Hong Leong Asia's (SGX:H22) Anemic Earnings Might Be Worse Than You Think

Hong Leong Asia's (SGX:H22) Anemic Earnings Might Be Worse Than You Think

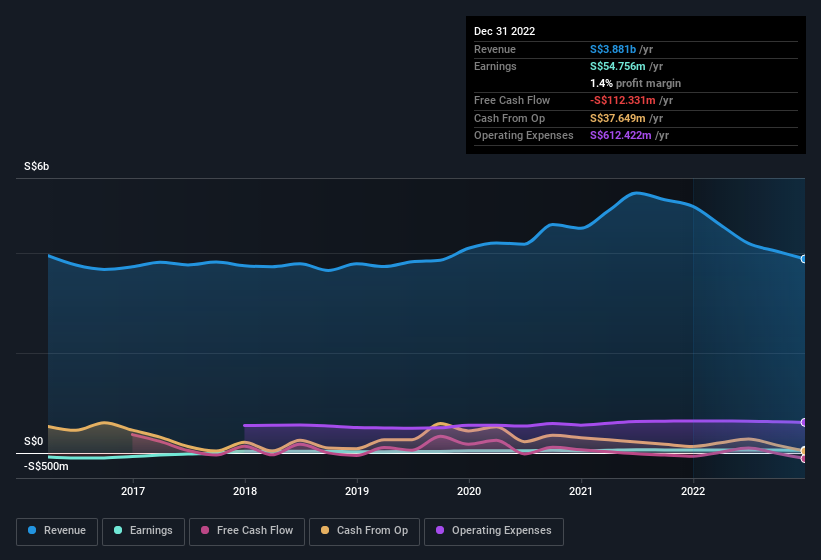

A lackluster earnings announcement from Hong Leong Asia Ltd. (SGX:H22) last week didn't sink the stock price. Our analysis suggests that along with soft profit numbers, investors should be aware of some other underlying weaknesses in the numbers.

View our latest analysis for Hong Leong Asia

The Impact Of Unusual Items On Profit

To properly understand Hong Leong Asia's profit results, we need to consider the S$10m gain attributed to unusual items. While it's always nice to have higher profit, a large contribution from unusual items sometimes dampens our enthusiasm. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. And that's as you'd expect, given these boosts are described as 'unusual'. Assuming those unusual items don't show up again in the current year, we'd thus expect profit to be weaker next year (in the absence of business growth, that is).

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

Our Take On Hong Leong Asia's Profit Performance

Arguably, Hong Leong Asia's statutory earnings have been distorted by unusual items boosting profit. Therefore, it seems possible to us that Hong Leong Asia's true underlying earnings power is actually less than its statutory profit. But at least holders can take some solace from the 19% per annum growth in EPS for the last three. Of course, we've only just scratched the surface when it comes to analysing its earnings; one could also consider margins, forecast growth, and return on investment, among other factors. If you'd like to know more about Hong Leong Asia as a business, it's important to be aware of any risks it's facing. While conducting our analysis, we found that Hong Leong Asia has 1 warning sign and it would be unwise to ignore this.

This note has only looked at a single factor that sheds light on the nature of Hong Leong Asia's profit. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

一份平淡无奇的财报康亮亚洲有限公司。(新加坡证券交易所股票代码:H22)上周的股价并未下跌。我们的分析表明,除了疲软的利润数据外,投资者还应该意识到数字中的其他一些潜在弱点。

查看我们对Hong Leong Asia的最新分析

异常项目对利润的影响

为了正确理解宏利亚洲的盈利业绩,我们需要考虑一下归因于不寻常项目的1000万新元收益。虽然有更高的利润总是好事,但不寻常的东西带来的巨大贡献有时会挫伤我们的热情。当我们分析全球绝大多数上市公司时,我们发现重大的不寻常项目往往不会重复。考虑到这些提振被描述为“不寻常的”,这正如你所预期的那样。假设这些不同寻常的项目在本年度不会再次出现,我们因此预计明年的利润会更弱(也就是说,在没有业务增长的情况下)。

这可能会让你想知道,分析师对未来盈利能力的预测是什么。幸运的是,您可以单击此处查看基于他们估计的未来盈利能力的互动图表。

我们对宏亮亚洲盈利表现的看法

可以说,宏亮亚洲的法定收益被不寻常的提振利润项目扭曲了。因此,在我们看来,宏利亚洲的真实潜在盈利能力实际上可能低于其法定利润。但至少持有者可以从过去三年每股收益每年19%的增长中得到一些安慰。当然,当谈到分析其收益时,我们只是触及了皮毛;人们还可以考虑利润率、预测增长和投资回报等因素。如果你想更多地了解宏隆亚洲的业务,了解它面临的任何风险是很重要的。我们在进行分析时发现,康亮亚洲1个警告标志忽视这一点是不明智的。

这份报告只关注了一个因素,这一因素揭示了宏利亚洲的利润性质。但还有很多其他方式可以让你了解一家公司的看法。一些人认为,高股本回报率是高质量企业的良好标志。虽然这可能需要为您做一些研究,但您可能会发现免费拥有高股本回报率的公司的集合,或者是内部人士购买的有用的股票清单。

对这篇文章有什么反馈吗?担心内容吗?保持联系直接与我们联系。或者,也可以给编辑组发电子邮件,地址是implywallst.com。

本文由Simply Wall St.撰写,具有概括性。我们仅使用不偏不倚的方法提供基于历史数据和分析师预测的评论,我们的文章并不打算作为财务建议。它不构成买卖任何股票的建议,也没有考虑你的目标或你的财务状况。我们的目标是为您带来由基本面数据驱动的长期重点分析。请注意,我们的分析可能不会将最新的对价格敏感的公司公告或定性材料考虑在内。Simply Wall St.对上述任何一只股票都没有持仓。

译文内容由第三方软件翻译。

风险及免责提示

- 分享到weixin

- 分享到qq

- 分享到facebook

- 分享到twitter

- 分享到微博

- 粘贴板

使用浏览器的分享功能,分享给你的好友吧