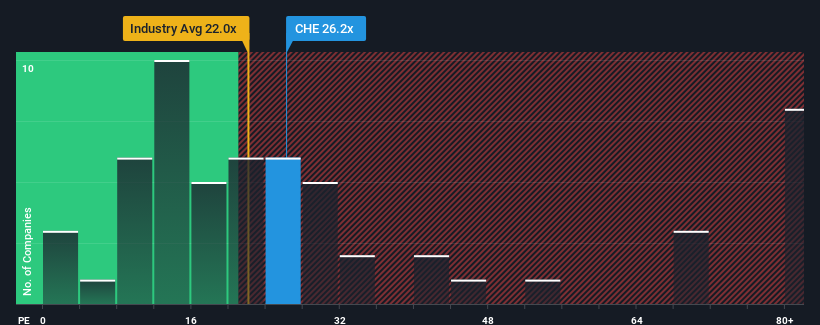

When close to half the companies in the United States have price-to-earnings ratios (or "P/E's") below 18x, you may consider Chemed Corporation (NYSE:CHE) as a stock to potentially avoid with its 26.2x P/E ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/E.

Chemed certainly has been doing a good job lately as it's been growing earnings more than most other companies. The P/E is probably high because investors think this strong earnings performance will continue. If not, then existing shareholders might be a little nervous about the viability of the share price.

NYSE:CHE Price to Earnings Ratio vs Industry January 2nd 2025 If you'd like to see what analysts are forecasting going forward, you should check out our free report on Chemed.

Is There Enough Growth For Chemed?

The only time you'd be truly comfortable seeing a P/E as high as Chemed's is when the company's growth is on track to outshine the market.

Retrospectively, the last year delivered an exceptional 23% gain to the company's bottom line. Still, EPS has barely risen at all from three years ago in total, which is not ideal. Accordingly, shareholders probably wouldn't have been overly satisfied with the unstable medium-term growth rates.

Shifting to the future, estimates from the three analysts covering the company suggest earnings should grow by 11% over the next year. That's shaping up to be materially lower than the 15% growth forecast for the broader market.

In light of this, it's alarming that Chemed's P/E sits above the majority of other companies. Apparently many investors in the company are way more bullish than analysts indicate and aren't willing to let go of their stock at any price. Only the boldest would assume these prices are sustainable as this level of earnings growth is likely to weigh heavily on the share price eventually.

The Key Takeaway

Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

Our examination of Chemed's analyst forecasts revealed that its inferior earnings outlook isn't impacting its high P/E anywhere near as much as we would have predicted. When we see a weak earnings outlook with slower than market growth, we suspect the share price is at risk of declining, sending the high P/E lower. This places shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

Don't forget that there may be other risks. For instance, we've identified 1 warning sign for Chemed that you should be aware of.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Retrospectively, the last year delivered an exceptional 23% gain to the company's bottom line. Still, EPS has barely risen at all from three years ago in total, which is not ideal. Accordingly, shareholders probably wouldn't have been overly satisfied with the unstable medium-term growth rates.

Retrospectively, the last year delivered an exceptional 23% gain to the company's bottom line. Still, EPS has barely risen at all from three years ago in total, which is not ideal. Accordingly, shareholders probably wouldn't have been overly satisfied with the unstable medium-term growth rates.

回顧過去的一年,公司實現了異常的23%的利潤增長。儘管如此,每股收益與三年前相比幾乎沒有上漲,這並不是理想的情況。因此,股東們對於不穩定的中期增長率可能不會感到特別滿意。

回顧過去的一年,公司實現了異常的23%的利潤增長。儘管如此,每股收益與三年前相比幾乎沒有上漲,這並不是理想的情況。因此,股東們對於不穩定的中期增長率可能不會感到特別滿意。