Pinduoduo handed over its performance note last night: the month-on-month decline in revenue growth, and the growth rate of marketing expenses exceeding the growth rate of core advertising revenue raised market concerns. Is Pinduoduo's high growth rate unsustainable? When will the cross-border e-commerce business reap the benefits?

Last night, Pinduoduo revealed financial results for the fourth quarter and full year of '22.

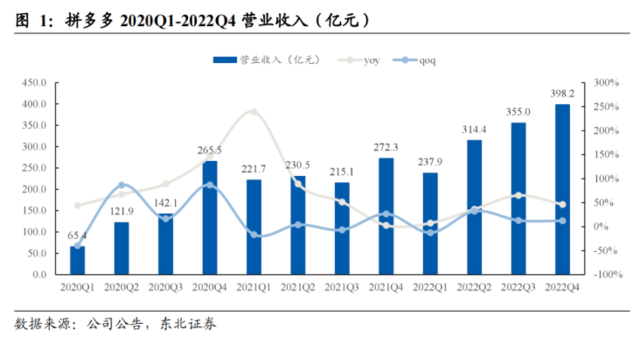

Revenue for the fourth quarter of last year was 39.8 billion yuan, up 46% year on year, up 12.2% month on month, lower than the unanimous forecast of 5.1%; Guimu's net profit was 12.11 billion yuan, up 43.4% year on year, down 2.7% month on month, higher than the unanimous forecast of 8.4%. The adjusted earnings per share were $8.34, higher than the forecast of $7.55.

Revenue for the full year of last year was 130.6 billion yuan, an increase of 39% over the previous year. Net profit for the full year of last year was 31,538 billion yuan, an increase of 306% over the previous year.

Under the extreme environment of the fourth quarter, Pinduoduo's revenue and profits were still able to grow by more than 40%.Net earnings per share were also higher than expected. Compared with the decline in the e-commerce sector, JD and Ali still showed strong resilience.

However, compared to myself, the 46% revenue growth rate in the fourth quarter was significantly lower than 65% in the third quarter.It has returned to the level of the second quarter.This makes the market wonder if Pinduoduo's high growth rate is unsustainable? At the same time, everyone is also concerned to what extent has Temu, Pinduoduo's key cross-border e-commerce business, developed?

The “inner volume” of the 10 billion subsidy has been upgraded

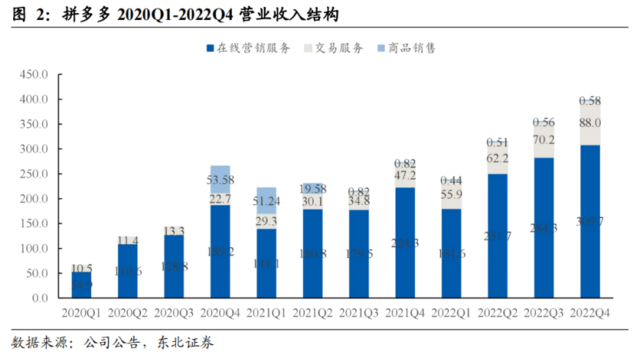

Looking at the split business, Pinduoduo's overall business is mainly divided into 3 segments: online marketing services (advertising), transaction services (commissions), and product sales, among whichAdvertising is the main source of revenue.This quarter, the core advertising revenue was 30.97 billion yuan, up 38.1% year on year; transaction commission revenue was 8.8 billion yuan, up 86.4% year on year; “advertising+commission” business revenue was 39.77 billion yuan, up 46.5% year on year. ,

We sawThe revenue growth rate of “advertising+commission” as the core business was slightly inferior compared to the previous quarter. Although it can still be called outstanding compared to e-commerce companies that have already published financial reports, I'm afraid we can't be too optimistic when looking at the situation over a long period of time.

On the one hand, there is the exhaustion of dividends in the e-commerce industry, and the peak growth of GMV (Total Merchandise Transactions) has become the consensus of the market. On the other hand, after the dividends were taken, the platforms had to fall into the “internal volume phase” in an attempt to retain users at lower prices. Pinduoduo CEO Chen Lei said in a telephone conference call that they would continue to increase subsidies. Even JD, which has always positioned the middle and high end, launched a 10 billion dollar subsidy in March.

How much impact did JD's “10 billion subsidy” have on Pinduoduo?

However, intellectual research suggests that JD's “10 billion subsidy” had little impact on Pinduoduo. First, there are still 2 important questions facing JD:Pinduoduo has already taken over the mentality of most cost-effective users through 3 years of 10 billion dollars of subsidies. How low will JD's price be to grab this segment of users? Can the ROI obtained from users through price-performance ratio be maintained at a reasonable level?

The opinion of insight research is that it will be difficult for JD to achieve both user growth and efficiency improvement. Especially in the context of economic recovery after the epidemic,JD will sacrifice part of its profit margin in exchange for user growth in the short term.

However, if you want long-term subsidies, I'm afraid it will be more difficult. On the one hand, long-term investment will have a great impact on the cost side.According to brokers' forecasts, based on the 5% subsidy ratio and the penetration rate of the “10 billion subsidy” GMV in the Jingdong market of 1%-5%, it is estimated that the “10 billion subsidy” will bring in an incremental GMV of 250 billion yuan and an incremental revenue of 67.2 billion yuan.The additional expenses brought about by the subsidies were about 6 billion yuan.The net decline in retail business was 3.5 billion yuan, correspondingOPM(Operating profit margin)The decline was about 53 bps(1 bps = 0.01%)

AgainFrom a cash flow perspective,The 10 billion dollar subsidy is not like large-scale events such as 618 or Double Eleven. Merchants reduce revenue per SKU in exchange for users, causing the merchant's interests to be greatly damaged.What is more damaged by the $10 billion subsidy is the platform's interests.

