A Closer Look At Kinder Morgan, Inc.'s (NYSE:KMI) Uninspiring ROE

A Closer Look At Kinder Morgan, Inc.'s (NYSE:KMI) Uninspiring ROE

Many investors are still learning about the various metrics that can be useful when analysing a stock. This article is for those who would like to learn about Return On Equity (ROE). By way of learning-by-doing, we'll look at ROE to gain a better understanding of Kinder Morgan, Inc. (NYSE:KMI).

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. Simply put, it is used to assess the profitability of a company in relation to its equity capital.

See our latest analysis for Kinder Morgan

How Do You Calculate Return On Equity?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Kinder Morgan is:

7.9% = US$2.5b ÷ US$32b (Based on the trailing twelve months to June 2022).

The 'return' is the yearly profit. Another way to think of that is that for every $1 worth of equity, the company was able to earn $0.08 in profit.

Does Kinder Morgan Have A Good ROE?

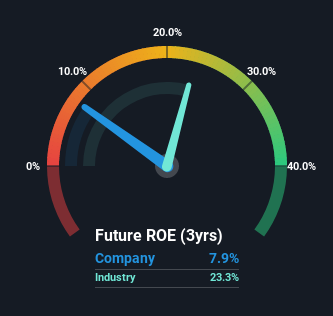

Arguably the easiest way to assess company's ROE is to compare it with the average in its industry. However, this method is only useful as a rough check, because companies do differ quite a bit within the same industry classification. As is clear from the image below, Kinder Morgan has a lower ROE than the average (23%) in the Oil and Gas industry.

NYSE:KMI Return on Equity August 4th 2022

NYSE:KMI Return on Equity August 4th 2022That certainly isn't ideal. That being said, a low ROE is not always a bad thing, especially if the company has low leverage as this still leaves room for improvement if the company were to take on more debt. A company with high debt levels and low ROE is a combination we like to avoid given the risk involved. You can see the 3 risks we have identified for Kinder Morgan by visiting our risks dashboard for free on our platform here.

How Does Debt Impact Return On Equity?

Most companies need money -- from somewhere -- to grow their profits. That cash can come from issuing shares, retained earnings, or debt. In the first two cases, the ROE will capture this use of capital to grow. In the latter case, the use of debt will improve the returns, but will not change the equity. That will make the ROE look better than if no debt was used.

Kinder Morgan's Debt And Its 7.9% ROE

It's worth noting the high use of debt by Kinder Morgan, leading to its debt to equity ratio of 1.00. The combination of a rather low ROE and significant use of debt is not particularly appealing. Debt increases risk and reduces options for the company in the future, so you generally want to see some good returns from using it.

Conclusion

Return on equity is a useful indicator of the ability of a business to generate profits and return them to shareholders. A company that can achieve a high return on equity without debt could be considered a high quality business. If two companies have around the same level of debt to equity, and one has a higher ROE, I'd generally prefer the one with higher ROE.

But ROE is just one piece of a bigger puzzle, since high quality businesses often trade on high multiples of earnings. Profit growth rates, versus the expectations reflected in the price of the stock, are a particularly important to consider. So you might want to check this FREE visualization of analyst forecasts for the company.

Of course Kinder Morgan may not be the best stock to buy. So you may wish to see this free collection of other companies that have high ROE and low debt.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

许多投资者仍在学习在分析股票时可能有用的各种指标。这篇文章是为那些想了解股本回报率(ROE)的人准备的。通过边做边学的方式,我们将关注净资产收益率,以更好地了解Kinder Morgan,Inc.(纽约证券交易所代码:KMI)。

股本回报率或净资产收益率是股东要考虑的一个重要因素,因为它告诉他们他们的资本再投资的效率。简而言之,它是用来评估一家公司相对于其权益资本的盈利能力。

查看我们对Kinder Morgan的最新分析

你如何计算股本回报率?

这个股本回报率公式是:

股本回报率=(持续经营的)净利润?股东权益

因此,根据上述公式,Kinder Morgan的净资产收益率为:

7.9%=25亿美元×320亿美元(基于截至2022年6月的12个月)。

“回报”就是年度利润。另一种想法是,每价值1美元的股本,公司就能够赚取0.08美元的利润。

金德摩根的净资产收益率好吗?

可以说,评估公司净资产收益率最简单的方法是将其与所在行业的平均水平进行比较。然而,这种方法只是作为一种粗略的检查,因为在同一行业分类中,公司确实有很大的不同。如下图所示,Kinder Morgan的净资产收益率(ROE)低于石油和天然气行业的平均水平(23%)。

纽约证券交易所:KMI股本回报率2022年8月4日这当然不是理想的情况。话虽如此,低ROE并不总是一件坏事,特别是如果公司的杠杆率较低,因为如果公司承担更多债务,这仍有改进的空间。考虑到涉及的风险,高债务水平和低ROE的公司是我们希望避免的组合。您可以访问我们为Kinder Morgan确定的3个风险风险控制面板在我们的平台上是免费的。

债务对股本回报率有何影响?

大多数公司都需要资金--从某个地方--来增加利润。这些现金可以来自发行股票、留存收益或债务。在前两种情况下,净资产收益率将抓住这种资本增长的用途。在后一种情况下,债务的使用将提高回报,但不会改变股权。这将使净资产收益率看起来比不使用债务的情况下更好。

金德摩根的债务及其7.9%的净资产收益率

值得注意的是,Kinder Morgan高度利用债务,导致其债务与股本比率为1.00。相当低的净资产收益率和大量使用债务的组合并不是特别有吸引力。债务增加了风险,减少了公司未来的选择,所以你通常希望看到使用它的一些良好回报。

结论

股本回报率是衡量一家企业产生利润并将其返还给股东的能力的有用指标。一家能够在没有债务的情况下实现高股本回报率的公司可以被认为是一家高质量的企业。如果两家公司的债务权益比大致相同,而其中一家公司的净资产收益率更高,我通常会更喜欢净资产收益率更高的那家公司。

但净资产收益率只是一个更大的谜题的一部分,因为高质量企业的市盈率往往很高。相对于股价反映的预期,利润增长率是一个特别重要的考虑因素。因此,你可能想查看分析师对该公司预测的免费可视化。

当然了金德摩根可能不是最值得买入的股票。所以你可能想看看这个免费其他拥有高ROE和低债务的公司的集合。

对这篇文章有什么反馈吗?担心内容吗? 保持联系直接与我们联系。或者,也可以给编辑组发电子邮件,地址是implywallst.com。

本文由Simply Wall St.撰写,具有概括性。我们仅使用不偏不倚的方法提供基于历史数据和分析师预测的评论,我们的文章并不打算作为财务建议。它不构成买卖任何股票的建议,也没有考虑你的目标或你的财务状况。我们的目标是为您带来由基本面数据驱动的长期重点分析。请注意,我们的分析可能不会将最新的对价格敏感的公司公告或定性材料考虑在内。Simply Wall St.对上述任何一只股票都没有持仓。

译文内容由第三方软件翻译。

风险及免责提示

- 分享到weixin

- 分享到qq

- 分享到facebook

- 分享到twitter

- 分享到微博

- 粘贴板

使用浏览器的分享功能,分享给你的好友吧