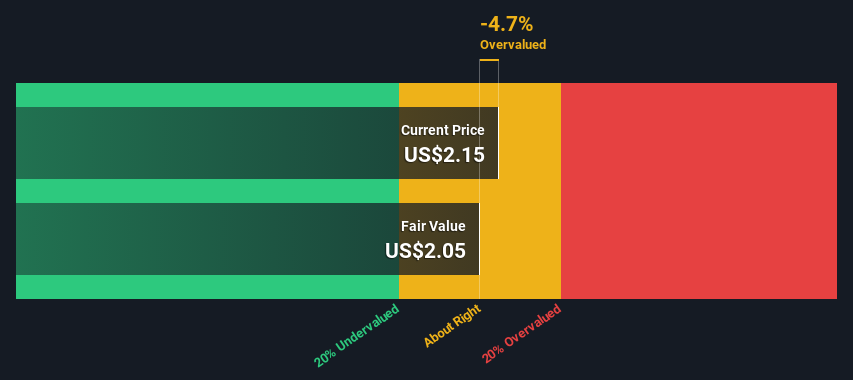

DFI Retail Group Holdings' estimated fair value is US$2.05 based on Dividend Discount Model

DFI Retail Group Holdings' US$2.15 share price indicates it is trading at similar levels as its fair value estimate

The US$3.13 analyst price target for D01 is 52% more than our estimate of fair value

How far off is DFI Retail Group Holdings Limited (SGX:D01) from its intrinsic value? Using the most recent financial data, we'll take a look at whether the stock is fairly priced by taking the forecast future cash flows of the company and discounting them back to today's value. The Discounted Cash Flow (DCF) model is the tool we will apply to do this. It may sound complicated, but actually it is quite simple!

Remember though, that there are many ways to estimate a company's value, and a DCF is just one method. If you want to learn more about discounted cash flow, the rationale behind this calculation can be read in detail in the Simply Wall St analysis model.

Step By Step Through The Calculation

As DFI Retail Group Holdings operates in the consumer retailing sector, we need to calculate the intrinsic value slightly differently. In this approach dividends per share (DPS) are used, as free cash flow is difficult to estimate and often not reported by analysts. Unless a company pays out the majority of its FCF as a dividend, this method will typically underestimate the value of the stock. The 'Gordon Growth Model' is used, which simply assumes that dividend payments will continue to increase at a sustainable growth rate forever. For a number of reasons a very conservative growth rate is used that cannot exceed that of a company's Gross Domestic Product (GDP). In this case we used the 5-year average of the 10-year government bond yield (2.1%). The expected dividend per share is then discounted to today's value at a cost of equity of 6.4%. Relative to the current share price of US$2.2, the company appears around fair value at the time of writing. Remember though, that this is just an approximate valuation, and like any complex formula - garbage in, garbage out.

Value Per Share = Expected Dividend Per Share / (Discount Rate - Perpetual Growth Rate)

= US$0.1 / (6.4% – 2.1%)

= US$2.1

SGX:D01 Discounted Cash Flow February 22nd 2024

The Assumptions

Now the most important inputs to a discounted cash flow are the discount rate, and of course, the actual cash flows. If you don't agree with these result, have a go at the calculation yourself and play with the assumptions. The DCF also does not consider the possible cyclicality of an industry, or a company's future capital requirements, so it does not give a full picture of a company's potential performance. Given that we are looking at DFI Retail Group Holdings as potential shareholders, the cost of equity is used as the discount rate, rather than the cost of capital (or weighted average cost of capital, WACC) which accounts for debt. In this calculation we've used 6.4%, which is based on a levered beta of 0.800. Beta is a measure of a stock's volatility, compared to the market as a whole. We get our beta from the industry average beta of globally comparable companies, with an imposed limit between 0.8 and 2.0, which is a reasonable range for a stable business.

SWOT Analysis for DFI Retail Group Holdings

Strength

Debt is well covered by cash flow.

Balance sheet summary for D01.

Weakness

Interest payments on debt are not well covered.

Dividend is low compared to the top 25% of dividend payers in the Consumer Retailing market.

Opportunity

Expected to breakeven next year.

Has sufficient cash runway for more than 3 years based on current free cash flows.

Good value based on P/S ratio compared to estimated Fair P/S ratio.

Threat

Paying a dividend but company is unprofitable.

See D01's dividend history.

Moving On:

Whilst important, the DCF calculation is only one of many factors that you need to assess for a company. It's not possible to obtain a foolproof valuation with a DCF model. Rather it should be seen as a guide to "what assumptions need to be true for this stock to be under/overvalued?" For instance, if the terminal value growth rate is adjusted slightly, it can dramatically alter the overall result. For DFI Retail Group Holdings, we've put together three pertinent aspects you should further research:

Risks: Be aware that DFI Retail Group Holdings is showing 1 warning sign in our investment analysis , you should know about...

Management:Have insiders been ramping up their shares to take advantage of the market's sentiment for D01's future outlook? Check out our management and board analysis with insights on CEO compensation and governance factors.

Other Solid Businesses: Low debt, high returns on equity and good past performance are fundamental to a strong business. Why not explore our interactive list of stocks with solid business fundamentals to see if there are other companies you may not have considered!

PS. Simply Wall St updates its DCF calculation for every Singaporean stock every day, so if you want to find the intrinsic value of any other stock just search here.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

关键见解

根据股息折扣模型,DFI Retail Group Holdings的估计公允价值为2.05美元

DFI Retail Group Holdings的2.15美元股价表明其交易价格与其公允价值估计相似

现在,贴现现金流的最重要输入是贴现率,当然还有实际现金流。如果你不同意这些结果,那就自己计算一下,试一试假设。DCF也没有考虑一个行业可能的周期性,也没有考虑公司未来的资本需求,因此它没有全面反映公司的潜在表现。鉴于我们将DFI Retail Group Holdings视为潜在股东,因此使用股本成本作为贴现率,而不是构成债务的资本成本(或加权平均资本成本,WACC)。在此计算中,我们使用了6.4%,这是基于0.800的杠杆测试版。Beta是衡量股票与整个市场相比波动性的指标。我们的测试版来自全球可比公司的行业平均贝塔值,设定在0.8到2.0之间,这是一个稳定的业务的合理范围。