GRP Limited (SGX:BLU) Shares May Have Slumped 29% But Getting In Cheap Is Still Unlikely

GRP Limited (SGX:BLU) Shares May Have Slumped 29% But Getting In Cheap Is Still Unlikely

GRP Limited (SGX:BLU) shareholders won't be pleased to see that the share price has had a very rough month, dropping 29% and undoing the prior period's positive performance. Looking back over the past twelve months the stock has been a solid performer regardless, with a gain of 17%.

GRP有限公司(新加坡證券交易所股票代碼:BLU)股東不會高興地看到股價經歷了非常艱難的一個月,下跌了29%,抹去了前一季度的積極表現。回顧過去12個月,該股表現穩健,漲幅達17%。

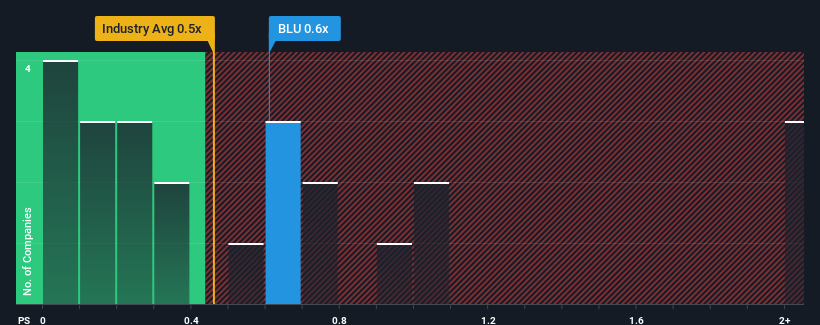

Although its price has dipped substantially, you could still be forgiven for feeling indifferent about GRP's P/S ratio of 0.6x, since the median price-to-sales (or "P/S") ratio for the Electronic industry in Singapore is also close to 0.5x. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

儘管它的價格已經大幅下降,但你仍然可以原諒對GRP的P/S比率0.6倍的無動於衷,因為新加坡電子行業的中位數價格與銷售額(或“P/S”)比率也接近0.5倍。儘管如此,在沒有解釋的情況下簡單地忽視本益比S是不明智的,因為投資者可能會忽視一個獨特的機會或代價高昂的錯誤。

View our latest analysis for GRP

查看我們對GRP的最新分析

What Does GRP's P/S Mean For Shareholders?

GRP的P/S對股東意味著什麼?

With revenue growth that's exceedingly strong of late, GRP has been doing very well. Perhaps the market is expecting future revenue performance to taper off, which has kept the P/S from rising. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's not quite in favour.

最近收入增長異常強勁,GRP的表現一直很好。或許,市場預期未來的營收表現將逐漸減弱,這使得本益比S不再上漲。如果你喜歡這家公司,你會希望情況並非如此,這樣你就可以在它不太受歡迎的時候買入一些股票。

Is There Some Revenue Growth Forecasted For GRP?

GRP是否有一些收入增長預測?

The only time you'd be comfortable seeing a P/S like GRP's is when the company's growth is tracking the industry closely.

看到像GRP這樣的P/S,你唯一會感到舒服的時候是該公司的增長正在密切跟蹤行業的發展。

If we review the last year of revenue growth, the company posted a terrific increase of 35%. The latest three year period has also seen an excellent 37% overall rise in revenue, aided by its short-term performance. So we can start by confirming that the company has done a great job of growing revenue over that time.

如果我們回顧一下去年的收入增長,該公司公佈了35%的驚人增長。在最近三年中,得益於其短期表現,該公司的整體收入也實現了37%的出色增長。因此,我們可以從確認該公司在這段時間內在收入增長方面做得很好開始。

This is in contrast to the rest of the industry, which is expected to grow by 31% over the next year, materially higher than the company's recent medium-term annualised growth rates.

這與其他行業形成鮮明對比,預計明年該行業將增長31%,大大高於該公司最近的中期年化增長率。

In light of this, it's curious that GRP's P/S sits in line with the majority of other companies. Apparently many investors in the company are less bearish than recent times would indicate and aren't willing to let go of their stock right now. Maintaining these prices will be difficult to achieve as a continuation of recent revenue trends is likely to weigh down the shares eventually.

有鑒於此,令人好奇的是,GRP的P/S與大多數其他公司坐在一起。顯然,該公司的許多投資者並不像最近的情況所顯示的那樣悲觀,他們現在不願拋售自己的股票。維持這些價格將很難實現,因為最近的收入趨勢可能最終會拖累股價。

The Key Takeaway

關鍵的外賣

With its share price dropping off a cliff, the P/S for GRP looks to be in line with the rest of the Electronic industry. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

隨著GRP股價的斷崖式下跌,GRP的本益比看起來與電子行業的其他公司一致。通常情況下,在做出投資決策時,我們會告誡不要過度解讀本益比,儘管它可以充分揭示其他市場參與者對該公司的看法。

Our examination of GRP revealed its poor three-year revenue trends aren't resulting in a lower P/S as per our expectations, given they look worse than current industry outlook. Right now we are uncomfortable with the P/S as this revenue performance isn't likely to support a more positive sentiment for long. If recent medium-term revenue trends continue, the probability of a share price decline will become quite substantial, placing shareholders at risk.

我們對GRP的調查顯示,其糟糕的三年收入趨勢並沒有像我們預期的那樣導致較低的本益比/S,因為它們看起來比當前的行業前景更糟糕。目前,我們對本益比/S感到不舒服,因為這種收入表現不太可能長期支持更積極的情緒。如果近期的中期營收趨勢持續下去,股價下跌的可能性將變得相當大,將股東置於風險之中。

You should always think about risks. Case in point, we've spotted 3 warning signs for GRP you should be aware of.

你應該時刻考慮風險。舉個例子,我們發現GRP的3個警告標誌你應該意識到。

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

如果強大的盈利公司激起了你的想像力,那麼你就會想要看看這個。免費本益比較低(但已證明它們可以增加收益)的有趣公司名單。

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

對這篇文章有什麼反饋嗎?擔心內容嗎? 保持聯繫直接與我們聯繫.或者,也可以給編輯組發電子郵件,地址是暗示Wallst.com。

本文由Simply Wall St.撰寫,具有概括性.我們僅使用不偏不倚的方法提供基於歷史數據和分析師預測的評論,我們的文章並不打算作為財務建議.它不構成買賣任何股票的建議,也沒有考慮你的目標或你的財務狀況.我們的目標是為您帶來由基本面數據驅動的長期重點分析.請注意,我們的分析可能不會將最新的對價格敏感的公司公告或定性材料考慮在內.Simply Wall St.對上述任何一隻股票都沒有持倉.

譯文內容由第三人軟體翻譯。