Some Confidence Is Lacking In Gan & Lee Pharmaceuticals.'s (SHSE:603087) P/S

Some Confidence Is Lacking In Gan & Lee Pharmaceuticals.'s (SHSE:603087) P/S

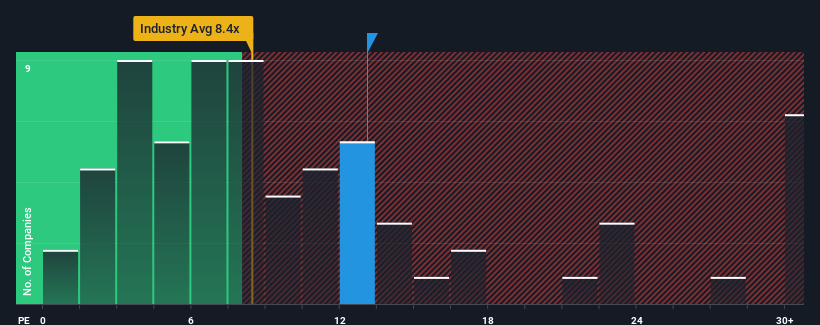

When you see that almost half of the companies in the Biotechs industry in China have price-to-sales ratios (or "P/S") below 8.4x, Gan & Lee Pharmaceuticals. (SHSE:603087) looks to be giving off strong sell signals with its 13.1x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/S.

Check out our latest analysis for Gan & Lee Pharmaceuticals

What Does Gan & Lee Pharmaceuticals' P/S Mean For Shareholders?

With revenue growth that's inferior to most other companies of late, Gan & Lee Pharmaceuticals has been relatively sluggish. One possibility is that the P/S ratio is high because investors think this lacklustre revenue performance will improve markedly. However, if this isn't the case, investors might get caught out paying too much for the stock.

Want the full picture on analyst estimates for the company? Then our free report on Gan & Lee Pharmaceuticals will help you uncover what's on the horizon.How Is Gan & Lee Pharmaceuticals' Revenue Growth Trending?

In order to justify its P/S ratio, Gan & Lee Pharmaceuticals would need to produce outstanding growth that's well in excess of the industry.

If we review the last year of revenue, the company posted a result that saw barely any deviation from a year ago. The lack of growth did nothing to help the company's aggregate three-year performance, which is an unsavory 26% drop in revenue. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Turning to the outlook, the next year should generate growth of 28% as estimated by the only analyst watching the company. That's shaping up to be materially lower than the 908% growth forecast for the broader industry.

With this in consideration, we believe it doesn't make sense that Gan & Lee Pharmaceuticals' P/S is outpacing its industry peers. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. There's a good chance these shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with the growth outlook.

The Key Takeaway

While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

Despite analysts forecasting some poorer-than-industry revenue growth figures for Gan & Lee Pharmaceuticals, this doesn't appear to be impacting the P/S in the slightest. Right now we aren't comfortable with the high P/S as the predicted future revenues aren't likely to support such positive sentiment for long. At these price levels, investors should remain cautious, particularly if things don't improve.

And what about other risks? Every company has them, and we've spotted 3 warning signs for Gan & Lee Pharmaceuticals (of which 2 make us uncomfortable!) you should know about.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

當你看到中國生物技術行業中將近一半的公司的市售率(或 “市盈率”)低於8.4倍時,甘李製藥。(SHSE: 603087) 的市盈率爲13.1倍,似乎發出了強烈的賣出信號。儘管如此,我們需要進行更深入的挖掘,以確定市盈率大幅上漲是否有合理的基礎。

查看我們對 Gan & Lee Pharmicals 的最新分析

甘李製藥的市盈率對股東意味着什麼?

由於最近收入增長不如大多數其他公司,甘李製藥一直相對緩慢。一種可能性是市盈率很高,因爲投資者認爲這種乏善可陳的收入表現將顯著改善。但是,如果不是這樣,投資者可能會被困爲股票支付過多的費用。

想全面了解分析師對公司的估計?然後,我們關於甘李製藥的免費報告將幫助您發現即將發生的事情。甘李藥業的收入增長趨勢如何?

爲了證明其市盈率是合理的,Gan & Lee Pharmicals需要實現遠遠超過該行業的出色增長。

如果我們回顧一下去年的收入,該公司公佈的業績與去年同期幾乎沒有任何差異。增長乏力無助於該公司的三年總體業績,收入下降了26%,令人不快。因此,可以公平地說,最近的收入增長對公司來說是不可取的。

談到前景,正如唯一關注該公司的分析師所估計,明年將實現28%的增長。這將大大低於整個行業908%的增長預期。

考慮到這一點,我們認爲甘李製藥的市盈率超過行業同行是沒有道理的。看來大多數投資者都希望公司的業務前景出現轉機,但分析師群體對這種情況的發生並不那麼有信心。如果市盈率降至更符合增長前景的水平,這些股東很有可能爲未來的失望做好準備。

關鍵要點

雖然市銷比不應該是決定你是否買入股票的決定性因素,但它是衡量收入預期的有力晴雨表。

儘管分析師預測甘李製藥的收入增長數字將低於行業,但這似乎絲毫沒有影響市盈率。目前,我們對高市盈率不滿意,因爲預測的未來收入不太可能長期支撐這種樂觀情緒。在這些價格水平下,投資者應保持謹慎,尤其是在情況沒有改善的情況下。

那其他風險呢?每家公司都有它們,我們發現了 Gan & Lee Pharmicals 的 3 個警告信號(其中 2 個讓我們感到不舒服!)你應該知道。

重要的是要確保你尋找一家優秀的公司,而不僅僅是你遇到的第一個想法。因此,如果盈利能力的增長與你對一家優秀公司的想法一致,那就來看看這份免費名單吧,列出了最近收益增長強勁(市盈率低)的有趣公司。

對這篇文章有反饋嗎?對內容感到擔憂?直接聯繫我們。 或者,給編輯團隊 (at) simplywallst.com 發送電子郵件。

Simply Wall St的這篇文章本質上是籠統的。我們僅使用公正的方法根據歷史數據和分析師的預測提供評論,我們的文章無意作爲財務建議。它不構成買入或賣出任何股票的建議,也沒有考慮到您的目標或財務狀況。我們的目標是爲您提供由基本數據驅動的長期重點分析。請注意,我們的分析可能不考慮最新的價格敏感型公司公告或定性材料。簡而言之,華爾街沒有持有任何上述股票的頭寸。

譯文內容由第三人軟體翻譯。

風險及免責聲明

- 分享到weixin

- 分享到qq

- 分享到facebook

- 分享到twitter

- 分享到微博

- 粘贴板

使用瀏覽器的分享功能,分享給你的好友吧