Avarga Limited (SGX:U09) shares have had a really impressive month, gaining 33% after a shaky period beforehand. Unfortunately, the gains of the last month did little to right the losses of the last year with the stock still down 17% over that time.

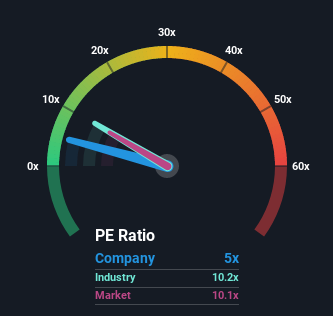

In spite of the firm bounce in price, Avarga's price-to-earnings (or "P/E") ratio of 5x might still make it look like a strong buy right now compared to the market in Singapore, where around half of the companies have P/E ratios above 11x and even P/E's above 18x are quite common. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so limited.

For instance, Avarga's receding earnings in recent times would have to be some food for thought. One possibility is that the P/E is low because investors think the company won't do enough to avoid underperforming the broader market in the near future. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

Check out our latest analysis for Avarga

SGX:U09 Price Based on Past Earnings October 31st 2022 Although there are no analyst estimates available for Avarga, take a look at this

free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.

How Is Avarga's Growth Trending?

Avarga's P/E ratio would be typical for a company that's expected to deliver very poor growth or even falling earnings, and importantly, perform much worse than the market.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 59%. Even so, admirably EPS has lifted 65% in aggregate from three years ago, notwithstanding the last 12 months. Accordingly, while they would have preferred to keep the run going, shareholders would probably welcome the medium-term rates of earnings growth.

This is in contrast to the rest of the market, which is expected to grow by 3.4% over the next year, materially lower than the company's recent medium-term annualised growth rates.

With this information, we find it odd that Avarga is trading at a P/E lower than the market. Apparently some shareholders believe the recent performance has exceeded its limits and have been accepting significantly lower selling prices.

The Key Takeaway

Avarga's recent share price jump still sees its P/E sitting firmly flat on the ground. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

Our examination of Avarga revealed its three-year earnings trends aren't contributing to its P/E anywhere near as much as we would have predicted, given they look better than current market expectations. When we see strong earnings with faster-than-market growth, we assume potential risks are what might be placing significant pressure on the P/E ratio. It appears many are indeed anticipating earnings instability, because the persistence of these recent medium-term conditions would normally provide a boost to the share price.

You always need to take note of risks, for example - Avarga has 1 warning sign we think you should be aware of.

You might be able to find a better investment than Avarga. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a P/E below 20x (but have proven they can grow earnings).

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Avarga Limited(SGX:U09)股價在經歷了一段不穩定的時期後,經歷了令人印象深刻的一個月,上漲了33%。不幸的是,上個月的收益幾乎沒有彌補去年的損失,在此期間,該股仍下跌了17%。

儘管Avarga股價強勁反彈,但與新加坡股市相比,Avarga目前5倍的市盈率可能仍是一個強勁的買入。在新加坡,大約一半的公司的市盈率高於11倍,甚至市盈率高於18倍的情況也很常見。儘管如此,僅僅從面值來看待市盈率是不明智的,因為可能會有一個解釋,為什麼它如此有限。

例如,Avarga近期不斷下滑的收益肯定值得深思。一種可能性是,市盈率較低是因為投資者認為該公司在不久的將來不會採取足夠的措施來避免表現遜於大盤。如果你喜歡這家公司,你會希望情況並非如此,這樣你就可以在它不再受青睞的時候買入一些股票。

查看我們對Avarga的最新分析

新交所:U09價格基於過去的收益2022年10月31日雖然沒有分析師對Avarga的估計,但看看這個

免費豐富的數據可視化,看看公司的收益、收入和現金流是如何堆積的。

Avarga的增長趨勢如何?

Avarga的市盈率對於一家公司來説是典型的,因為預計這家公司的增長非常糟糕,甚至會出現收益下降,更重要的是,它的表現遠遠遜於市場。

首先回顧一下,該公司去年的每股收益增長並不令人興奮,因為它公佈了令人失望的59%的降幅。即便如此,令人欽佩的是,儘管在過去的12個月裏,每股收益比三年前累計上漲了65%。因此,儘管股東們更願意繼續運營,但他們可能會歡迎中期的盈利增長率。

這與市場其他部分形成對比,後者預計明年增長3.4%,大大低於該公司最近的中期年化增長率。

有了這些信息,我們發現Avarga的市盈率低於市場,這很奇怪。顯然,一些股東認為,最近的表現已經超出了極限,他們一直在接受明顯較低的售價。

關鍵的外賣

Avarga最近的股價上漲仍顯示其市盈率停滯不前。有人認為,市盈率是衡量某些行業價值的次要指標,但它可以成為一個強大的商業信心指標。

我們對Avarga的調查顯示,鑑於Avarga的三年收益趨勢看起來好於當前的市場預期,它對市盈率的貢獻遠沒有我們預期的那麼大。當我們看到強勁的收益和快於市場的增長時,我們認為潛在的風險可能會給市盈率帶來重大壓力。似乎許多人確實預計到了盈利不穩定,因為近期這些中期狀況的持續通常會提振股價。

你總是需要注意風險,例如-Avarga有一個警告標誌我們認為你應該意識到。

你或許能找到比Avarga更好的投資。如果您想要選擇可能的候選人,請查看以下內容免費令人感興趣的市盈率低於20倍的公司名單(但已證明它們可以增加收益)。

對這篇文章有什麼反饋嗎?擔心內容嗎? 保持聯繫直接與我們聯繫。或者,也可以給編輯組發電子郵件,地址是implywallst.com。

本文由Simply Wall St.撰寫,具有概括性。我們僅使用不偏不倚的方法提供基於歷史數據和分析師預測的評論,我們的文章並不打算作為財務建議。它不構成買賣任何股票的建議,也沒有考慮你的目標或你的財務狀況。我們的目標是為您帶來由基本面數據驅動的長期重點分析。請注意,我們的分析可能不會將最新的對價格敏感的公司公告或定性材料考慮在內。Simply Wall St.對上述任何一隻股票都沒有持倉。