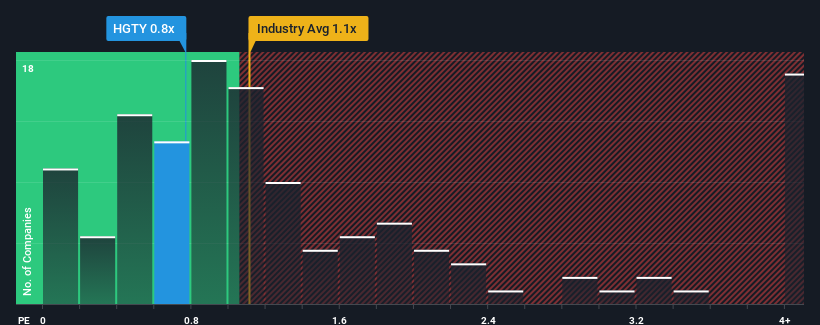

There wouldn't be many who think Hagerty, Inc.'s (NYSE:HGTY) price-to-sales (or "P/S") ratio of 0.8x is worth a mention when the median P/S for the Insurance industry in the United States is similar at about 1.1x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

NYSE:HGTY Price to Sales Ratio vs Industry December 28th 2024

What Does Hagerty's Recent Performance Look Like?

Recent times have been advantageous for Hagerty as its revenues have been rising faster than most other companies. It might be that many expect the strong revenue performance to wane, which has kept the P/S ratio from rising. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's not quite in favour.

Want the full picture on analyst estimates for the company? Then our free report on Hagerty will help you uncover what's on the horizon.

How Is Hagerty's Revenue Growth Trending?

The only time you'd be comfortable seeing a P/S like Hagerty's is when the company's growth is tracking the industry closely.

If we review the last year of revenue growth, the company posted a terrific increase of 21%. Pleasingly, revenue has also lifted 97% in aggregate from three years ago, thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing revenue over that time.

Shifting to the future, estimates from the two analysts covering the company suggest revenue should grow by 14% over the next year. That's shaping up to be materially higher than the 3.9% growth forecast for the broader industry.

With this in consideration, we find it intriguing that Hagerty's P/S is closely matching its industry peers. Apparently some shareholders are skeptical of the forecasts and have been accepting lower selling prices.

The Final Word

Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Hagerty currently trades on a lower than expected P/S since its forecasted revenue growth is higher than the wider industry. When we see a strong revenue outlook, with growth outpacing the industry, we can only assume potential uncertainty around these figures are what might be placing slight pressure on the P/S ratio. This uncertainty seems to be reflected in the share price which, while stable, could be higher given the revenue forecasts.

The company's balance sheet is another key area for risk analysis. Our free balance sheet analysis for Hagerty with six simple checks will allow you to discover any risks that could be an issue.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Have feedback on this article? Concerned about the content?Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com. This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If we review the last year of revenue growth, the company posted a terrific increase of 21%. Pleasingly, revenue has also lifted 97% in aggregate from three years ago, thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing revenue over that time.

If we review the last year of revenue growth, the company posted a terrific increase of 21%. Pleasingly, revenue has also lifted 97% in aggregate from three years ago, thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing revenue over that time.

回顧過去一年的營業收入增長,公司實現了21%的顯著增長。令人高興的是,得益於過去12個月的增長,營業收入自三年前以來總共也提升了97%。所以我們可以首先確認公司在那段時間內在營業收入方面做得很好。

回顧過去一年的營業收入增長,公司實現了21%的顯著增長。令人高興的是,得益於過去12個月的增長,營業收入自三年前以來總共也提升了97%。所以我們可以首先確認公司在那段時間內在營業收入方面做得很好。