In addition to the debate over the extent of the rate hike, this time the market will also pay attention to the policy direction after the meeting, such as the duration of the interest rate hike cycle. Most big banks expect the federal funds rate to peak at 4 per cent between the end of this year and next year, while the market expects it to reach 4.5 per cent.

Interest rate hikes of at least 75 basis points are "stable", and the market is waiting for another key signal-when the Fed will release its eagle.

At 14:00 EDT on Wednesday (02:00 Beijing time on Thursday), the Fed's FOMC will release interest rate decisions, policy statements and economic forecasts. Subsequently, Federal Reserve Chairman Powell will hold a press conference on monetary policy.

So far, CME's Fed Watch tool shows that the probability of the market expecting the Fed to raise interest rates by 75 basis points at this meeting is 82 per cent, while the probability of raising interest rates by 100bp is only 18 per cent.

In addition to the rate hike, the market is also very concerned about the bitmap and economic outlook released by the Federal Reserve after the meeting.Compared with the recent market controversy of "raising interest rates by 75 basis points or 100 basis points", this part is related to the Fed's later process of raising interest rates and may have a greater impact on the market.

At present, most institutions' expectations for the peak federal funds rate between the end of this year and next year fluctuate in the range of 4 per cent, while market expectations are generally high, which could reach 4.5 per cent in March next year.

As for the follow-up interest rate policy, analysts believe that if economic data show that inflation falls towards the target level next year, it is expected that the FOMC will finally end the interest rate hike cycle. But if the economy does not show substantial weakness, the Fed is likely to continue to tighten policy until 2023.

75bp vs 100bp?

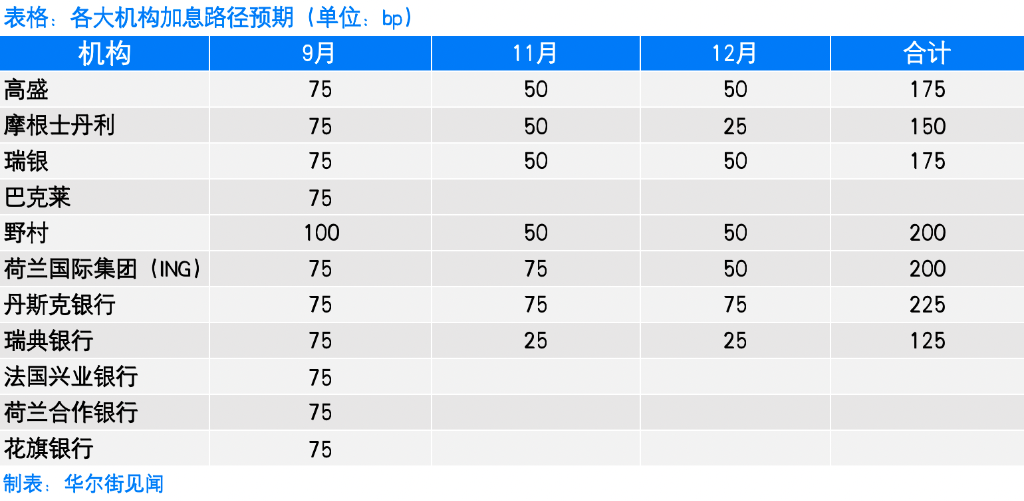

A number of Wall Street banks, including JPMorgan Chase & Co, Morgan Stanley, UBS, Goldman Sachs Group and Barclays, expect the Fed to raise interest rates by 75 basis points at the meeting, which is almost certain and unlikely.

While a key part of core inflation accelerated in August, Morgan Stanley believes inflation is far from where the Fed needs to act so aggressively.Raising interest rates at such a rapid pace in history increases the risk that the Fed is moving too fast. The total accumulation of past actions will have a lag effect.

