摘要:

宏观面,美联储11月大概率Taper,但预计对市场影响有限,主要焦点在于是否传递加息信号。关注11月4日美联储议息会议。国内方面,中国公布10月官方制造业PMI指数49.2,较9月下降0.4个百分点,连续两个月处于收缩区间。非制造业活动指数52.4,较9月下调0.8个百分点。经济数据下行印证前期担忧,能源紧张仍在加强,四季度经济放缓预期进一步加强,利空增加。

基本面,10月29日铜精矿TC报价62.84美元/吨,较9月30日的65.3美元/吨下降2.46美元/吨。9月以来TC回升放缓,主因近期南美铜矿端仍有扰动。国内精铜受限电扰动产量不及预期,需求疲软下,库存维持低位态势。铜价冲高回落,精废价差先扩大后收窄,因废铜货源并不充裕,整体替代效应有限。10月末最后一周,SHFE库存止跌回升,相较前一周增加9488吨至49327吨。LME挤仓虽有缓解,但现货升水仍处相对高位,进口窗口持续关闭,月内库存下降至140175吨,注销仓单占比78.9%,可利用库存约3万吨。整体内外库存变化的持续性仍有待关注。

观点及策略:进入11月后预计煤炭市场引发的负面情绪将逐步缓解,如果美联储议息会议无超预期扰动,铜价或将逐步企稳,供需双弱格局下,低库存对价格支撑仍有效,但价格向上驱动仍需进一步利多消息的指引。预计CU2112主要波动参考区间为69000-74000元/吨,操作上,仍以区间波段交易为主。

风险提示:海外能源危机继续发酵(上行风险);美联储议息会议偏鹰超市场预期(下行风险)。

一、行情回顾

10月国庆节后,因欧洲能源危机发酵及伦铜库存存在较大挤仓风险,铜价冲高至76000元/吨上方,随后LME修改交割规则致挤仓风险缓解,LME升水从1103.5美元/吨高点收窄至200美元/吨下方。临近10月末,国内对煤炭市场实施强有力的保供政策,市场恐慌情绪波及有色金属,铜价跟随下跌。月内LME铜最高10452.5美元/吨,最低8876.5美元/吨,目前运行9500美元/吨附近,月涨幅约7%。CU2112合约期价最高76550元/吨,最低68660元/吨,收盘70540元/吨,月涨幅4.01%。

