When ASL Marine Holdings Ltd. (SGX:A04) reported its results to June 2022 its auditors, Ernst & Young LLP could not be sure that it would be able to continue as a going concern in the next year. It is therefore fair to assume that, based on those financials, the company should strengthen its balance sheet in the short term, perhaps by issuing shares.

If the company does have to issue more shares, potential investors will be sure to consider how desperate it is for capital. So current risks on the balance sheet could have a big impact on how shareholders fare from here. Debt is always a risk factor in these cases, as creditors could be in a position to wind up the company, in the worst case scenario.

View our latest analysis for ASL Marine Holdings

What Is ASL Marine Holdings's Net Debt?

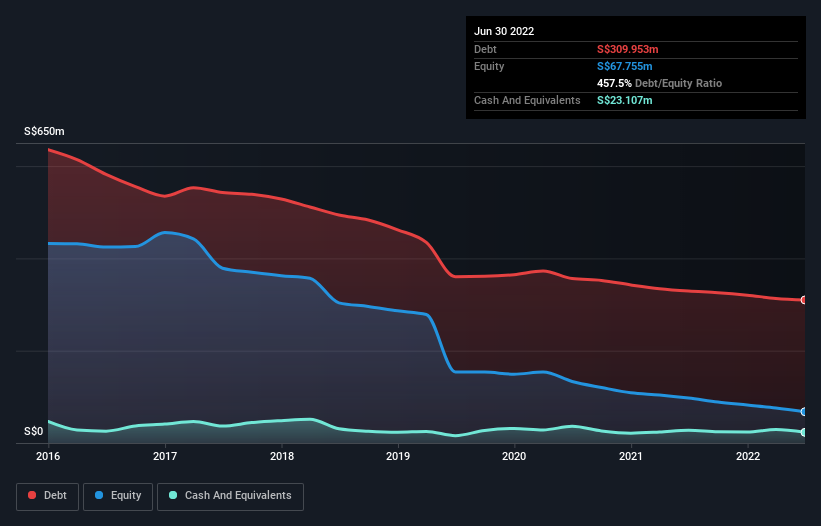

As you can see below, ASL Marine Holdings had S$310.0m of debt at June 2022, down from S$329.1m a year prior. However, it also had S$23.1m in cash, and so its net debt is S$286.8m.

SGX:A04 Debt to Equity History October 14th 2022

How Healthy Is ASL Marine Holdings' Balance Sheet?

We can see from the most recent balance sheet that ASL Marine Holdings had liabilities of S$230.7m falling due within a year, and liabilities of S$285.5m due beyond that. On the other hand, it had cash of S$23.1m and S$76.7m worth of receivables due within a year. So its liabilities total S$416.4m more than the combination of its cash and short-term receivables.

This deficit casts a shadow over the S$23.3m company, like a colossus towering over mere mortals. So we'd watch its balance sheet closely, without a doubt. After all, ASL Marine Holdings would likely require a major re-capitalisation if it had to pay its creditors today. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since ASL Marine Holdings will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year ASL Marine Holdings wasn't profitable at an EBIT level, but managed to grow its revenue by 22%, to S$236m. With any luck the company will be able to grow its way to profitability.

Caveat Emptor

Despite the top line growth, ASL Marine Holdings still had an earnings before interest and tax (EBIT) loss over the last year. Indeed, it lost a very considerable S$16m at the EBIT level. Reflecting on this and the significant total liabilities, it's hard to know what to say about the stock because of our intense dis-affinity for it. Sure, the company might have a nice story about how they are going on to a brighter future. But the reality is that it is low on liquid assets relative to liabilities, and it lost S$32m in the last year. So we think buying this stock is risky. We prefer to avoid a company after its auditor has expressed any uncertainty about its ability to continue as a going concern. That's because we find it more comfortable to invest in companies that always keep the balance sheet reasonably strong. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. Be aware that ASL Marine Holdings is showing 2 warning signs in our investment analysis , and 1 of those is potentially serious...

