Those holding Touchstone International Medical Science Co., Ltd. (SHSE:688013) shares would be relieved that the share price has rebounded 25% in the last thirty days, but it needs to keep going to repair the recent damage it has caused to investor portfolios. Unfortunately, the gains of the last month did little to right the losses of the last year with the stock still down 23% over that time.

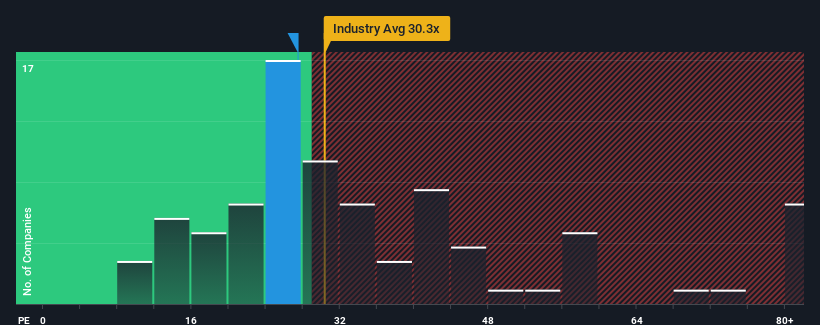

In spite of the firm bounce in price, Touchstone International Medical Science's price-to-earnings (or "P/E") ratio of 27.4x might still make it look like a buy right now compared to the market in China, where around half of the companies have P/E ratios above 32x and even P/E's above 58x are quite common. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

The earnings growth achieved at Touchstone International Medical Science over the last year would be more than acceptable for most companies. One possibility is that the P/E is low because investors think this respectable earnings growth might actually underperform the broader market in the near future. If that doesn't eventuate, then existing shareholders have reason to be optimistic about the future direction of the share price.

SHSE:688013 Price to Earnings Ratio vs Industry March 18th 2024 Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Touchstone International Medical Science will help you shine a light on its historical performance.

What Are Growth Metrics Telling Us About The Low P/E?

The only time you'd be truly comfortable seeing a P/E as low as Touchstone International Medical Science's is when the company's growth is on track to lag the market.

Retrospectively, the last year delivered an exceptional 20% gain to the company's bottom line. As a result, it also grew EPS by 23% in total over the last three years. So we can start by confirming that the company has actually done a good job of growing earnings over that time.

Comparing that to the market, which is predicted to deliver 40% growth in the next 12 months, the company's momentum is weaker based on recent medium-term annualised earnings results.

With this information, we can see why Touchstone International Medical Science is trading at a P/E lower than the market. Apparently many shareholders weren't comfortable holding on to something they believe will continue to trail the bourse.

The Bottom Line On Touchstone International Medical Science's P/E

Despite Touchstone International Medical Science's shares building up a head of steam, its P/E still lags most other companies. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

We've established that Touchstone International Medical Science maintains its low P/E on the weakness of its recent three-year growth being lower than the wider market forecast, as expected. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. Unless the recent medium-term conditions improve, they will continue to form a barrier for the share price around these levels.

There are also other vital risk factors to consider before investing and we've discovered 1 warning sign for Touchstone International Medical Science that you should be aware of.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

儘管股價出現反彈,但Touchstone International Medical Science27.4倍的市盈率(或 “市盈率”)與中國市場相比,目前仍可能看起來像買入,中國約有一半公司的市盈率超過32倍,甚至市盈率超過58倍也很常見。但是,僅按面值計算市盈率是不明智的,因爲可以解釋爲什麼市盈率有限。

Touchstone International Medical Science去年實現的收益增長對於大多數公司來說是完全可以接受的。一種可能性是市盈率很低,因爲投資者認爲這種可觀的收益增長在不久的將來實際上可能低於整個市場。如果最終沒有發生這種情況,那麼現有股東就有理由對股價的未來走向持樂觀態度。

儘管Touchstone International Medical Science的股價蓬勃發展,但其市盈率仍然落後於大多數其他公司。儘管市盈率不應該成爲決定你是否買入股票的決定性因素,但它是衡量收益預期的有力晴雨表。

我們已經確定,Touchstone International Medical Science維持了較低的市盈率,原因是其最近三年的增長疲軟,低於更廣泛的市場預測,正如預期的那樣。目前,股東們正在接受低市盈率,因爲他們承認未來的收益可能不會帶來任何驚喜。除非最近的中期狀況有所改善,否則它們將繼續構成股價在這些水平附近的障礙。

在投資之前,還有其他重要的風險因素需要考慮,我們已經發現了Touchstone International Medical Science的一個警告信號,你應該注意這一點。