图表1:沪铜2112合约价格走势

数据来源:文华财经、广州期货研究中心

二、基本面分析

(一)供应端情况

1.铜矿维持恢复态势

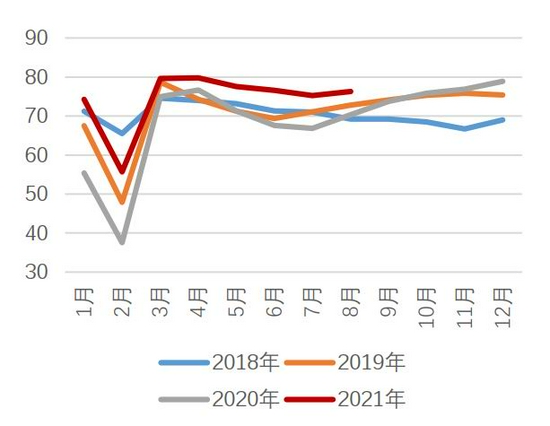

10月29日铜精矿TC报价62.84美元/吨,已经较今年3月30美元/吨有较大的回升,差不多接近疫情前水平。然9月以来TC回升放缓,主因近期南美铜矿端仍有扰动。

图表2:铜精矿现货TC上行节奏放缓

数据来源:SMM、广州期货研究中心

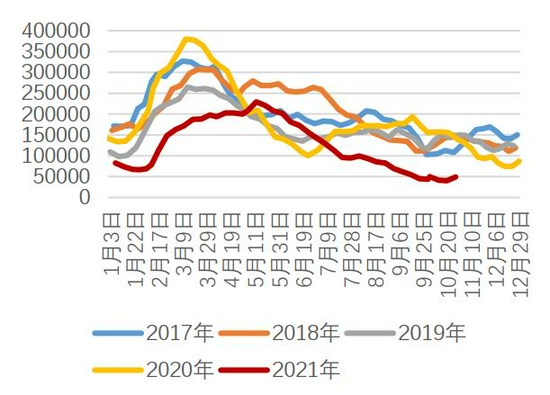

图表3:铜矿进口环比持续回升

数据来源:SMM、广州期货研究中心

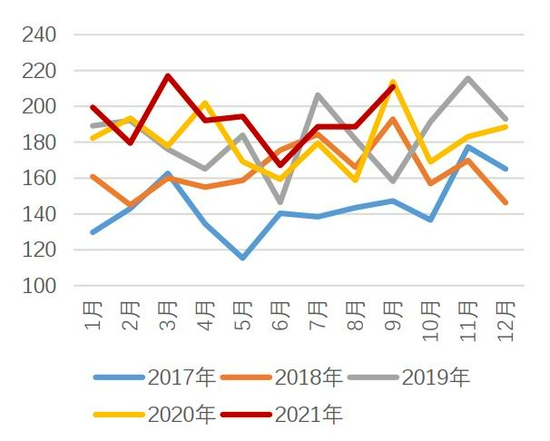

铜矿石及精矿,2021年9月铜矿砂及其精矿进口211.09万吨,环比+11.9%,同比-1.3%18.86%;1-9月累计进口1736.94万吨,累计同比+6.2%。

国际铜研究组织(ICSG)的数据显示,2021年7月世界精炼铜短缺3.1万吨,6月为短缺9.8万吨。2021年1-7月精炼铜产量为1436.1万吨,去年同期为1399.4万吨。2021年7月精炼铜产量为207.3万吨,去年同期为202.7万吨。

2.国内精炼产量有望回升

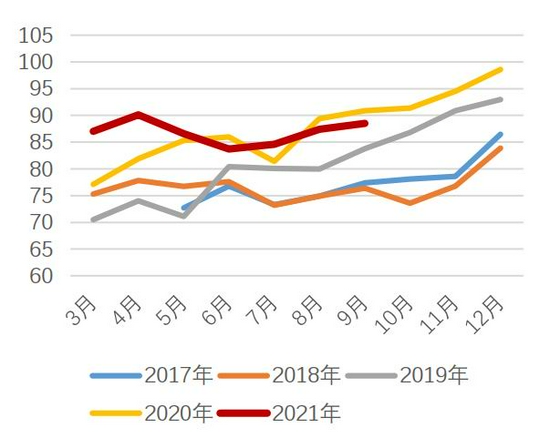

9月统计局公布中国电解铜产量为88.5万吨,环比+1.3%,同比+2.4%。二三季度国内铜冶炼企业受限电限产影响,大多提前安排检修,精铜产量明显受到抑制。据SMM调研显示,9月冶炼厂逐步结束检修,且TC的回升及硫酸价格维持1000附近的高位,增厚炼厂利润,如果没有更严格的限产压力,预计四季度精铜产量有望环比回升。

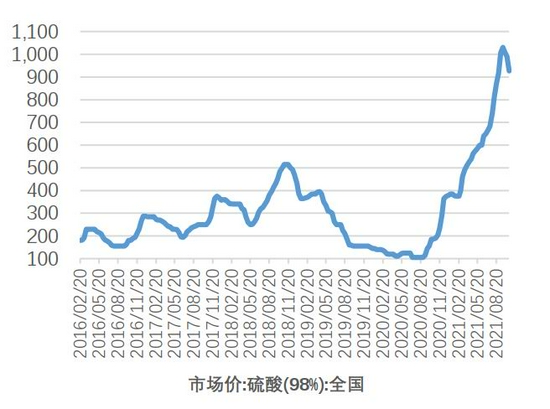

截至10月20日,全国硫酸(98%)市场价926.3元/吨,较9月高点1031元/吨下调104.7元/吨。据SMM了解,由于华东地区持续受到限电影响,当地化工企业被迫减产已致硫酸需求骤降,铜陵有色旗下金冠及金隆铜业由于担心潜在的硫酸胀库风险,决定开始降低铜冶炼投矿量,暂时预计降影响20%投矿量。目前硫酸价格在传统淡季,且需求端受到较大限电扰动下逐渐高位回落。

