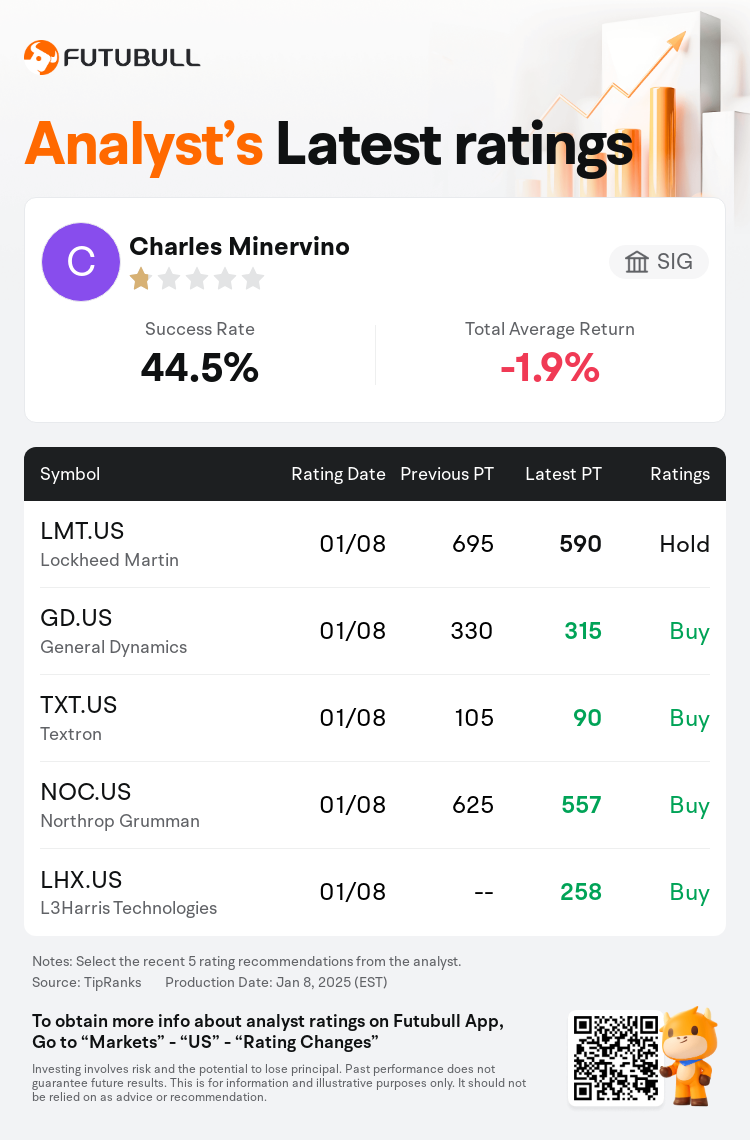

SIG analyst Charles Minervino downgrades $Lockheed Martin (LMT.US)$ to a hold rating, and adjusts the target price from $695 to $590.

According to TipRanks data, the analyst has a success rate of 44.5% and a total average return of -1.9% over the past year.

Furthermore, according to the comprehensive report, the opinions of $Lockheed Martin (LMT.US)$'s main analysts recently are as follows:

Furthermore, according to the comprehensive report, the opinions of $Lockheed Martin (LMT.US)$'s main analysts recently are as follows:

Barclays notes that aerospace is likely to generate positive relative earnings growth and anticipates further outperformance in 2025, with greater benefits leaning towards original equipment rather than aftermarket. On the defense side, performance has been weaker and the situation remains challenging, largely due to increased budget risks and uncertainties associated with government fiscal policies.

The outlook for commercial aerospace remains guarded, reflecting anticipated delays in the OEM build ramp, consistent with previous assessments. Discussions late in the fourth quarter support this perspective. In the defense sector, persistent concerns over funding and DOGE risk are expected to continue overshadowing the market, with the final quarter unlikely to provide significant clarity. There is potential for Lockheed Martin to pre-fund its 2025 pension obligations and/or proceed with the remaining MFC option exercise charges; both moves could be seen favorably. However, any increases in government services guidance may be tempered by the ongoing uncertainties related to the continuing resolution extension into March.

The revenue outlook for Defense and IT services is considered even-keeled and currently without optimistic drivers, according to an analyst discussing expectations for the Aerospace and Defense Electronics sector through 2025. In comparison, the commercial aerospace segment continues to be favored going into 2024, a stance that is anticipated to remain steady, with a particular focus on names heavily linked to the 2025 aftermarket.

Note:

TipRanks, an independent third party, provides analysis data from financial analysts and calculates the Average Returns and Success Rates of the analysts' recommendations. The information presented is not an investment recommendation and is intended for informational purposes only.

Success rate is the number of the analyst's successful ratings, divided by his/her total number of ratings over the past year. A successful rating is one based on if TipRanks' virtual portfolio earned a positive return from the stock. Total average return is the average rate of return that the TipRanks' virtual portfolio has earned over the past year. These portfolios are established based on the analyst's preliminary rating and are adjusted according to the changes in the rating.

TipRanks provides a ranking of each analyst up to 5 stars, which is representative of all recommendations from the analyst. An analyst's past performance is evaluated on a scale of 1 to 5 stars, with more stars indicating better performance. The star level is determined by his/her total success rate and average return.

