GSE Systems, Inc. (NASDAQ:GVP) shareholders would be excited to see that the share price has had a great month, posting a 92% gain and recovering from prior weakness. Unfortunately, the gains of the last month did little to right the losses of the last year with the stock still down 43% over that time.

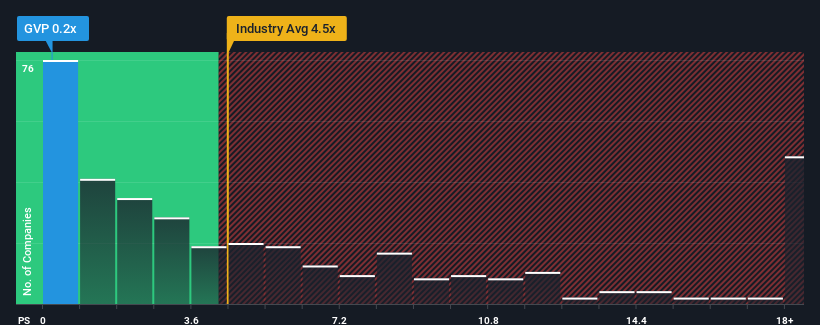

In spite of the firm bounce in price, GSE Systems may still be sending very bullish signals at the moment with its price-to-sales (or "P/S") ratio of 0.2x, since almost half of all companies in the Software industry in the United States have P/S ratios greater than 4.5x and even P/S higher than 10x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/S.

See our latest analysis for GSE Systems

NasdaqCM:GVP Price to Sales Ratio vs Industry November 16th 2023

What Does GSE Systems' Recent Performance Look Like?

GSE Systems could be doing better as its revenue has been going backwards lately while most other companies have been seeing positive revenue growth. It seems that many are expecting the poor revenue performance to persist, which has repressed the P/S ratio. If you still like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on GSE Systems.

What Are Revenue Growth Metrics Telling Us About The Low P/S?

In order to justify its P/S ratio, GSE Systems would need to produce anemic growth that's substantially trailing the industry.

Retrospectively, the last year delivered a frustrating 14% decrease to the company's top line. This means it has also seen a slide in revenue over the longer-term as revenue is down 34% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Shifting to the future, estimates from the sole analyst covering the company suggest revenue should grow by 19% each year over the next three years. Meanwhile, the rest of the industry is forecast to only expand by 16% per annum, which is noticeably less attractive.

With this in consideration, we find it intriguing that GSE Systems' P/S sits behind most of its industry peers. It looks like most investors are not convinced at all that the company can achieve future growth expectations.

What We Can Learn From GSE Systems' P/S?

GSE Systems' recent share price jump still sees fails to bring its P/S alongside the industry median. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

GSE Systems' analyst forecasts revealed that its superior revenue outlook isn't contributing to its P/S anywhere near as much as we would have predicted. When we see strong growth forecasts like this, we can only assume potential risks are what might be placing significant pressure on the P/S ratio. At least price risks look to be very low, but investors seem to think future revenues could see a lot of volatility.

We don't want to rain on the parade too much, but we did also find 5 warning signs for GSE Systems (2 can't be ignored!) that you need to be mindful of.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

GSE Systems, Inc.(納斯達克股票代碼:GVP)的股東們一定會興奮地看到,該公司的股價在本月表現出色,漲幅高達92%,從之前的疲軟狀態中恢復過來。不幸的是,上個月的漲勢並沒有糾正去年的跌勢,同期該股仍下跌了43%。

儘管價格大幅反彈,但GSE Systems目前仍可能發出非常看漲的信號,其市盈率(或 “市盈率”)爲0.2倍,因爲美國軟件行業幾乎有一半的市盈率超過4.5倍,甚至市盈率高於10倍也並不罕見。儘管如此,我們需要更深入地挖掘以確定市盈率大幅下降是否有合理的基礎。

查看我們對 GSE 系統的最新分析

納斯達克CM: GVP 市銷比與行業對比 2023 年 11 月 16 日

GSE Systems 最近的表現是什麼樣子?

GSE Systems可能會做得更好,因爲其收入最近一直在倒退,而大多數其他公司的收入卻出現了正增長。似乎許多人預計糟糕的收入表現將持續下去,這抑制了市盈率。如果你還喜歡這家公司,你會希望情況並非如此,這樣你就有可能在它失寵的時候買入一些股票。

如果你想了解分析師對未來的預測,你應該查看我們關於GSE Systems的免費報告。

關於低市盈率,收入增長指標告訴我們什麼?

爲了證明其市盈率是合理的,GSE Systems需要實現大幅落後於該行業的疲軟增長。

回顧過去,去年該公司的收入下降了14%,令人沮喪。這意味着從長遠來看,它的收入也有所下滑,因爲在過去三年中,總收入下降了34%。因此,可以公平地說,最近的收入增長對公司來說是不可取的。

展望未來,報道該公司的唯一分析師的估計表明,在未來三年中,收入每年將增長19%。同時,預計該行業的其他部門每年僅增長16%,這明顯降低了吸引力。

考慮到這一點,我們發現有趣的是,GSE Systems的市盈率落後於大多數行業同行。看來大多數投資者根本不相信該公司能夠實現未來的增長預期。

我們可以從GSE Systems的P/S中學到什麼?

GSE Systems最近的股價上漲仍未能使其市盈率與行業中位數持平。通常,我們傾向於將價格與銷售比率的使用限制在確定市場對公司整體健康狀況的看法上。

GSE Systems的分析師預測顯示,其優異的收入前景對其市盈率的貢獻不如我們預期的那麼大。當我們看到這樣的強勁增長預測時,我們只能假設潛在風險可能會給市盈率帶來巨大壓力。至少價格風險看起來很低,但投資者似乎認爲未來的收入可能會出現很大的波動。

我們不想在遊行隊伍中下太多雨,但我們也發現了 GSE Systems 的 5 個警告標誌(2 個不容忽視!)你需要注意的。

如果過去盈利增長穩健的公司處於困境,那麼你可能希望看到這些盈利增長強勁、市盈率低的其他公司的免費集合。

對這篇文章有反饋嗎?對內容感到擔憂嗎?請直接聯繫我們。或者,也可以發送電子郵件至編輯團隊 (at) simplywallst.com。

Simply Wall St的這篇文章本質上是籠統的。我們僅使用公正的方法根據歷史數據和分析師的預測提供評論,我們的文章無意作爲財務建議。它不構成買入或賣出任何股票的建議,也沒有考慮到您的目標或財務狀況。我們的目標是爲您提供由基本數據驅動的長期重點分析。請注意,我們的分析可能不考慮最新的價格敏感型公司公告或定性材料。簡而言之,華爾街沒有持有任何上述股票的頭寸。