Here's Why Manitowoc Company (NYSE:MTW) Is Weighed Down By Its Debt Load

Here's Why Manitowoc Company (NYSE:MTW) Is Weighed Down By Its Debt Load

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that The Manitowoc Company, Inc. (NYSE:MTW) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for Manitowoc Company

How Much Debt Does Manitowoc Company Carry?

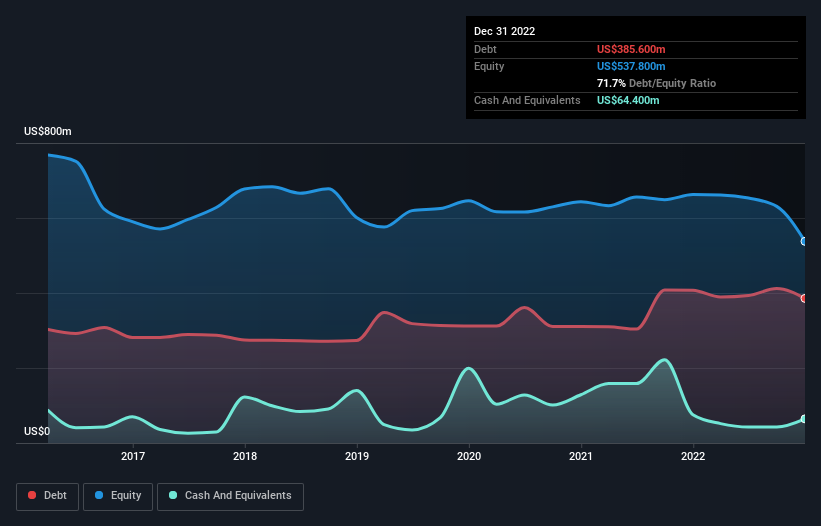

You can click the graphic below for the historical numbers, but it shows that Manitowoc Company had US$385.6m of debt in December 2022, down from US$407.2m, one year before. However, it also had US$64.4m in cash, and so its net debt is US$321.2m.

How Strong Is Manitowoc Company's Balance Sheet?

According to the last reported balance sheet, Manitowoc Company had liabilities of US$547.8m due within 12 months, and liabilities of US$529.9m due beyond 12 months. On the other hand, it had cash of US$64.4m and US$276.9m worth of receivables due within a year. So it has liabilities totalling US$736.4m more than its cash and near-term receivables, combined.

Given this deficit is actually higher than the company's market capitalization of US$630.1m, we think shareholders really should watch Manitowoc Company's debt levels, like a parent watching their child ride a bike for the first time. Hypothetically, extremely heavy dilution would be required if the company were forced to pay down its liabilities by raising capital at the current share price.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Even though Manitowoc Company's debt is only 2.2, its interest cover is really very low at 2.4. This does have us wondering if the company pays high interest because it is considered risky. Either way there's no doubt the stock is using meaningful leverage. Sadly, Manitowoc Company's EBIT actually dropped 8.3% in the last year. If that earnings trend continues then its debt load will grow heavy like the heart of a polar bear watching its sole cub. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Manitowoc Company's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we always check how much of that EBIT is translated into free cash flow. Over the last three years, Manitowoc Company recorded negative free cash flow, in total. Debt is far more risky for companies with unreliable free cash flow, so shareholders should be hoping that the past expenditure will produce free cash flow in the future.

Our View

On the face of it, Manitowoc Company's interest cover left us tentative about the stock, and its conversion of EBIT to free cash flow was no more enticing than the one empty restaurant on the busiest night of the year. Having said that, its ability handle its debt, based on its EBITDA, isn't such a worry. We're quite clear that we consider Manitowoc Company to be really rather risky, as a result of its balance sheet health. For this reason we're pretty cautious about the stock, and we think shareholders should keep a close eye on its liquidity. Given our concerns about Manitowoc Company's debt levels, it seems only prudent to check if insiders have been ditching the stock.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

传奇基金经理Li·Lu曾说过,最大的投资风险不是价格的波动,而是你是否会遭受永久性的资本损失。因此,当你评估一家公司的风险有多大时,聪明的投资者似乎知道债务--通常涉及破产--是一个非常重要的因素。我们注意到马尼托沃克公司。(纽约证券交易所股票代码:MTW)的资产负债表上确实有债务。但真正的问题是,这笔债务是否让该公司面临风险。

债务在什么时候是危险的?

