Here's Why United Overseas Bank (SGX:U11) Has Caught The Eye Of Investors

Here's Why United Overseas Bank (SGX:U11) Has Caught The Eye Of Investors

Investors are often guided by the idea of discovering 'the next big thing', even if that means buying 'story stocks' without any revenue, let alone profit. Sometimes these stories can cloud the minds of investors, leading them to invest with their emotions rather than on the merit of good company fundamentals. A loss-making company is yet to prove itself with profit, and eventually the inflow of external capital may dry up.

Despite being in the age of tech-stock blue-sky investing, many investors still adopt a more traditional strategy; buying shares in profitable companies like United Overseas Bank (SGX:U11). Even if this company is fairly valued by the market, investors would agree that generating consistent profits will continue to provide United Overseas Bank with the means to add long-term value to shareholders.

Check out our latest analysis for United Overseas Bank

How Fast Is United Overseas Bank Growing Its Earnings Per Share?

Even when EPS earnings per share (EPS) growth is unexceptional, company value can be created if this rate is sustained each year. So it's easy to see why many investors focus in on EPS growth. United Overseas Bank's EPS has risen over the last 12 months, growing from S$2.17 to S$2.61. That's a 20% gain; respectable growth in the broader scheme of things.

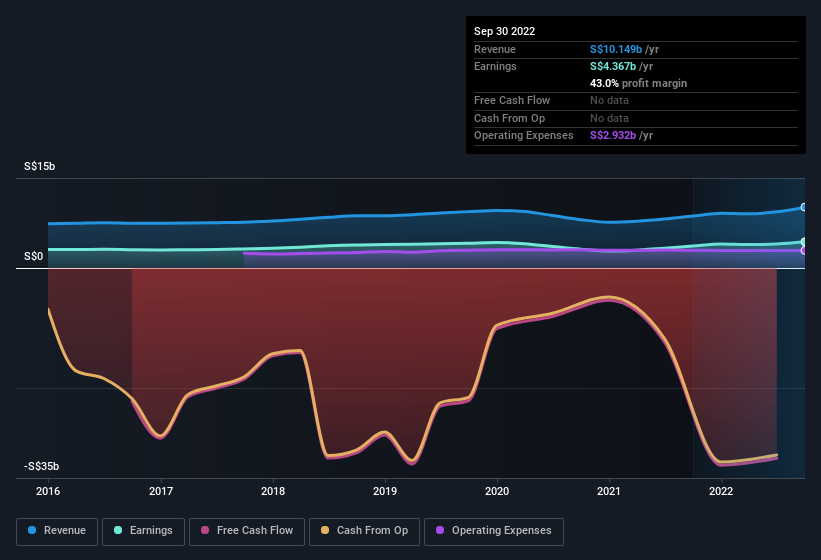

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. Not all of United Overseas Bank's revenue this year is revenue from operations, so keep in mind the revenue and margin numbers used in this article might not be the best representation of the underlying business. United Overseas Bank maintained stable EBIT margins over the last year, all while growing revenue 17% to S$10b. That's encouraging news for the company!

The chart below shows how the company's bottom and top lines have progressed over time. Click on the chart to see the exact numbers.

SGX:U11 Earnings and Revenue History December 13th 2022

SGX:U11 Earnings and Revenue History December 13th 2022You don't drive with your eyes on the rear-view mirror, so you might be more interested in this free report showing analyst forecasts for United Overseas Bank's future profits.

Are United Overseas Bank Insiders Aligned With All Shareholders?

It's said that there's no smoke without fire. For investors, insider buying is often the smoke that indicates which stocks could set the market alight. Because often, the purchase of stock is a sign that the buyer views it as undervalued. However, insiders are sometimes wrong, and we don't know the exact thinking behind their acquisitions.

The real kicker here is that United Overseas Bank insiders spent a staggering S$3.3m on acquiring shares in just one year, without single share being sold in the meantime. The shareholders within the general public should find themselves expectant and certainly hopeful, that this large outlay signals prescient optimism for the business. Zooming in, we can see that the biggest insider purchase was by Deputy Chairman & CEO Ee Cheong Wee for S$1.3m worth of shares, at about S$26.95 per share.

The good news, alongside the insider buying, for United Overseas Bank bulls is that insiders (collectively) have a meaningful investment in the stock. We note that their impressive stake in the company is worth S$8.2b. Coming in at 16% of the business, that holding gives insiders a lot of influence, and plenty of reason to generate value for shareholders. So there is opportunity here to invest in a company whose management have tangible incentives to deliver.

Should You Add United Overseas Bank To Your Watchlist?