As of the fourth quarter of '22, cash and cash equivalents of Pinduoduo and JD were 92.3 billion yuan and 85.2 billion yuan respectively. Although JD's 10 billion subsidy is shared by 3P merchants (market sellers) and brands,With JD's current cash and equivalents situation, I'm afraid it will be difficult to support a protracted price war with 10 billion dollars to subsidize all categories for a long time.

When will overseas businesses that have smashed their money pay off?

It is worth noting that, judging from the financial data disclosed for this quarter,The growth rate of Pinduoduo's marketing expenses exceeds the growth rate of advertising revenue(Marketing expenses increased 56% year over year, compared to a 38% increase in advertising revenue),This is the first time since 2018.Although Pinduoduo did not break down domestic and foreign businesses in detail, insight research suggests that, on the one hand, because the fourth quarter was originally the peak season for e-commerce, including the big annual promotions for Double Eleven, marketing expenses were usually higher than in the third quarter. The other reason isThe acceleration of overseas cross-border e-commerce business TEMU has greatly increased marketing expenses.

So how is the overseas business that has been slashed so hard to develop?

Temu is a cross-border e-commerce brand owned by Pinduoduo. It went overseas to the US for the first time in September last year, continuing the “low price, good goods, social fission” style of the main site.Compared with local American brands, the competitive advantage of low prices is obvious. From the consumer's point of view,In December 2022, the average price of buying toys, office supplies, and handicrafts on Temu was $5.1, 2.8, and $3, respectively, and $26, 27, and $18 on Amzon during the same period.It's almost 5-10 times Temu's.

Also, if you look at it from a merchant's point of view,Merchants entering Amazon excluded 20%-30% of product costs, 8%-15% sales commissions, $39.99/month opening commission, 15%-20% tariff costs, and 10%-15% advertising and marketing costs, and profits were seriously reduced. In contrast, Pinduoduo's “Support Plan to Go Overseas” skewed some resources to merchants and solved matters other than supply for merchants, attracting many businesses to settle in. Currently, more than 30,000 businesses have settled in.

At the same time, Temu doesn't have a fuss when it comes to spending money on marketing.In February of this year, Temu spent 100 million dollars to buy a 60-second adGo to the “American Spring Festival Gala” Super BowlThis also caused Temu's traffic to skyrocket. According to Sensor Tower data, on the day of the Super Bowl game, TEMU's app downloads increased 45% compared to the previous day, and daily active users increased by about 20%.The total number of reported viewers reached 208 million people.

Spending money this hard has indeed brought about rapid growth in GMV.Currently, Temu's GMV estimate is 15 million US dollars per day, which has already reached one-tenth of the SHEIN target set earlier, and according to the latest cross-border e-commerce news, the domestic Guangzhou warehouse is already bursting out of stock due to too many orders from North America and being too late for delivery.However, losses due to high expenses also increased year-on-year, with Temu's annual loss reaching 4.13 billion yuan.

Regarding the increase in losses brought about by the rapid development of TEMU, insight research suggests that in addition to the high subsidy expenses and marketing expenses mentioned above, another factor is that logistics costs remain high.

Unlike SHEIN, which has set up multiple overseas transit warehouses overseas, Temu's express delivery usesThree-stage logistics, higher delivery costs(The first section is for domestic merchants to ship goods to the Guangzhou warehouse at a cost of 3.5 yuan/order; the second section is shipping from the Guangzhou warehouse to the US, with an average cost of 15 US dollars; the third section is shipping from the US local warehouse to the user's delivery address, with an average cost of 9-15 US dollars/order), accounting for 40%-50%.

In the future, this part of the high cost will be effectively diluted by increasing the value of individual packages.According to brokers' estimates,Fulfilment costs will account for around 34% in 2023, and are expected to drop to around 24% in '26.

Let's also look at customer acquisition costs. Since Temu is still in the early stages of expansion, it needs to spend a lot of money to acquire users, so it is difficult for this part of the cost to be effectively diluted. Only with the expansion of the user base and the increase in the value of a single user can the share of customer acquisition costs decrease. Finally, looking at the UE model, the OP margin for 2023 is expected to be around -33%.There will still be large loss margins in the short term. In the future, with the optimization of the above costs, we will achieve a break-even balance.

summed

Generally speaking, Pinduoduo is known for its cost-effective consumption in China. Over the years, it has used 10 billion dollars of subsidies to break out of its way in Taobao and Jingdong. Along with social fission, it quickly accumulated a large number of users, and profits were quickly released after sales expenses were reduced. Even when the overall environment was severe, other platforms experienced a good growth rate in the fourth quarter, when they were slightly weak. However, I have to admit thatE-commerce has already passed the era of high growth, and Pinduoduo is no exception. What we should pay attention to in the future is whether it can continue to obtain considerable GMV growth without expanding marketing expenses.

whereasThe cross-border e-commerce business Temu will become a huge variable in Pinduoduo's business. On the one hand, Pinduoduo's investment resources are skewed sharply towards Temu. On the other hand, Temu has made impressive progress. Currently, GMV revenue is growing rapidly, but it is still in the early stages of expansion where money needs to be spent, and losses are still large. Temu's break-even point will be an important milestone.

Editor/phoebe