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

何時 亞洲海事控股有限公司 SGX:A04)在 2022 年 6 月向其審計師報告了其業績,安永有限責任公司無法確定它將能夠繼續在明年繼續擔憂。因此,可以公平地假設,根據這些財務狀況,公司應該在短期內加強其資產負債表,也許是通過發行股票。

如果公司確實需要發行更多股票,潛在投資者一定會考慮資本的絕望程度。因此,資產負債表上的當前風險可能會對股東從這裡開始的票價產生重大影響。在這些情況下,債務始終是風險因素,因為在最壞的情況下,債權人可能處於清盤公司的位置。

查看我們對亞洲海洋控股的最新分析

什麼是亞洲海事控股的淨債務?

如下所示,亞洲海事控股於 2022 年 6 月的債務總額為 310.00 萬新加坡元,較前一年的 329.1 億新加坡元下降。但是,它也有 2100 萬新加坡元的現金,因此其淨債務為 286.8 億新加坡元。

新加坡代碼:A04 債務對股本歷史記錄 2022 年 10 月 14 日

ASL 海洋控股的資產負債表健康程度如何?

從最近的資產負債表中,我們可以看出,亞洲海事控股在一年內到期負債為 230.7 億新加坡元,負債超出了 285.5 億新加坡元。另一方面,該公司有 230 萬新加坡元的現金和價值 76.7 億新加坡元的應收帳款。因此,其負債總額超過其現金和短期應收帳款的總額為 416.4 億新元。

這種赤字為 2300 萬新元的公司帶來了陰影,就像一個聳立在凡人之上的巨人。因此,毫無疑問,我們會密切關注其資產負債表。畢竟,如果亞洲海事控股今天必須支付其債權人,則可能需要進行重大的重新資本化。在分析債務水平時,資產負債表是顯而易見的起點。但是您無法完全隔離查看債務;因為 ASL 海洋控股將需要收入來為該債務提供服務。因此,在考慮債務時,絕對值得一看的盈利趨勢。按一下這裡以取得互動式快照。

在去年,亞洲海洋控股在 EBIT 水平上沒有盈利,但設法將其收入增長了 22%,達到 236 億新加坡元。隨著任何運氣,該公司將能夠增長自己的方式盈利能力。

警告需要注意的事項

儘管增長最高,亞洲海洋控股在過去一年仍錄得除利息稅前盈利(EBIT)虧損。事實上,它在 EBIT 水平下損失了相當可觀的 16 億新加坡元。反思這一點和重要的總負債,由於我們對股票的強烈不親和力,很難知道該說些什麼。當然,該公司可能對他們如何走向更光明的未來有一個很好的故事。但現實情況是,它相對於負債的流動資產較低,去年損失了 32 億新元。因此,我們認為購買此股票有風險。我們更願意避免一家公司在其審計師對公司繼續擔憂的能力有任何不確定性之後。這是因為我們發現投資於始終保持資產負債表合理強大的公司更加舒適。在分析債務水平時,資產負債表是顯而易見的起點。但最終,每家公司都可能包含資產負債表之外存在的風險。請注意,亞洲海洋控股正在顯示 投資分析中的 2 個警告標誌 ,其中 1 個潛在是嚴重的...

畢竟,如果您對擁有堅如磐石的資產負債表的快速發展公司更感興趣,那麼請立即查看我們的淨現金增長股票清單。

對這篇文章有反饋嗎?關注內容? 取得聯繫 直接與我們聯繫。 或者,通過電子郵件發送電子郵件給編輯團隊。

這篇文章由簡單牆聖是一般性質. 我們僅使用公正的方法,根據歷史數據和分析師預測提供評論,我們的文章並不打算作為財務建議。 它並不構成購買或出售任何股票的建議,也不會考慮您的目標或您的財務狀況。我們的目標是為您帶來由基本數據驅動的長期集中分析。請注意,我們的分析可能不會考慮最新的價格敏感公司公告或定性材料。簡易華街在提及的任何股票中都沒有倉位。