2022年Codelco发往欧洲铜长单溢价为128美元/吨,较2021年98美元/吨增长30美元/吨,其增幅高达30%;预计发往中国长单溢价为118美元/吨。自2008年以来,Codelco发往中国铜长单溢价最高138美元/吨,发生在2014年。反应市场对明年精铜供应存偏紧预期。

图表4:精炼铜产量有望回升

数据来源:Wind、广州期货研究中心

图表5:硫酸价格高位小幅回落

数据来源:Wind、广州期货研究中心

3.废铜供应偏紧未有明显改善

精铜,9月进口量约为26万吨,同比减少50%;1-8月累计进口量258.2万吨,同比减少27.5%。

废铜,9月进口13.4万吨,同比增加68.3%,环比增加3.6%。2021年1-9月份累计进口量为123.4万吨,同比增长85.1%。

从废铜进口量来看,虽然今年中国废铜进口量虽然同比大增超过80%,但是国内再生铜制杆产能迅速扩张,废铜原料供应仍然存在较大缺口,无论是进口还是国内回收的再生铜原料供应,均较难在短期内大幅增加以满足需求。6月马来西亚因疫情再度封锁更是加重了废铜紧张的局面,精废价差一度倒挂;如今马来西亚有所好转,但进口政策又要收紧。根据最新修订的进口指南,所有经过检查和批准的废金属进口都要求达到94.75%的最低金属含量。

根据2020年11月1日起实施的中国再生铜原料新标准细则来看,再生铜原料铜含量最低不小于97%,再生黄铜原料黄铜含量最低不小于95%,马来西亚进口新标准在某些方面已经和中国相仿。

马来西亚拆解的废铜多数来源于海外,短时间内,如果马来西亚从11月1日期开始实施进口废铜新政策,可能导致马来西亚废铜进口量的下降,进而出口到中国的废铜量会减少,对我国的废铜供应端构成冲击。9月我们对江西鹰潭的几家废铜制杆企业进行实地考察,企业反应未来马来西亚的大部分拆解工厂大概率转移到印度,但受疫情影响可能需要比较长的过渡时间,废铜进口货源依旧会维持较长时间的偏紧状态。

