Will Jumia Technologies (NYSE:JMIA) Spend Its Cash Wisely?

Will Jumia Technologies (NYSE:JMIA) Spend Its Cash Wisely?

Just because a business does not make any money, does not mean that the stock will go down. For example, although software-as-a-service business Salesforce.com lost money for years while it grew recurring revenue, if you held shares since 2005, you'd have done very well indeed. But the harsh reality is that very many loss making companies burn through all their cash and go bankrupt.

Given this risk, we thought we'd take a look at whether Jumia Technologies (NYSE:JMIA) shareholders should be worried about its cash burn. For the purposes of this article, cash burn is the annual rate at which an unprofitable company spends cash to fund its growth; its negative free cash flow. Let's start with an examination of the business' cash, relative to its cash burn.

Check out our latest analysis for Jumia Technologies

When Might Jumia Technologies Run Out Of Money?

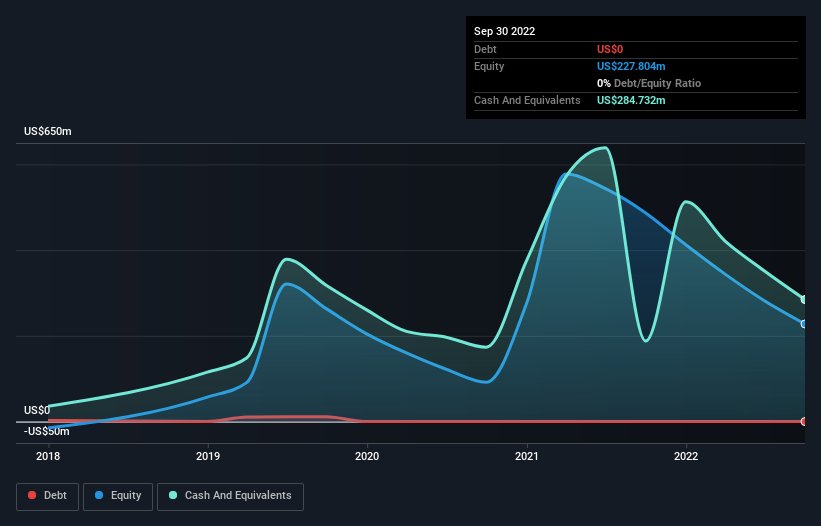

A company's cash runway is calculated by dividing its cash hoard by its cash burn. In September 2022, Jumia Technologies had US$285m in cash, and was debt-free. Looking at the last year, the company burnt through US$264m. So it had a cash runway of approximately 13 months from September 2022. Notably, analysts forecast that Jumia Technologies will break even (at a free cash flow level) in about 3 years. Essentially, that means the company will either reduce its cash burn, or else require more cash. The image below shows how its cash balance has been changing over the last few years.

NYSE:JMIA Debt to Equity History December 3rd 2022

NYSE:JMIA Debt to Equity History December 3rd 2022How Well Is Jumia Technologies Growing?

Jumia Technologies boosted investment sharply in the last year, with cash burn ramping by 83%. But the silver lining is that operating revenue increased by 30% in that time. In light of the data above, we're fairly sanguine about the business growth trajectory. Clearly, however, the crucial factor is whether the company will grow its business going forward. So you might want to take a peek at how much the company is expected to grow in the next few years.

Can Jumia Technologies Raise More Cash Easily?

While Jumia Technologies seems to be in a fairly good position, it's still worth considering how easily it could raise more cash, even just to fuel faster growth. Companies can raise capital through either debt or equity. Commonly, a business will sell new shares in itself to raise cash and drive growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

Jumia Technologies' cash burn of US$264m is about 56% of its US$474m market capitalisation. From this perspective, it seems that the company spent a huge amount relative to its market value, and we'd be very wary of a painful capital raising.

How Risky Is Jumia Technologies' Cash Burn Situation?