But Nomura was the first to raise interest rates by 100bp after the August CPI data were released. Nomura analysts give three reasons:

First, the inflation trend has not improved.It will do little good to increase interest rates in the more distant future, raising the risk that inflation will become more entrenched

Second, although the Fed has taken tightening measures, financial conditions have not tightened significantly.Combined with the recent development of inflation, more participants may be inclined to raise interest rates by 100 basis points-higher than current market pricing-to tighten the financial environment more significantly.

Third, raising interest rates by 100 basis points will make the Fed's policy interest rate steadily higher than this level, increase the possibility of interest rates entering a restricted range, and exert obvious downward pressure on inflation.

Steven Blitz, chief US economist at T.S. Lombard, believes that this will also give Fed officials some policy flexibility, with the mid-term congressional elections still a week away.Inflation is a central topic in this election.

The follow-up interest rate hike cycle of the Federal Reserve deserves more attention.

HSBC pointed out in a report last week that if the Fed had only about 150 basis points to raise interest rates in the future, it would make little difference whether a single rate increase would be 50 basis points or 100 basis points, as it would take two or three more meetings to peak interest rates.By implication, what is more noteworthy now is the bitmap released by the Federal Reserve after the meeting and the forecast for the peak of interest rates.

For investors who focus on long-term market trends, this part is related to the cumulative extent and duration of the Fed's interest rate hikes, which will have a greater impact on the market.

UBS also thinksThis time Fed officials will pay more attention to the direction of policy after the meeting.FOMC members will also discuss whether the pace of interest rate hikes and the contraction in the balance sheet are sufficient to restore inflation to their target of 2.0 per cent within their forecast period. That means they also have to discuss the actions at the November and December meetings, the effectiveness of monetary policy, and where the federal funds rate peaked.

The market expects interest rates to peak at 4.5%

The massive rate hike will bring the Fed's policy interest rate to a range of 3% to 3.25%, which Fed officials believe will begin to enter a restrictive range, curbing economic growth.

At present, most institutions' expectations for the peak federal funds rate fluctuate within the range of 4 per cent, while market expectations are generally high, which could reach 4.5 per cent in March next year.

Morgan Stanley believes that the current risk is that interest rates are higher, the pace of raising interest rates is slower, and the pace of raising interest rates is more inclined to slow down. The Fed is expected to raise interest rates by 50 basis points in November and 25 basis points in December, bringing the federal funds rate to 3.875 per cent by the end of the year, peaking at 4.1 per cent at the end of 2023 and cutting rates by 25 basis points twice in 2024.

UBS believes the Fed will raise interest rates by another 50 basis points in November and December, for a total of 175 basis points this year. The FOMC is likely to discuss suspending interest rate hikes early next year for three reasons:First,Core CPI will decline significantly in the fourth quarter of this year.Second,The labor market is expected to really slow down by the end of this year.Third,The base effect will depress year-on-year price increases more significantly.

UBS said that against a backdrop of relatively weak economic growth and a marked slowdown in labour market expansion, the FOMC was likely to maintain a restrictive policy stance, but would relax slightly in line with the progress of inflation. As a result, the target range of interest rates is expected to be 4% Murray 4.25% by the end of this year, and the US economy will contract in the fourth quarter of this year.

Later next year, FOMC may consider lowering its target range and cutting interest rates by 75 basis points, keeping the target range at 3.25% Mel 3.5% by the end of 2023. This is still within the restricted range, even though the FOMC has made significant progress in reducing inflation.

UBS expects participants' expectations for "appropriate interest rates" to fall to 2.9 per cent and close to longer-term expectations in 2025.

According to Barclays, the federal funds rate peaked at 4.25 per cent at the end of the year (indicating that the rate increase in November was still 50 or 75 basis points) and then remained stable in 2023.

Goldman Sachs Group expects the Fed's pace of rate hikes to slow to 50 basis points in November and December, reaching 4.25 per cent at the end of the year and then peaking at 4.25 per cent in 2023.Restrictive policies will last until 2025.