图表6:精铜进口量依然偏低

数据来源:Wind、广州期货研究中心

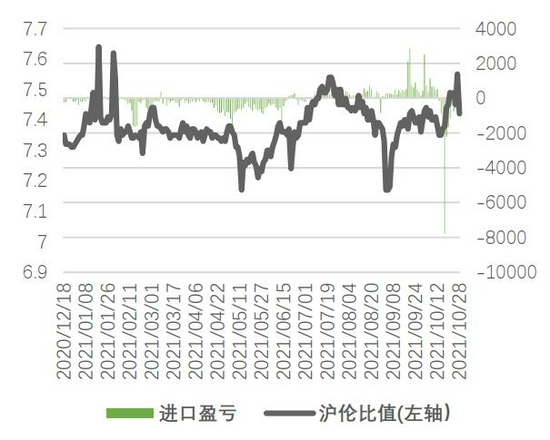

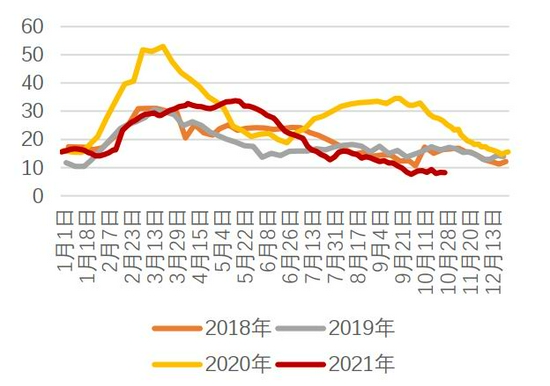

图表7:精铜进口维持亏损

数据来源:Wind、广州期货研究中心

图表8:废铜进口货源偏紧

数据来源:Wind、广州期货研究中心

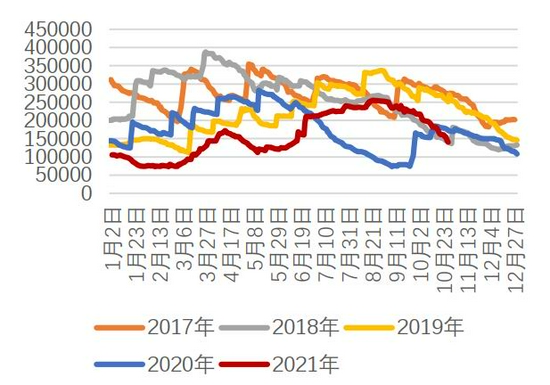

图表9:精废价差明显扩大

数据来源:Wind、广州期货研究中心

(二)消费端情况

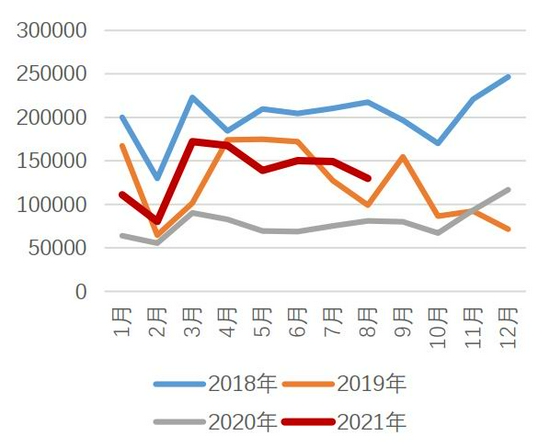

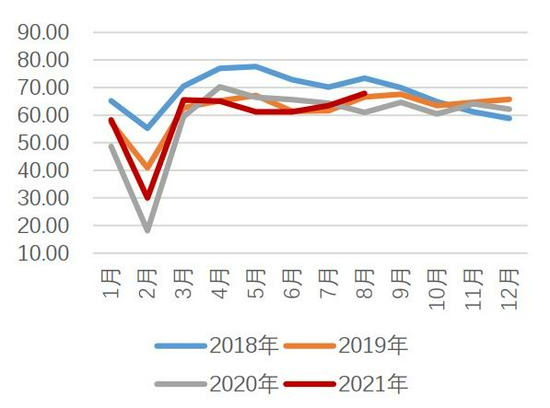

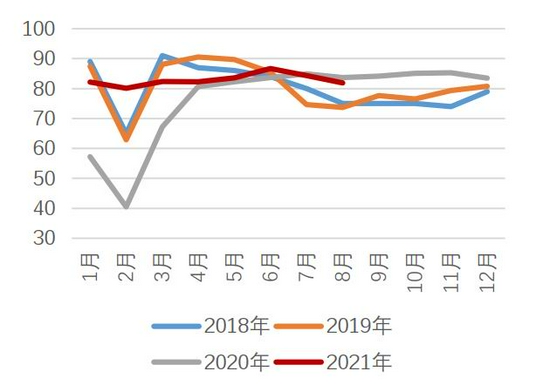

Mysteel数据显示,9月铜杆企业开工率为64.43%,环比减少3.42%;铜板带企业开工率为78.1%,环比增加1.84%。铜管企业开工率为75.87%,环比下降6%。

基差方面,随着国内库存持续下滑,市场可流通货源减少,现货偏紧致升水(现货价-期货主力合约)高企,隔月价差扩大至400元高位。

图表10:铜杆企业开工率

数据来源:Mysteel、广州期货研究中心

图表11:铜管企业开工率

数据来源:Mysteel、广州期货研究中心

图表12:铜板带企业开工率

数据来源:Mysteel、广州期货研究中心

图表13:基差维持较高升水结构

数据来源:Mysteel、广州期货研究中心

(三)库存情况

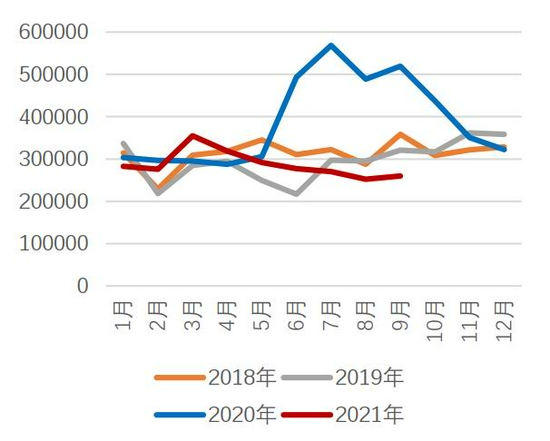

首先我们看国内库存,无论是交易所库存还是社库从5月以来一直保持回落趋势,目前已降绝对低位水平,截至10月29日,两者之和约13.1万吨,以中国一年消费量约1250万吨来计算,每天大概消费3.5万吨,目前国内库存可消费3.74天。