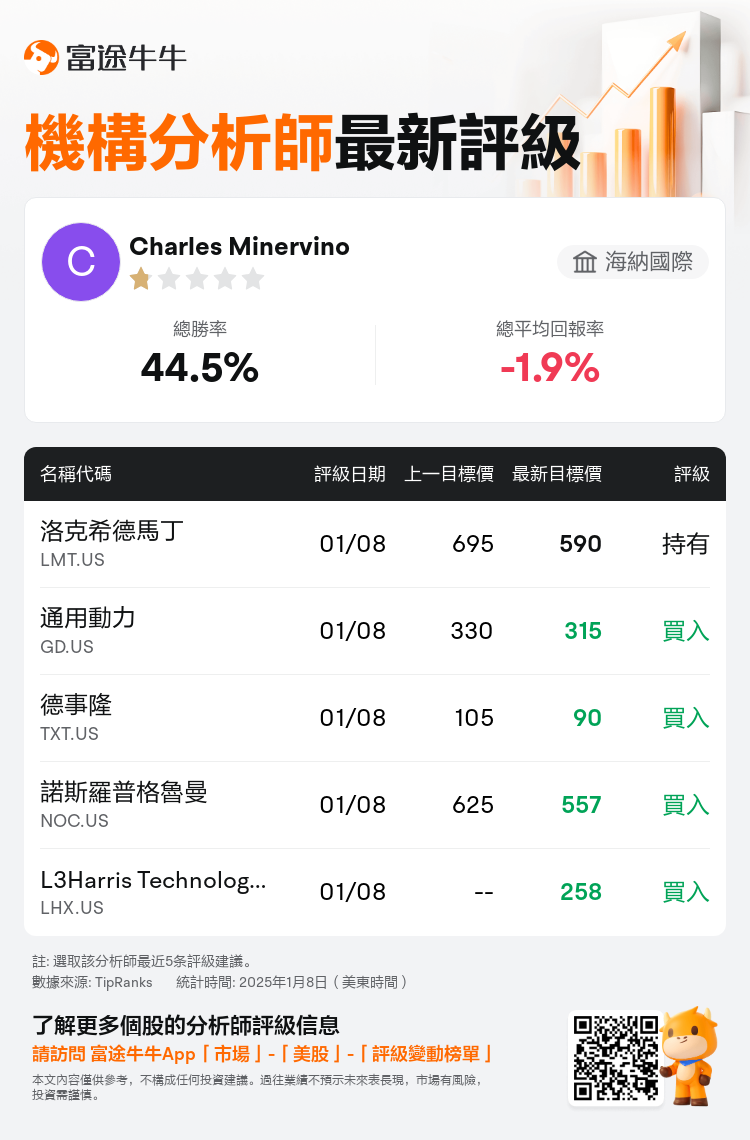

海納國際分析師Charles Minervino下調$洛克希德馬丁 (LMT.US)$至持有評級,並將目標價從695美元下調至590美元。

根據TipRanks數據顯示,該分析師近一年總勝率為44.5%,總平均回報率為-1.9%。

此外,綜合報道,$洛克希德馬丁 (LMT.US)$近期主要分析師觀點如下:

此外,綜合報道,$洛克希德馬丁 (LMT.US)$近期主要分析師觀點如下:

巴克萊指出,航空航天可能會帶來正的相對收益增長,並預計2025年將進一步跑贏大盤,更大的收益將傾向於原始設備而不是售後市場。在國防方面,表現一直疲軟,形勢仍然嚴峻,這主要是由於預算風險增加以及與政府財政政策相關的不確定性。

與先前的評估一致,商用航空航天的前景仍然保守,這反映了原始設備製造商建造階段的預期延遲。第四季度末的討論支持了這一觀點。在國防領域,對資金和DOGE風險的持續擔憂預計將繼續給市場蒙上陰影,最後一個季度不太可能提供明顯的明晰度。洛克希德·馬丁公司有可能爲其2025年的養老金義務預先注資和/或繼續支付剩餘的MFC期權行使費用;這兩項舉措都可能得到積極評價。但是,與決議持續延期至3月相關的持續不確定性可能會抑制政府服務指導方針的任何增加。

一位分析師在討論2025年之前航空航太和國防電子行業的預期時表示,國防和資訊技術服務的收入前景被認爲平穩,目前沒有樂觀的驅動因素。相比之下,到2024年,商用航空航天領域將繼續受到青睞,這一立場預計將保持穩定,特別關注與2025年售後市場密切相關的名稱。

提示:

TipRanks為獨立第三方,提供金融分析師的分析數據,並計算分析師推薦的平均回報率和勝率。提供的信息並非投資建議,僅供参考。本文不對評級數據和報告的完整性與準確性做出認可、聲明或保證。

TipRanks提供每位分析師的星級,分析師星級代表分析師所有推薦的過往表現,通過分析師的總勝率和平均回報率综合計算得出,星星越多,則該分析師過往表現越優異,最高爲5颗星。

分析師總勝率為近一年分析師的評級成功次數占總評級次數的比率。評级的成功與否,取決於TipRanks的虚擬投資組合是否從該股票中產生正回報。

總平均回報率為基於分析師的初始評級創建虚擬投資組合,並根據評級變化對組合進行調整,在近一年中該投資組合所獲得的回報率。