市盈率之低可能是有原因的,需要進一步調查以確定其是否合理。

與大多數其他公司的收益下降相比,Turning Point Brands的收益增長處於正值區間,最近表現良好。許多人可能預計,強勁的盈利表現將大幅下降,可能超過抑制市盈率的市場。否則,現有股東有理由對股價的未來走向持相當樂觀的態度。

紐約證券交易所:TPB對比行業的市盈率 2024年3月24日 如果你想了解分析師對未來的預測,你應該查看我們關於Turning Point Brands的免費報告。

增長與低市盈率相匹配嗎?

只有當公司的增長有望落後於市場時,你才能真正放心地看到市盈率低至Turning Point Brands的水平。