To the annoyance of some shareholders, Baijiayun Group Ltd (NASDAQ:RTC) shares are down a considerable 59% in the last month, which continues a horrid run for the company. The recent drop completes a disastrous twelve months for shareholders, who are sitting on a 91% loss during that time.

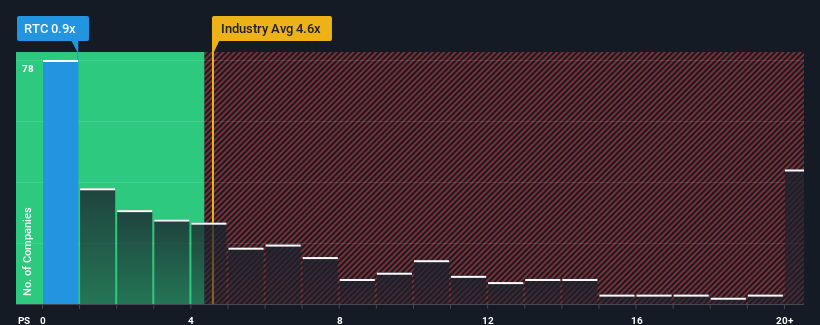

After such a large drop in price, Baijiayun Group may be sending very bullish signals at the moment with its price-to-sales (or "P/S") ratio of 0.9x, since almost half of all companies in the Software industry in the United States have P/S ratios greater than 4.6x and even P/S higher than 11x are not unusual. However, the P/S might be quite low for a reason and it requires further investigation to determine if it's justified.

NasdaqGM:RTC Price to Sales Ratio vs Industry February 1st 2024

How Baijiayun Group Has Been Performing

Revenue has risen firmly for Baijiayun Group recently, which is pleasing to see. It might be that many expect the respectable revenue performance to degrade substantially, which has repressed the P/S. If that doesn't eventuate, then existing shareholders have reason to be optimistic about the future direction of the share price.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Baijiayun Group's earnings, revenue and cash flow.

What Are Revenue Growth Metrics Telling Us About The Low P/S?

Baijiayun Group's P/S ratio would be typical for a company that's expected to deliver very poor growth or even falling revenue, and importantly, perform much worse than the industry.

Taking a look back first, we see that the company grew revenue by an impressive 20% last year. The strong recent performance means it was also able to grow revenue by 252% in total over the last three years. So we can start by confirming that the company has done a great job of growing revenue over that time.

Comparing that recent medium-term revenue trajectory with the industry's one-year growth forecast of 15% shows it's noticeably more attractive.

With this information, we find it odd that Baijiayun Group is trading at a P/S lower than the industry. It looks like most investors are not convinced the company can maintain its recent growth rates.

The Key Takeaway

Having almost fallen off a cliff, Baijiayun Group's share price has pulled its P/S way down as well. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

Our examination of Baijiayun Group revealed its three-year revenue trends aren't boosting its P/S anywhere near as much as we would have predicted, given they look better than current industry expectations. When we see robust revenue growth that outpaces the industry, we presume that there are notable underlying risks to the company's future performance, which is exerting downward pressure on the P/S ratio. While recent revenue trends over the past medium-term suggest that the risk of a price decline is low, investors appear to perceive a likelihood of revenue fluctuations in the future.

We don't want to rain on the parade too much, but we did also find 4 warning signs for Baijiayun Group (2 are potentially serious!) that you need to be mindful of.

If you're unsure about the strength of Baijiayun Group's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

令一些股東煩惱的是,百佳雲集團有限公司(納斯達克股票代碼:RTC)的股價在上個月下跌了59%,這延續了該公司的糟糕表現。對於股東來說,最近的下跌結束了災難性的十二個月,在此期間,股東虧損了91%。

在價格大幅下跌之後,百佳雲集團目前可能發出了非常看漲的信號,其市銷率(或 “市盈率”)爲0.9倍,因爲美國軟件行業幾乎有一半公司的市盈率大於4.6倍,甚至市盈率高於11倍也並不罕見。但是,市銷率可能很低是有原因的,需要進一步調查以確定其是否合理。

納斯達克通用汽車公司:RTC 與行業的股價銷售比率 2024 年 2 月 1 日

百佳雲集團的表現如何

最近,百佳雲集團的收入穩步增長,這令人高興。許多人可能預計,可觀的收入表現將大幅下降,這抑制了市銷率。如果最終沒有出現這種情況,那麼現有股東就有理由對股價的未來走向持樂觀態度。

我們沒有分析師的預測,但您可以查看我們關於百佳雲集團收益、收入和現金流的免費報告,了解最近的趨勢如何爲公司的未來做好準備。

關於低市盈率,收入增長指標告訴我們什麼?

對於一家預計增長非常糟糕甚至收入下降的公司,百佳雲集團的市銷率是典型的,而且重要的是,其表現要比行業差得多。

首先回顧一下,我們發現該公司去年的收入增長了令人印象深刻的20%。最近的強勁表現意味着它在過去三年中總收入增長了252%。因此,我們可以首先確認該公司在這段時間內在增加收入方面做得很好。

將最近的中期收入軌跡與該行業15%的年度增長預測進行比較,可以看出該行業明顯更具吸引力。

有了這些信息,我們感到奇怪的是,百佳雲集團的市銷售率低於該行業。看來大多數投資者不相信該公司能夠維持其最近的增長率。

關鍵要點

在幾乎跌下懸崖之後,百佳雲集團的股價也大幅下調了市銷率。僅使用市銷率來確定是否應該出售股票是不明智的,但它可以作爲公司未來前景的實用指南。

我們對百佳雲集團的調查顯示,其三年收入趨勢並沒有像我們預期的那樣提高市銷率,因爲這些趨勢看起來好於當前的行業預期。當我們看到強勁的收入增長超過行業時,我們認爲公司的未來業績存在明顯的潛在風險,這給市銷率帶來了下行壓力。儘管過去中期最近的收入趨勢表明價格下跌的風險很低,但投資者似乎認爲未來收入可能會出現波動。

我們不想在遊行隊伍中下太多雨,但我們也確實發現了百佳雲集團的4個警告標誌(2個可能很嚴重!)這是你需要注意的。

如果您不確定百佳雲集團的業務實力,爲什麼不瀏覽我們的互動股票清單,這些股票具有穩健的業務基本面,您可能錯過的其他一些公司。

對這篇文章有反饋嗎?對內容感到擔憂嗎?請直接聯繫我們。或者,也可以發送電子郵件至編輯團隊 (at) simplywallst.com。

Simply Wall St的這篇文章本質上是籠統的。我們僅使用公正的方法根據歷史數據和分析師的預測提供評論,我們的文章無意作爲財務建議。它不構成買入或賣出任何股票的建議,也沒有考慮到您的目標或財務狀況。我們的目標是爲您提供由基本數據驅動的長期重點分析。請注意,我們的分析可能不考慮最新的價格敏感型公司公告或定性材料。簡而言之,華爾街沒有持有任何上述股票的頭寸。