Goldman Sachs Group also said that if interest rates peak above 4.5% in 2023, it will deal a serious blow to the stock market.

According to Nomura, interest rates will be raised by another 50 basis points in November and December and another 25 basis points in February 2023, pushing the key interest rate to a range of 4.50-4.75%. After four consecutive quarters of economic contraction, inflation and the labour market are clearly under pressure, and interest rates are expected to be cut by 25 basis points per FOMC meeting starting in September 2023.

Nomura expects the new bitmap to show median interest rates of 4.125%, 4.625% and 3.875% for 2022-2024, respectively, a significant increase from previous forecasts.A range of interest rates above market pricing helps to tighten financial conditions and conveys the Fed's confidence in restoring price stability.

But market expectations for the end point of the Fed's rate hike have been raised. At present, the market expects that the federal funds rate will reach a range of 4.25% by the end of this year, 4.25% by February 2023, and 4.50% by February, and may reach 4.50% by 4.75%, close to the level at the end of 2007 on the eve of the financial crisis.Some people expect even higher, thinking that the peak will be around 5%.

When will the interest rate hike cycle end?

UBS said there were clear upside risks in its forecasts for peak interest rates and the length of the tightening cycle, and believed that the Fed would consider extending the tightening cycle and raising interest rate peaks at this meeting.If the real economy does not show more substantial weakness, the Fed is likely to continue to tighten policy until 2023.

Barclays believes that there are reliable signs that inflation will move towards the 2% target next year, job growth is also slowing, and FOMC is expected to suspend interest rate hikes and eventually end the interest rate hike cycle.The federal funds rate was gradually cut in the third quarter of 2023.

But the end of the rate hike cycle remains highly dependent on inflation and employment data, and there are considerable upside risks to Barclays' forecasts, especially if inflation continues to be higher than expected or labour demand does not slow. Interest rates are likely to rise again. The risk of recession caused by this process will still be very serious.

More important than specific policy actions is the pace of interest rate hikes. Morgan Stanley expects Powell to reiterate the view that "it is appropriate to slow down the rate increase at some point". But it seems inappropriate to mention directly the conditions needed to start slowing the pace of rate hikes, and if this is included, it will undoubtedly increase the market's bet on a 50 basis point rate hike in November.

Nomura believes that policy makers will not imply that interest rates will be cut before 2024, and that once they start, the pace of interest rate cuts is likely to be gradual, in line with Powell's remarks at the Jackson Hole conference. That is, "historical experience strongly warns us not to loosen policy prematurely."

Barclays also said that as the interest rate hike cycle draws to a close, the Fed's reference to "sustained interest rate hikes" could become "additional interest rate hikes".The focus of the wording will shift from a sharp interest rate hike in the previous period to figuring out an appropriate restrictive policy position.

Inflation is still above all else.

Economists believe that because of the unexpectedly strong CPI data in August, Powell will be tough on inflation at the news conference, which could be interpreted by the market as a rather hawkish signal.

Nomura predicts that the recent fall in commodity prices may put pressure on the Fed's PCE inflation forecast, but better-than-expected August CPI data suggestCore PCE inflation is likely to be revised up to 4.4 per cent in 2022.

Mr Powell's speech is likely to continue to focus on the difficulty of the current task of fighting inflation, further highlighting the possibility of interest rates exceeding 4 per cent and the Fed's single focus on achieving inflation above all else.

When discussing when the Fed might withdraw from tightening policy, Federal Reserve Governor Waller said this month:

I was "burned" by inflation last year. We are very careful not to get hurt again.

Inflation must achieve a real, permanent, long-term decline.

Waller also said wage growth was unlikely to slow without significant weakness in the labour market. The Fed will not have a trade-off between inflation and employment until the unemployment rate rises above 5 per cent. This poses a certain upside risk to the median forecast of unemployment.

Edit / phoebe