境外库存来看,上海保税区库存从7月初的44万吨附近快速下滑,至目前的20万吨附近,降幅超50%,这与7月以来国内产量受限,废铜偏紧导致精铜替代消费、进口盈利窗口打开有关,使得保税区库存大量流入国内。LME库存至9月以来也开始转为下降,目前为14万吨,较9月高点25万吨,降幅44%。我们把三大交易所+上海保税区+国内社库都算进去,总的库存量约51.9万吨,按全球一年消费量2503万吨计算,可消费天数大概是7.5天。

值得关注的是,进入10月后,LME铜的注销仓单占比快速拉升,致可利用库存持续降低,周中LME注销仓单比超90%,导致LME铜可用库存不到2万吨,挤仓风险推升现货升水至1000美元上方的绝对历史高位。随后,LME对铜交易进行调查,并实施现货溢价限制和延期交割机制。LME铜的Back结构有所收缩,10月28日LME0-3最近报价189美元/吨。

图表14:上期所库存环比继续下滑

数据来源:Wind、广州期货研究中心

图表15:国内主流地区现货库存环比继续下滑

数据来源:Wind、广州期货研究中心

图表16:LME铜库存持续明显下滑

数据来源:Wind、广州期货研究中心

图表17:LME铜可利用库存

数据来源:Wind、广州期货研究中心

图表18:LME+COMEX+SHFE+上海保税区库存合计

数据来源:Wind、广州期货研究中心

图表19:全球整体库存消费比绝对低位

数据来源:Wind、广州期货研究中心

三、投资建议

进入11月后预计煤炭市场引发的负面情绪将逐步缓解,如果美联储议息会议无超预期扰动,铜价或将逐步企稳,供需双弱格局下,低库存对价格支撑仍有效,但价格向上驱动仍需进一步利多消息的指引。预计CU2112主要波动参考区间为69000-74000元/吨,操作上,仍以区间波段交易为主。

风险提示:海外能源危机继续发酵(上行风险);美联储议息会议偏鹰超市场预期(下行风险)。

广州期货 许克元

摘要:

宏觀面,美聯儲11月大概率Taper,但預計對市場影響有限,主要焦點在於是否傳遞加息信號。關注11月4日美聯儲議息會議。國內方面,中國公佈10月官方製造業PMI指數49.2,較9月下降0.4個百分點,連續兩個月處於收縮區間。非製造業活動指數52.4,較9月下調0.8個百分點。經濟數據下行印證前期擔憂,能源緊張仍在加強,四季度經濟放緩預期進一步加強,利空增加。

基本面,10月29日銅精礦TC報價62.84美元/噸,較9月30日的65.3美元/噸下降2.46美元/噸。9月以來TC回升放緩,主因近期南美銅礦端仍有擾動。國內精銅受限電擾動產量不及預期,需求疲軟下,庫存維持低位態勢。銅價衝高回落,精廢價差先擴大後收窄,因廢銅貨源並不充裕,整體替代效應有限。10月末最後一週,SHFE庫存止跌回升,相較前一週增加9488噸至49327噸。LME擠倉雖有緩解,但現貨升水仍處相對高位,進口窗口持續關閉,月內庫存下降至140175噸,註銷倉單佔比78.9%,可利用庫存約3萬噸。整體內外庫存變化的持續性仍有待關注。

觀點及策略:進入11月後預計煤炭市場引發的負面情緒將逐步緩解,如果美聯儲議息會議無超預期擾動,銅價或將逐步企穩,供需雙弱格局下,低庫存對價格支撐仍有效,但價格向上驅動仍需進一步利多消息的指引。預計CU2112主要波動參考區間為69000-74000元/噸,操作上,仍以區間波段交易為主。

風險提示:海外能源危機繼續發酵(上行風險);美聯儲議息會議偏鷹超市場預期(下行風險)。

一、行情回顧

10月國慶節後,因歐洲能源危機發酵及倫銅庫存存在較大擠倉風險,銅價衝高至76000元/噸上方,隨後LME修改交割規則致擠倉風險緩解,LME升水從1103.5美元/噸高點收窄至200美元/噸下方。臨近10月末,國內對煤炭市場實施強有力的保供政策,市場恐慌情緒波及有色金屬,銅價跟隨下跌。月內LME銅最高10452.5美元/噸,最低8876.5美元/噸,目前運行9500美元/噸附近,月漲幅約7%。CU2112合約期價最高76550元/噸,最低68660元/噸,收盤70540元/噸,月漲幅4.01%。