债务是帮助企业发展的一种工具,但如果一家企业无法偿还贷款人的债务,那么它就只能听从贷款人的摆布。在最糟糕的情况下,如果一家公司无法偿还债权人的债务,它可能会破产。然而,一种更常见(但仍令人痛苦)的情景是,它不得不以低价筹集新的股本,从而永久性地稀释股东。当然,债务的好处是,它往往代表着廉价资本,特别是当它用能够以高回报率进行再投资的能力取代公司的稀释时。当我们检查债务水平时,我们首先同时考虑现金和债务水平。

查看我们对Manitowoc公司的最新分析

马尼托瓦克公司背负着多少债务?

你可以点击下图查看历史数据,但它显示马尼托瓦克公司在2022年12月的债务为3.856亿美元,低于一年前的4.072亿美元。然而,它也有6440万美元的现金,因此其净债务为3.212亿美元。

马尼托沃克公司的资产负债表有多强?

根据最新报告的资产负债表,Manitowoc公司有5.478亿美元的债务在12个月内到期,5.299亿美元的债务在12个月后到期。另一方面,它有6440万美元的现金和价值2.769亿美元的应收账款在一年内到期。因此,该公司的负债总额为7.364亿美元,比现金和近期应收账款的总和还要多。

鉴于这一赤字实际上高于该公司6.301亿美元的市值,我们认为股东们真的应该关注马尼托瓦克公司的债务水平,就像父母第一次看孩子骑车一样。假设,如果该公司被迫通过以当前股价筹集资金来偿还债务,将需要极大的稀释。

为了评估一家公司的债务相对于它的收益,我们计算它的净债务除以它的利息、税项、折旧和摊销前收益(EBITDA)和它的利息和税前收益(EBIT)除以它的利息支出(它的利息覆盖)。这种方法的优点是,我们既考虑了债务的绝对数量(净债务与EBITDA之比),也考虑了与债务相关的实际利息支出(及其利息覆盖率)。

尽管马尼托瓦克公司的债务只有2.2英镑,但它的利息覆盖率真的很低,只有2.4英镑。这确实让我们想知道,该公司是否因为被认为有风险而支付高额利息。无论哪种方式,毫无疑问,该股正在使用有意义的杠杆。遗憾的是,马尼托沃克公司去年的息税前利润实际上下降了8.3%。如果盈利趋势继续下去,那么它的债务负担将变得沉重,就像北极熊看着自己唯一的幼崽的心脏一样。当你分析债务时,资产负债表显然是你关注的领域。但最重要的是,未来的收益将决定马尼托沃克公司未来保持健康资产负债表的能力。因此,如果你想看看专业人士的想法,你可能会发现这份关于分析师利润预测的免费报告很有趣。

最后,一家公司只能用冷硬现金偿还债务,而不是会计利润。因此,我们总是检查EBIT中有多少转化为自由现金流。在过去的三年中,马尼托瓦克公司的自由现金流总额为负。对于自由现金流不可靠的公司来说,债务的风险要大得多,因此股东们应该希望过去的支出能在未来产生自由现金流。

我们的观点

从表面上看,Manitowoc公司的利息担保让我们对这只股票持怀疑态度,它将息税前利润转换为自由现金流并不比一年中最繁忙的夜晚的一家空荡荡的餐厅更具诱惑力。话虽如此,根据其EBITDA,它处理债务的能力并不是那么令人担忧。我们非常清楚,由于马尼托沃克公司的资产负债表状况良好,我们认为该公司确实相当有风险。出于这个原因,我们对该股相当谨慎,我们认为股东应该密切关注其流动性。鉴于我们对Manitowoc公司债务水平的担忧,检查内部人士是否一直在抛售该股似乎是唯一谨慎的做法。

归根结底,关注那些没有净债务的公司往往更好。你可以访问我们的这类公司的特别名单(都有利润增长的记录)。这是免费的。

对这篇文章有什么反馈吗?担心内容吗?保持联系直接与我们联系。或者,也可以给编辑组发电子邮件,地址是implywallst.com。

本文由Simply Wall St.撰写,具有概括性。我们仅使用不偏不倚的方法提供基于历史数据和分析师预测的评论,我们的文章并不打算作为财务建议。它不构成买卖任何股票的建议,也没有考虑你的目标或你的财务状况。我们的目标是为您带来由基本面数据驱动的长期重点分析。请注意,我们的分析可能不会将最新的对价格敏感的公司公告或定性材料考虑在内。Simply Wall St.对上述任何一只股票都没有持仓。

译文内容由第三方软件翻译。

风险及免责提示

- 分享到weixin

- 分享到qq

- 分享到facebook

- 分享到twitter

- 分享到微博

- 粘贴板

使用浏览器的分享功能,分享给你的好友吧