Those holding ImmunoPrecise Antibodies Ltd. (NASDAQ:IPA) shares would be relieved that the share price has rebounded 44% in the last thirty days, but it needs to keep going to repair the recent damage it has caused to investor portfolios. Still, the 30-day jump doesn't change the fact that longer term shareholders have seen their stock decimated by the 62% share price drop in the last twelve months.

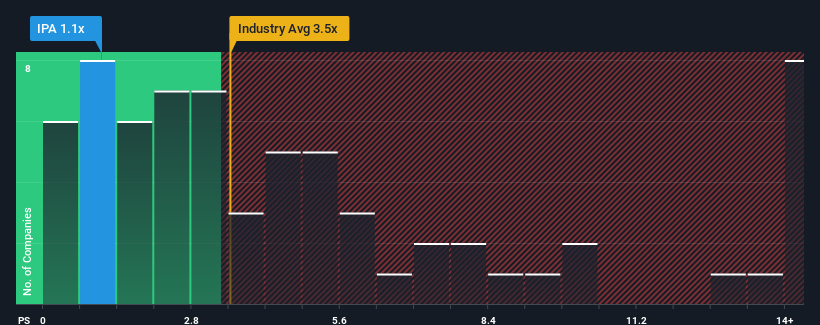

Although its price has surged higher, ImmunoPrecise Antibodies may still be sending very bullish signals at the moment with its price-to-sales (or "P/S") ratio of 1.1x, since almost half of all companies in the Life Sciences industry in the United States have P/S ratios greater than 3.6x and even P/S higher than 7x are not unusual. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so limited.

NasdaqGM:IPA Price to Sales Ratio vs Industry January 7th 2025

How Has ImmunoPrecise Antibodies Performed Recently?

ImmunoPrecise Antibodies certainly has been doing a good job lately as it's been growing revenue more than most other companies. Perhaps the market is expecting future revenue performance to dive, which has kept the P/S suppressed. If the company manages to stay the course, then investors should be rewarded with a share price that matches its revenue figures.

Want the full picture on analyst estimates for the company? Then our free report on ImmunoPrecise Antibodies will help you uncover what's on the horizon.

Do Revenue Forecasts Match The Low P/S Ratio?

There's an inherent assumption that a company should far underperform the industry for P/S ratios like ImmunoPrecise Antibodies' to be considered reasonable.

If we review the last year of revenue growth, the company posted a worthy increase of 6.4%. Revenue has also lifted 29% in aggregate from three years ago, partly thanks to the last 12 months of growth. Accordingly, shareholders would have probably been satisfied with the medium-term rates of revenue growth.

Turning to the outlook, the next three years should generate growth of 18% each year as estimated by the two analysts watching the company. That's shaping up to be materially higher than the 7.0% per annum growth forecast for the broader industry.

With this in consideration, we find it intriguing that ImmunoPrecise Antibodies' P/S sits behind most of its industry peers. It looks like most investors are not convinced at all that the company can achieve future growth expectations.

What Does ImmunoPrecise Antibodies' P/S Mean For Investors?

Shares in ImmunoPrecise Antibodies have risen appreciably however, its P/S is still subdued. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

ImmunoPrecise Antibodies' analyst forecasts revealed that its superior revenue outlook isn't contributing to its P/S anywhere near as much as we would have predicted. When we see strong growth forecasts like this, we can only assume potential risks are what might be placing significant pressure on the P/S ratio. At least price risks look to be very low, but investors seem to think future revenues could see a lot of volatility.

And what about other risks? Every company has them, and we've spotted 4 warning signs for ImmunoPrecise Antibodies (of which 1 is potentially serious!) you should know about.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

There's an inherent assumption that a company should far underperform the industry for P/S ratios like ImmunoPrecise Antibodies' to be considered reasonable.

There's an inherent assumption that a company should far underperform the industry for P/S ratios like ImmunoPrecise Antibodies' to be considered reasonable.

有一種固有的假設是,一個公司的表現應該遠低於行業,以便像ImmunoPrecise Antibodies這樣的市銷率才算合理。

有一種固有的假設是,一個公司的表現應該遠低於行業,以便像ImmunoPrecise Antibodies這樣的市銷率才算合理。