圖表1:滬銅2112合約價格走勢

數據來源:文華財經、廣州期貨研究中心

二、基本面分析

(一)供應端情況

1.銅礦維持恢復態勢

10月29日銅精礦TC報價62.84美元/噸,已經較今年3月30美元/噸有較大的回升,差不多接近疫情前水平。然9月以來TC回升放緩,主因近期南美銅礦端仍有擾動。

圖表2:銅精礦現貨TC上行節奏放緩

數據來源:SMM、廣州期貨研究中心

圖表3:銅礦進口環比持續回升

數據來源:SMM、廣州期貨研究中心

銅礦石及精礦,2021年9月銅礦砂及其精礦進口211.09萬噸,環比+11.9%,同比-1.3%18.86%;1-9月累計進口1736.94萬噸,累計同比+6.2%。

國際銅研究組織(ICSG)的數據顯示,2021年7月世界精煉銅短缺3.1萬噸,6月為短缺9.8萬噸。2021年1-7月精煉銅產量為1436.1萬噸,去年同期為1399.4萬噸。2021年7月精煉銅產量為207.3萬噸,去年同期為202.7萬噸。

2.國內精煉產量有望回升

9月統計局公佈中國電解銅產量為88.5萬噸,環比+1.3%,同比+2.4%。二三季度國內銅冶煉企業受限電限產影響,大多提前安排檢修,精銅產量明顯受到抑制。據SMM調研顯示,9月冶煉廠逐步結束檢修,且TC的回升及硫酸價格維持1000附近的高位,增厚煉廠利潤,如果沒有更嚴格的限產壓力,預計四季度精銅產量有望環比回升。

截至10月20日,全國硫酸(98%)市場價926.3元/噸,較9月高點1031元/噸下調104.7元/噸。據SMM瞭解,由於華東地區持續受到限電影響,當地化工企業被迫減產已致硫酸需求驟降,銅陵有色旗下金冠及金隆銅業由於擔心潛在的硫酸脹庫風險,決定開始降低銅冶煉投礦量,暫時預計降影響20%投礦量。目前硫酸價格在傳統淡季,且需求端受到較大限電擾動下逐漸高位回落。

2022年Codelco發往歐洲銅長單溢價為128美元/噸,較2021年98美元/噸增長30美元/噸,其增幅高達30%;預計發往中國長單溢價為118美元/噸。自2008年以來,Codelco發往中國銅長單溢價最高138美元/噸,發生在2014年。反應市場對明年精銅供應存偏緊預期。

圖表4:精煉銅產量有望回升

數據來源:Wind、廣州期貨研究中心

圖表5:硫酸價格高位小幅回落

數據來源:Wind、廣州期貨研究中心

3.廢銅供應偏緊未有明顯改善

精銅,9月進口量約為26萬噸,同比減少50%;1-8月累計進口量258.2萬噸,同比減少27.5%。

廢銅,9月進口13.4萬噸,同比增加68.3%,環比增加3.6%。2021年1-9月份累計進口量為123.4萬噸,同比增長85.1%。

從廢銅進口量來看,雖然今年中國廢銅進口量雖然同比大增超過80%,但是國內再生銅製杆產能迅速擴張,廢銅原料供應仍然存在較大缺口,無論是進口還是國內回收的再生銅原料供應,均較難在短期內大幅增加以滿足需求。6月馬來西亞因疫情再度封鎖更是加重了廢銅緊張的局面,精廢價差一度倒掛;如今馬來西亞有所好轉,但進口政策又要收緊。根據最新修訂的進口指南,所有經過檢查和批准的廢金屬進口都要求達到94.75%的最低金屬含量。

根據2020年11月1日起實施的中國再生銅原料新標準細則來看,再生銅原料銅含量最低不小於97%,再生黃銅原料黃銅含量最低不小於95%,馬來西亞進口新標準在某些方面已經和中國相仿。

