Investors Shouldn't Be Too Comfortable With Broadwind's (NASDAQ:BWEN) Earnings

Investors Shouldn't Be Too Comfortable With Broadwind's (NASDAQ:BWEN) Earnings

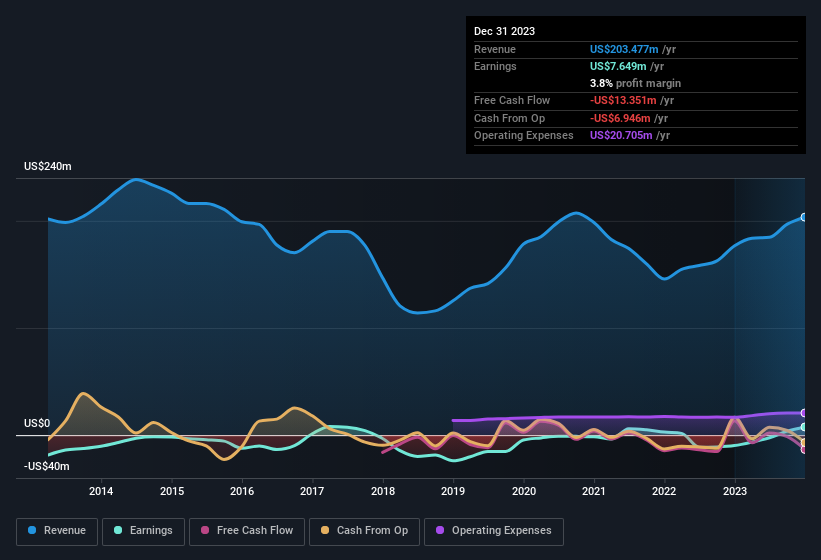

Despite posting some strong earnings, the market for Broadwind, Inc.'s (NASDAQ:BWEN) stock hasn't moved much. Our analysis suggests that this might be because shareholders have noticed some concerning underlying factors.

尽管公布了一些强劲的收益,但Broadwind, Inc.的市场s(纳斯达克股票代码:BWEN)的股票涨幅不大。我们的分析表明,这可能是因为股东已经注意到了一些相关的潜在因素。

Examining Cashflow Against Broadwind's Earnings

根据Broadwind的收益研究现金流

As finance nerds would already know, the accrual ratio from cashflow is a key measure for assessing how well a company's free cash flow (FCF) matches its profit. To get the accrual ratio we first subtract FCF from profit for a period, and then divide that number by the average operating assets for the period. The ratio shows us how much a company's profit exceeds its FCF.

正如金融迷已经知道的那样,现金流的应计比率是评估公司自由现金流(FCF)与利润匹配程度的关键指标。为了获得应计比率,我们首先从一段时期的利润中减去FCF,然后将该数字除以该期间的平均运营资产。该比率向我们显示了公司的利润超过其FCF的程度。

That means a negative accrual ratio is a good thing, because it shows that the company is bringing in more free cash flow than its profit would suggest. While having an accrual ratio above zero is of little concern, we do think it's worth noting when a company has a relatively high accrual ratio. That's because some academic studies have suggested that high accruals ratios tend to lead to lower profit or less profit growth.

这意味着负应计比率是一件好事,因为它表明该公司带来的自由现金流超出了其利润所暗示的范围。尽管应计比率高于零并不令人担忧,但我们确实认为,当公司的应计比率相对较高时,值得注意。那是因为一些学术研究表明,高应计比率往往会导致利润下降或利润增长放缓。

Over the twelve months to December 2023, Broadwind recorded an accrual ratio of 0.39. Statistically speaking, that's a real negative for future earnings. To wit, the company did not generate one whit of free cashflow in that time. Over the last year it actually had negative free cash flow of US$13m, in contrast to the aforementioned profit of US$7.65m. We saw that FCF was US$14m a year ago though, so Broadwind has at least been able to generate positive FCF in the past. The good news for shareholders is that Broadwind's accrual ratio was much better last year, so this year's poor reading might simply be a case of a short term mismatch between profit and FCF. As a result, some shareholders may be looking for stronger cash conversion in the current year.

在截至2023年12月的十二个月中,Broadwind记录的应计比率为0.39。从统计学上讲,这对未来的收益来说确实是负面的。换句话说,该公司在那段时间内没有产生一点自由现金流。在过去的一年里,它实际上有 负面的 自由现金流为1300万美元,而上述利润为765万美元。但是,我们看到一年前的FCF为1400万美元,因此Broadwind过去至少能够产生正的FCF。对股东来说,好消息是,Broadwind去年的应计比率要好得多,因此今年的糟糕数据可能只是利润与FCF之间短期不匹配的情况。因此,一些股东可能希望在本年度实现更强的现金转换。

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

这可能会让你想知道分析师对未来盈利能力的预测。幸运的是,您可以单击此处查看根据他们的估计描绘未来盈利能力的交互式图表。

Our Take On Broadwind's Profit Performance

我们对Broadwind盈利表现的看法

As we have made quite clear, we're a bit worried that Broadwind didn't back up the last year's profit with free cashflow. As a result, we think it may well be the case that Broadwind's underlying earnings power is lower than its statutory profit. The good news is that it earned a profit in the last twelve months, despite its previous loss. The goal of this article has been to assess how well we can rely on the statutory earnings to reflect the company's potential, but there is plenty more to consider. So if you'd like to dive deeper into this stock, it's crucial to consider any risks it's facing. Be aware that Broadwind is showing 4 warning signs in our investment analysis and 2 of those are significant...

正如我们已经明确指出的那样,我们有点担心Broadwind没有用自由现金流来支持去年的利润。因此,我们认为Broadwind的潜在盈利能力很可能低于其法定利润。好消息是,尽管之前出现亏损,但它在过去十二个月中还是实现了盈利。本文的目标是评估我们在多大程度上可以依靠法定收益来反映公司的潜力,但还有很多需要考虑的地方。因此,如果你想更深入地研究这只股票,那么考虑它面临的任何风险至关重要。请注意,Broadwind在我们的投资分析中显示了4个警告信号,其中2个信号很重要...

This note has only looked at a single factor that sheds light on the nature of Broadwind's profit. But there are plenty of other ways to inform your opinion of a company. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

这份报告只研究了揭示Broadwind利润性质的单一因素。但是,还有很多其他方法可以让你对公司的看法。例如,许多人认为高股本回报率是有利的商业经济的标志,而另一些人则喜欢 “关注资金”,寻找内部人士正在买入的股票。因此,你可能希望看到这份免费收藏的拥有高股本回报率的公司,或者这份内部人士正在购买的股票清单。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

对这篇文章有反馈吗?对内容感到担忧?直接联系我们。 或者,给编辑团队 (at) simplywallst.com 发送电子邮件。

Simply Wall St的这篇文章本质上是笼统的。我们仅使用公正的方法根据历史数据和分析师的预测提供评论,我们的文章无意作为财务建议。它不构成买入或卖出任何股票的建议,也没有考虑到您的目标或财务状况。我们的目标是为您提供由基本数据驱动的长期重点分析。请注意,我们的分析可能不考虑最新的价格敏感型公司公告或定性材料。简而言之,华尔街没有持有任何上述股票的头寸。

译文内容由第三方软件翻译。