Even though its cash burn relative to its market cap makes us a little nervous, we are compelled to mention that we thought Jumia Technologies' revenue growth was relatively promising. Shareholders can take heart from the fact that analysts are forecasting it will reach breakeven. Looking at the factors mentioned in this short report, we do think that its cash burn is a bit risky, and it does make us slightly nervous about the stock. Readers need to have a sound understanding of business risks before investing in a stock, and we've spotted 2 warning signs for Jumia Technologies that potential shareholders should take into account before putting money into a stock.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of companies insiders are buying, and this list of stocks growth stocks (according to analyst forecasts)

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

仅仅因为企业没有赚钱,并不意味着股票会下跌。例如,尽管软件即服务业务Salesforce.com在增加经常性收入的同时亏损了多年,但如果你自2005年以来持有股票,你确实会做得很好。但残酷的现实是,许多亏损的公司耗尽了所有现金并破产。

鉴于这种风险,我们想看看是否 Jumia 科技 (纽约证券交易所代码:JMIA)的股东应该担心其现金消耗。就本文而言,现金消耗是指无利可图的公司花费现金为其增长提供资金的年利率;其自由现金流为负。让我们从研究一下企业的现金消耗与其现金消耗的关系开始。

查看我们对 Jumia Technologies 的最新分析

Jumia Technologies 什么时候会没钱?

公司的现金流是用现金储备除以现金消耗来计算的。2022年9月,Jumia Technologies拥有2.85亿美元的现金,并且没有债务。纵观去年,该公司耗尽了2.64亿美元。因此,从2022年9月起,它的现金流持续了大约13个月。值得注意的是,分析师预测,Jumia Technologies将在大约3年内实现收支平衡(在自由现金流水平上)。从本质上讲,这意味着该公司要么减少现金消耗,要么需要更多的现金。下图显示了其现金余额在过去几年中的变化。

纽约证券交易所:JMIA 2022 年 12 月 3 日债转股历史Jumia 科技的增长情况如何?

去年,Jumia Technologies大幅增加了投资,现金消耗增加了83%。但一线希望是,在此期间,营业收入增长了30%。鉴于上述数据,我们对业务增长轨迹相当乐观。但是,显然,关键因素是该公司未来是否会发展业务。因此,你可能想看看该公司在未来几年预计将增长多少。

Jumia Technologies 能否轻松筹集更多

尽管Jumia Technologies似乎处于相当不错的地位,但仍然值得考虑的是,即使只是为了推动更快的增长,它也可以轻松地筹集到更多现金。公司可以通过债务或股权筹集资金。通常,企业会自行出售新股以筹集现金并推动增长。通过将一家公司的年度现金消耗与其总市值进行比较,我们可以大致估计它必须发行多少股才能将公司再经营一年(以相同的消耗率)。

Jumia Technologies的2.64亿美元现金消耗约为其4.74亿美元市值的56%。从这个角度来看,相对于其市值,该公司似乎花费了巨额资金,我们对痛苦的融资非常警惕。

Jumia Technologies 的现金消耗情况有多风险?

尽管相对于市值而言,它的现金消耗使我们有点紧张,但我们不得不提及的是,我们认为Jumia Technologies的收入增长相对乐观。股东们可以从分析师预测它将达到盈亏平衡这一事实中振作起来。从这份简短的报告中提到的因素来看,我们确实认为它的现金消耗有点风险,这确实使我们对这只股票有些紧张。读者在投资股票之前需要对商业风险有充分的了解,我们已经发现 Jumia Technologies 有 潜在股东在向股票投入资金之前应该考虑到这一点。

当然, 你可能会在其他地方找到一笔不错的投资。 所以来看看这个 免费的 内部人士正在买入的公司名单,以及这份成长型股票清单(根据分析师的预测)

对这篇文章有反馈吗?对内容感到担忧? 取得联系 直接和我们联系。 或者,给编辑团队 (at) simplywallst.com 发送电子邮件。

Simply Wall St 的这篇文章本质上是一般性的。 我们仅使用不偏不倚的方法根据历史数据和分析师预测提供评论,我们的文章并非旨在提供财务建议。 它不构成买入或卖出任何股票的建议,也没有考虑您的目标或财务状况。我们的目标是为您提供由基本面数据驱动的长期重点分析。请注意,我们的分析可能未将最新的价格敏感型公司公告或定性材料考虑在内。简而言之,华尔街对上述任何股票都没有头寸。

译文内容由第三方软件翻译。

风险及免责提示

- 分享到weixin

- 分享到qq

- 分享到facebook

- 分享到twitter

- 分享到微博

- 粘贴板

使用浏览器的分享功能,分享给你的好友吧