馬來西亞拆解的廢銅多數來源於海外,短時間內,如果馬來西亞從11月1日期開始實施進口廢銅新政策,可能導致馬來西亞廢銅進口量的下降,進而出口到中國的廢銅量會減少,對我國的廢銅供應端構成衝擊。9月我們對江西鷹潭的幾家廢銅製杆企業進行實地考察,企業反應未來馬來西亞的大部分拆解工廠大概率轉移到印度,但受疫情影響可能需要比較長的過渡時間,廢銅進口貨源依舊會維持較長時間的偏緊狀態。

圖表6:精銅進口量依然偏低

數據來源:Wind、廣州期貨研究中心

圖表7:精銅進口維持虧損

數據來源:Wind、廣州期貨研究中心

圖表8:廢銅進口貨源偏緊

數據來源:Wind、廣州期貨研究中心

圖表9:精廢價差明顯擴大

數據來源:Wind、廣州期貨研究中心

(二)消費端情況

Mysteel數據顯示,9月銅杆企業開工率為64.43%,環比減少3.42%;銅板帶企業開工率為78.1%,環比增加1.84%。銅管企業開工率為75.87%,環比下降6%。

基差方面,隨着國內庫存持續下滑,市場可流通貨源減少,現貨偏緊緻升水(現貨價-期貨主力合約)高企,隔月價差擴大至400元高位。

圖表10:銅杆企業開工率

數據來源:Mysteel、廣州期貨研究中心

圖表11:銅管企業開工率

數據來源:Mysteel、廣州期貨研究中心

圖表12:銅板帶企業開工率

數據來源:Mysteel、廣州期貨研究中心

圖表13:基差維持較高升水結構

數據來源:Mysteel、廣州期貨研究中心

(三)庫存情況

首先我們看國內庫存,無論是交易所庫存還是社庫從5月以來一直保持回落趨勢,目前已降絕對低位水平,截至10月29日,兩者之和約13.1萬噸,以中國一年消費量約1250萬噸來計算,每天大概消費3.5萬噸,目前國內庫存可消費3.74天。

境外庫存來看,上海保税區庫存從7月初的44萬噸附近快速下滑,至目前的20萬噸附近,降幅超50%,這與7月以來國內產量受限,廢銅偏緊導致精銅替代消費、進口盈利窗口打開有關,使得保税區庫存大量流入國內。LME庫存至9月以來也開始轉為下降,目前為14萬噸,較9月高點25萬噸,降幅44%。我們把三大交易所+上海保税區+國內社庫都算進去,總的庫存量約51.9萬噸,按全球一年消費量2503萬噸計算,可消費天數大概是7.5天。

值得關注的是,進入10月後,LME銅的註銷倉單佔比快速拉昇,致可利用庫存持續降低,週中LME註銷倉單比超90%,導致LME銅可用庫存不到2萬噸,擠倉風險推升現貨升水至1000美元上方的絕對歷史高位。隨後,LME對銅交易進行調查,並實施現貨溢價限制和延期交割機制。LME銅的Back結構有所收縮,10月28日LME0-3最近報價189美元/噸。

圖表14:上期所庫存環比繼續下滑

數據來源:Wind、廣州期貨研究中心

圖表15:國內主流地區現貨庫存環比繼續下滑

數據來源:Wind、廣州期貨研究中心

圖表16:LME銅庫存持續明顯下滑

數據來源:Wind、廣州期貨研究中心

圖表17:LME銅可利用庫存

數據來源:Wind、廣州期貨研究中心

圖表18:LME+COMEX+SHFE+上海保税區庫存合計

數據來源:Wind、廣州期貨研究中心

圖表19:全球整體庫存消費比絕對低位

數據來源:Wind、廣州期貨研究中心

三、投資建議

進入11月後預計煤炭市場引發的負面情緒將逐步緩解,如果美聯儲議息會議無超預期擾動,銅價或將逐步企穩,供需雙弱格局下,低庫存對價格支撐仍有效,但價格向上驅動仍需進一步利多消息的指引。預計CU2112主要波動參考區間為69000-74000元/噸,操作上,仍以區間波段交易為主。

風險提示:海外能源危機繼續發酵(上行風險);美聯儲議息會議偏鷹超市場預期(下行風險)。

廣州期貨 許克元