One positive for United Overseas Bank is that it is growing EPS. That's nice to see. Better yet, insiders are significant shareholders, and have been buying more shares. That makes the company a prime candidate for your watchlist - and arguably a research priority. What about risks? Every company has them, and we've spotted 1 warning sign for United Overseas Bank you should know about.

The good news is that United Overseas Bank is not the only growth stock with insider buying. Here's a list of them... with insider buying in the last three months!

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

投资者往往以发现“下一个大事件”为指导,即使这意味着在没有任何收入、更不用说利润的情况下买入“故事股”。有时,这些故事可能会蒙蔽投资者的头脑,导致他们以自己的情绪投资,而不是投资于良好的公司基本面。一家亏损的公司还没有用盈利来证明自己,最终外部资本的流入可能会枯竭。

尽管处于科技股蓝天投资的时代,许多投资者仍采取更传统的策略;购买盈利的公司的股票,如大华银行(新加坡证券交易所:U11)。即使大华银行得到市场的公平估值,投资者也会同意,产生稳定的利润将继续为大华银行提供为股东增加长期价值的手段。

查看我们对大华银行的最新分析

大华银行每股收益增长速度有多快?

即使在每股收益(EPS)增长正常的情况下,如果每年保持这一速度,也可以创造公司价值。因此,很容易理解为什么许多投资者关注每股收益的增长。大华银行的每股收益在过去12个月里有所上升,从2.17新元增至2.61新元。这是20%的增长;从更广泛的角度来看,这是一个可观的增长。

仔细考虑收入增长和息税前利润(EBIT)利润率有助于了解最近利润增长的可持续性。大华银行今年的营收并非全部是营收从运营部因此,请记住,本文中使用的收入和利润率数字可能不是基础业务的最佳代表。大华银行去年保持了稳定的息税前利润,同时收入增长了17%,达到100亿新元。这对公司来说是个鼓舞人心的消息!

下面的图表显示了该公司的利润和收入是如何随着时间的推移而变化的。点击图表查看确切的数字。

新交所:U11收益和收入历史2022年12月13日你开车的时候眼睛不会盯着后视镜,所以你可能会对这个更感兴趣免费显示分析师对大华银行预测的报告未来利润。

大华银行内部人士是否与所有股东一致?

有人说,无风不起浪。对于投资者来说,内幕购买往往是表明哪些股票可能点燃市场的烟雾。因为通常情况下,购买股票是买家认为其价值被低估的迹象。然而,内部人士有时是错的,我们不知道他们收购背后的确切想法。

真正的问题是,大华银行内部人士在短短一年内斥资330万新元购入股份,而在此期间却没有出售任何股份。普通公众中的股东应该发现自己期待着,当然也充满希望,因为这笔巨额支出标志着对企业的先见之明的乐观。放大后,我们可以看到,最大的内部收购是副董事长兼首席执行官EE Cheong Wee以每股26.95新元的价格收购了价值130万新元的股票。

对于看涨大华银行的人来说,除了内部人士购买外,好消息是内部人士(集体)对大华银行股票进行了有意义的投资。我们注意到,他们在该公司令人印象深刻的股份价值82亿新元。持股比例为16%,这给内部人士带来了很大的影响力,也有足够的理由为股东创造价值。因此,这里有机会投资于一家管理层具有切实激励措施的公司。

您是否应该将大华银行列入您的观察名单?

大华银行的一个利好消息是,它的每股收益正在增长。很高兴见到你。更好的是,内部人士是大股东,他们一直在买入更多股票。这使该公司成为你观察名单的首选--也可以说是研究重点。那么风险呢?每家公司都有它们,我们已经发现大华银行的1个警告标志你应该知道。

好消息是,大华银行并不是唯一一只有内幕买入的成长股。这是他们的名单。在过去的三个月里有内幕交易!

请注意,本文中讨论的内幕交易指的是相关司法管辖区内的应报告交易。

对这篇文章有什么反馈吗?担心内容吗? 保持联系直接与我们联系。或者,也可以给编辑组发电子邮件,地址是implywallst.com。

本文由Simply Wall St.撰写,具有概括性。我们仅使用不偏不倚的方法提供基于历史数据和分析师预测的评论,我们的文章并不打算作为财务建议。它不构成买卖任何股票的建议,也没有考虑你的目标或你的财务状况。我们的目标是为您带来由基本面数据驱动的长期重点分析。请注意,我们的分析可能不会将最新的对价格敏感的公司公告或定性材料考虑在内。Simply Wall St.对上述任何一只股票都没有持仓。

译文内容由第三方软件翻译。

风险及免责提示

- 分享到weixin

- 分享到qq

- 分享到facebook

- 分享到twitter

- 分享到微博

- 粘贴板

使用浏览器的分享功能,分享给你的好友吧